This note was originally published at 8am on August 12, 2014 for Hedgeye subscribers.

"Mistakes are the portals of discovery."

- James Joyce

There is nothing like a mistake to enhance our learning. At times, defining a mistake can be a nuanced exercise. For stock market operators, though, a mistake is very easy to define. Simply: if a stock price goes against you meaningfully and over a sustainable period, you are wrong.

The most successful investors are often those investors that are effective at both learning from and minimizing their mistakes. Many successful portfolio managers implement a stop loss so as to ensure that their mistakes are minimized. Others buy value plays with little perceived downside to minimize mistakes.

About a year ago, we introduced Hedgeye’s Best Idea list. The idea of the list was to focus our research team on developing deep dive investment ideas with asymmetric reward characteristics. Overall, the list has had some really strong performers. Not surprisingly we’ve also had some stocks that have not performed very well. Due to a light global macro calendar this morning, we are going to do a deep dive on one of our very public “mistakes”.

Back to the Global Macro Grind . . .

Yesterday, one of our Best Ideas, Short Kinder Morgan Energy Partners (KMP), went against us and decidedly so. Rich Kinder, the CEO and Company’s namesake, decided to consolidate the group of companies that existed under the Kinder Morgan umbrella. In the announced deal, KMI, the C-Corp GP, will acquired its two MLPs, KMP/KMR and EPB in a ~$71B transaction comprised of 56% KMI equity, 38% assumed debt, and 6% cash.

On one hand, it is worth applauding Kinder for this move. After a long and successful run, we thought he was out of tricks, but he wasn’t. On the other hand, in implementing this dramatic corporate restructuring, Kinder readily acknowledged our thesis, which was that transparency was limited, cost of capital was very high, and growth options were limited for the Kinder Morgan complex. And by bidding for our favored short of the group, KMP, at premium, he also marked the idea against us by about 15%.

It doesn’t matter that we’ve had some great calls on other MLPS, such as Linn Energy (LNCO) and Boardwalk Partners (BWP), on KMP we are now seriously in the red. As always though, the question is what to do with the stock from here (even if you have been long and taking the other side of our trade it is worth considering). As my colleague Kevin Kaiser writes:

“On 2014 Pro Forma (“PF”) metrics, we have PF KMI valued at 17x EV/EBITDA, 24x EV/EBIT, 27x market cap/pre-tax earnings. If we strip out the E&P segment at a $5.5B valuation ($1.0B of EBITDA x 5.5x multiple), PF KMI Midstream is valued at 19x EV/EBITDA. On an absolute basis, the valuation multiples are very high, in our opinion (19x EBITDA for a capital intensive, fully-taxable, highly-leveraged business), but even relative to peers, PF KMI seems mispriced here. EPD – which is not subject to federal income taxes – is valued at 17x EV/EBITDA, two EBITDA turns below PF KMI Midstream”

Combined with this egregious valuation is the more interesting point of KMI’s ability (or inability) to pay out its massive distribution going forward. As Kevin also writes:

“On a cash flow basis, assuming a full tax shield, PF KMI will generate ~$5.3B/year in operating cash flow. Run-rate total CapEx is ~$4.1B/year (excluding Trans Mountain), putting run-rate, pre-tax Free Cash Flow at $1.2B, or $0.56 per PF KMI share. PF KMI is trading at a 1.4% pre-tax FCF yield. Its annual distribution burden will be $4.3B starting in 2015, putting its annual funding gap around $3.1B. These are rough metrics, but a good guide for how much capital PF KMI will need to raise on a go-forward basis.”

In the Early Look today, we’ve included two charts. The first chart is a comp table that Kinder Morgan showed in their presentation yesterday comparing KMI against blue chip companies with growing dividends. Included in the table are companies like McDonald’s, Cisco, Altria and so on. The title of the table is quite explicit, “KMI Compares Favorable to its Mid-Stream Energy Peers and S&P 500 High Dividend Companies.” Since the Company is guiding us to 10% dividend growth and a yield of 4.5%, on these basic metrics, KMI does look great! But beauty, as always, is in the eye of the beholder.

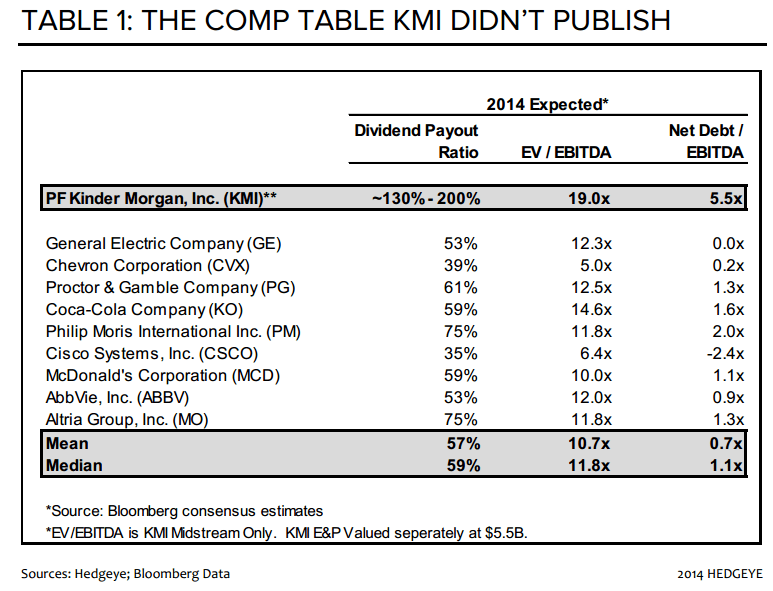

In the second chart in today’s note, we’ve included, “The Comp Table KMI Didn’t Publish.” In this table we look at payout ratios, valuation metrics, and leverage ratios. Far be it from us to question someone who yesterday made more money then we will perhaps every make, but we do think it is important to consider KMI’s risk profile in the context of some basic financial metrics.

Now perhaps we’ve lost all credibility because we didn’t see this corporate restructuring coming (we thought Kinder Morgan was in a proverbial box), but if you are contemplating owning KMI here, you do need to take the Company’s advice and look at your options, like S&P 500 high dividend companies.

On a basic level, would you rather own a company like Cisco that grows its dividend at ~7.9%, trades at ~6.0x EBITDA, and has $30 billion in net cash, or a company with the financial profile of KMI that trades ~19.0x EV/EBITDA, has debt/EBITDA at 5.5x, and has a dividend payout ratio of 130 – 200%. Perhaps we are just simpletons, but to us the answer is obvious.

Keep your head up and stick on the ice,

Daryl G. Jones

Director of Research