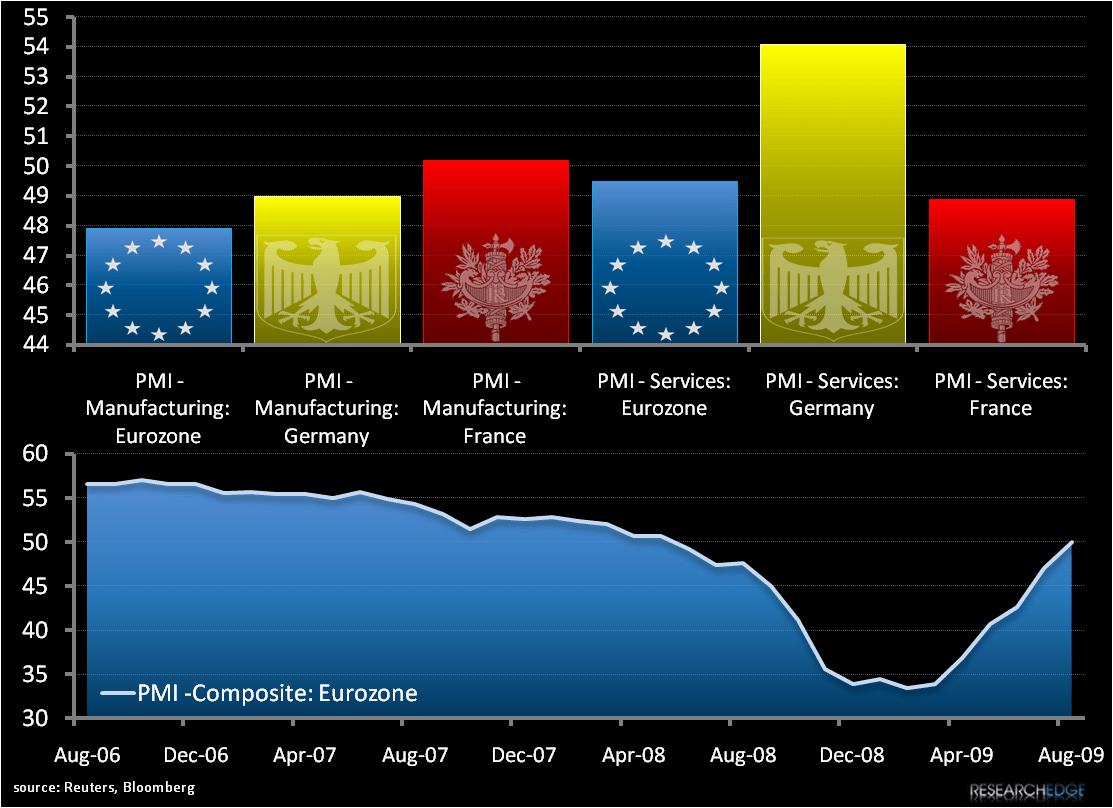

We’ve been hitting on improved fundamentals in Europe in recent posts and today’s European PMI numbers continue the positive trend we have been watching develop. Critically, PMI readings for the German service and French manufacturing sectors released today for August crossed the 50 threshold, which indicates expansion. According to Markit Economics the German service sector rose to 54.1 from 48.1 (far exceeding forecasts of 48.6) and French manufacturing rose to 50.2. German manufacturing and French services also improved sequentially but stayed in contracted territory at 49.0 and 48.9 respectively.

As we’ve been reiterating in recent weeks, we believe that the improvement in Europe’s larger economies will greatly benefit other parts of the region due to the interdependent of trade within the EU. Clearly the improvement in German and French PMI as the Eurozone’s largest economies that each posted Q2 GDP growth of +0.3% quarter-on-quarter helped lift the composite Eurozone PMI to a 15-month high at 50.0.

Today Keith made a tactical sale of our position in Germany (EWG) in our model portfolio, with the ETF up ~3.9% as the DAX traded at ~1.8% at the time of the sale. European indices reacted positively to the PMI numbers, up 2-3% across the region. Despite the improved fundamentals we still see slow growth across Europe ahead, with relative winners and losers on a country basis. Our bullishness on Germany remains in the intermediate term; look for us to buy back Germany on a down day.

Matthew Hedrick

Analyst