We weren’t overly surprised by Target’s guide-down today due to a) the fact that our comp and Gross Margin expectations were well below consensus for the quarter, and b) it makes sense that the company would want to front-load this news along with any lingering costs associated with the data breach and its debt retirement before Brian Cornell steps into the CEO seat on August 12. No CEO wants to step into a new role only to deal with near-term earnings events that he had nothing to do with. Look at Doug McMillon at Wal-Mart. He started at his job on Saturday February 1st, but the day before WMT guided down by 3% (meaningful for WMT).

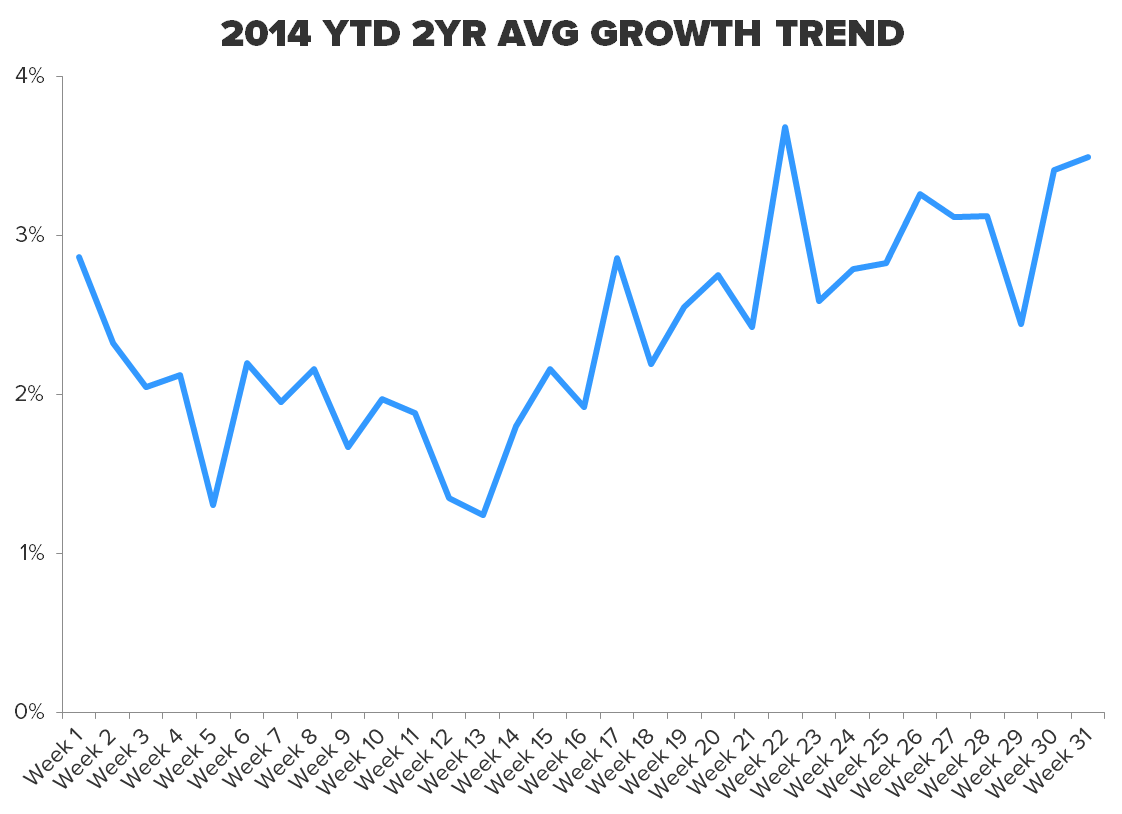

While the TGT headline talks about data breach and debt retirement costs, it’s important to note that comps are flat, and that was despite increased promotional activity. Canada was weaker than guided, though probably not much weaker than we expected. TGT reported this on the same day that we got yet another blockbuster week of retail sales data from ICSC. We’ve been looking at a string of weekly sales reports in aggregate that are better than 4% vs last year. The 2-year trend is also decidedly positive. If there was ever a time for even a mediocre retailer to surprise on the upside, we’d argue that this is it. But TGT did not. Maybe it’s because the high-end is outperforming, and TGT is going increasingly after the low-end consumer. Or maybe the retailer still has remarkably poor traction with consumers relative to its competitive set.

In the end, we’re still short TGT – though we fully acknowledge that all eyes are on Cornell at this point. We don’t yet know what he’ll do once in office. Will he patch the operation enough to boost earnings in years 1 and 2? That might be enough for the equity market to get behind the stock. Or, will he champion the investments needed to fix Target meaningfully and restore its reputation as one of the great retailers in the US? That would hurt earnings considerably near-term, but could make it a big winner in the outer years.

While the path that Cornell takes is in question, one thing that we think is inarguable for a long-term investor; to win big with TGT, it’s going to be very painful near-term. If the painful steps are not taken, then it does little to sharpen TGT’s positioning amongst a very tough competitive set (WMT, Department Stores, Dollar Stores, Supermarkets, and Amazon).