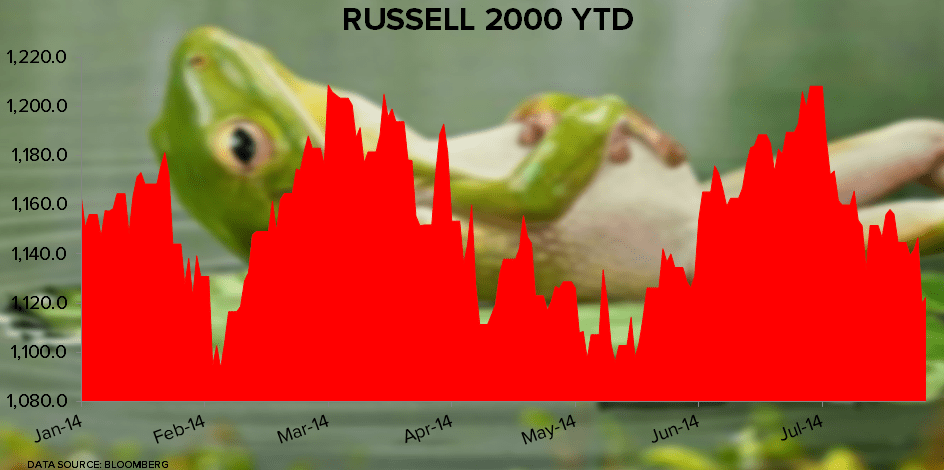

The Russell 2000 is down -3.7% year-to-date (and down -7.2% since the VIX bottomed July 7th).

This correction in U.S. growth expectations is real. Yesterday’s PMI print of 52.6 JUL (vs 62.6 JUN) was a friendly reminder that its not Q2 GDP that matters - #Q3Slowing does.

Editor's note: This is a brief excerpt from CEO Keith McCullough's morning research.