NOTE SUMMARY

- BEAT & RAISE AGAIN: Once again, YELP didn’t produce much upside to the print, beating revenue estimates by only 3%. The guidance raise wasn’t all that impressive either, up by $11-12M, which is a 4% raise on 2H14 after factoring in the 2Q beat. Incremental detail on the core metrics below.

- FOOL's GOLD: There are some obvious metrics that the sell-side bulls will be touting. We’re going to take a deeper look at what’s going on there, because most of it isn't that good, some of it is just scary.

- WINTER IS HERE: The turn happened sooner than we expected. We initially believed YELP's fundamentals would begin deteriorating in 2H14 and worsen through 2015, but YELP’s active business accounts took a sharp turn for the worse in 2Q14. Further, there is another glaring sign that the business model breaking down.

BEAT AND RAISE AGAIN

Once again, YELP didn’t produce much upside to the print, beating revenue estimates by only 3%. The guidance raise wasn’t all that impressive either, up by $11-12M, which is a 4% raise on 2H14 after factoring in the 2Q beat. Detail on the core metric below

- Revenues: Growth decelerated to 61% y/y (from 66% last quarter), despite an acceleration in local advertising growth to 69% y/y , from 67% last quarter

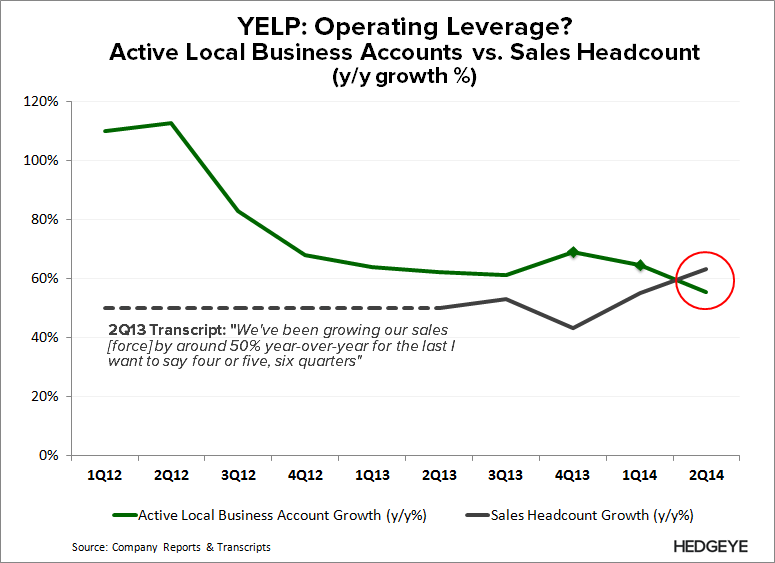

- Active Local Business Accounts: Decelerated sharply to 55% y/y growth in 2Q14 vs. 65% in 1Q14 (more detail below)

- Customer Repeat Rate: 75%, consistent with last quarter, which was a record for the company in its reported history.

- Attrition Rate: accelerated to 18.6%, from 17.9% in 1Q14.

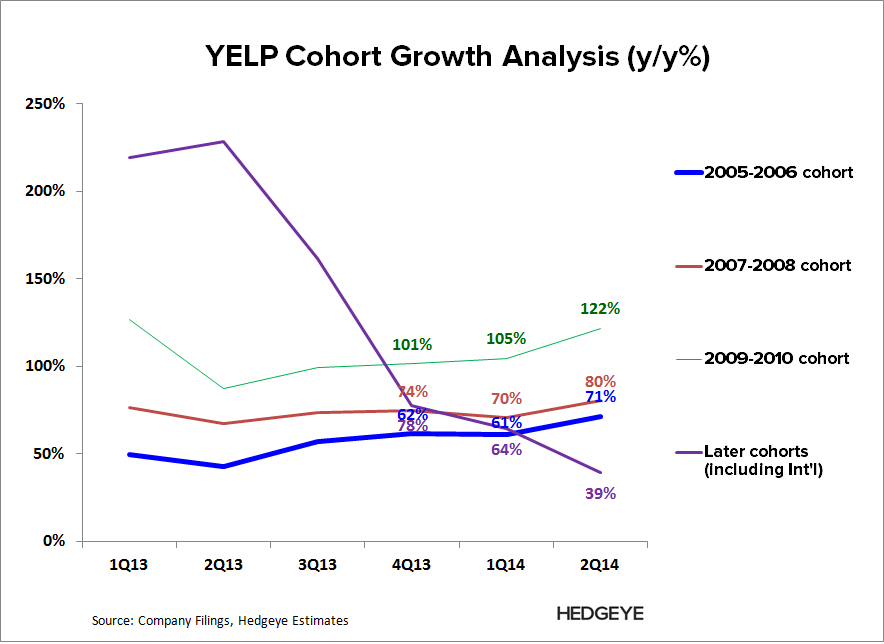

- Local Cohorts: 2005-2010 exhibited a sharp acceleration in revenue growth.

- Sales Headcount: Accelerated to 63% growth, vs. 55% in 1Q14

FOOL'S GOLD

There are some obvious metrics that the sell-side bulls will be touting. We’re going to take a deeper look at what’s going on there, because most of it isn't that good, some of it is just scary.

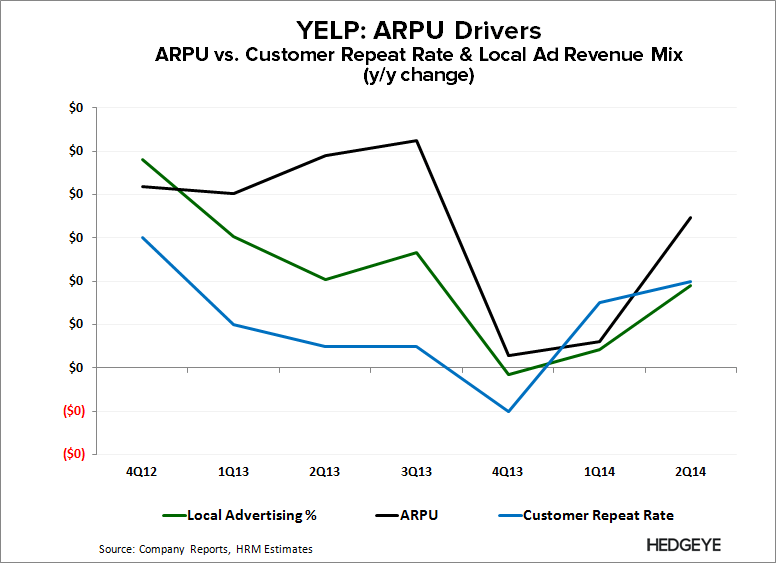

Customer Repeat Rate

This is not a retention metric, it is a measure of mix (new vs. existing accounts). The higher the customer repeat, the greater the mix of repeating clients, and the lower the contribution of new accounts. Reporting record highs in customer repeat rate is not a good thing, because it means there is a lower percentage of clients locked into longer-term contracts. When your business model is riddled by rampant attrition, that is a problem.

Surging ARPU

This is more of a function of revenue mix and the customer repeat rate than anything else. We estimate that Local Ad Revenue comes with a higher ARPU, so increasing mix there will drive the trend. Further, If YELP's repeat rate is higher, it has a higher percentage of customers paying the full quarterly rate than its new customers who may have only paid for one or two months. So while we have seen a surge in 2Q14, we suspect this has more to do with revenue sources vs. any underlying changes in the company's fundamentals.

Local Cohort Growth

This is going to get a lot of positive attention, but is actually one of our greatest concerns from the print. YELP produced a massive acceleration across each of its legacy cohorts. However, what isn't reported is the massive deceleration in its remaining cohort, which decelerated from 64% revenue growth in 1Q14, to 39% in 2Q14. However, that is not our main concern.

There is really only one explanation for the bifurcation in cohort trends: YELP is redeploying its salesforce to attack the earlier earlier cohorts. Maybe management is trying to juice its reported cohort metrics. More likely, management has realized that its scattered TAM in the later cohort are tougher to penetrate, meaning its's business model isn't viable here. Scary prospects when considering how large YELP's TAM really is.

WINTER IS HERE

We didn't expect YELP to begin showing signs of deterioration until 2H14, and it's net account growth decelerated sharply in 2Q14, with growth decelerating by 10 percentage points (the most since its hyper-growth phase in 2012).

We also need to consider that SeatMe customers are included in its 2Q14 accounts. YELP is no longer reporting this metric; management wouldn't answer the question during the call regarding the number of exclusive Seat-Me customers in 2Q14 (was last reported at 500 in 1Q14). In short, its core business is likely seeing more pressure than its reported metrics suggest.

So what happened? New account growth just wasn't good enough. It's not that the 20K new accounts added in 2Q14 is bad, it's actually a record (excluding the Qype transition in 4Q13). It's because attrition is starting to exert more influence over the model, and that's because YELP's account base is larger. So despite record new absolute account growth, net y/y account growth decelerated by 10 percentage points.

That is the problem with YELP's business model: the larger the account base, the higher its attrition, and the more new sales reps YELP must hire to drive enough new account growth to compensate.

This may be the more telling chart, because it calls the viability of its business model into question.

YELP is moving in a direction where its net account growth can't keep pace with its salesforce hires; that is what happens when you have rampant attrition. This means the long-term growth story doesn't have any legs. YELP must consistently hire more and more reps just to tread water, and do so at a declining to an eventually negative yield when these reps can't deliver enough growth to support their own salaries.

The company isn't dying, but its business model is, along with the +50% growth rates that street is paying 12x 2015 revenues for. It only gets tougher from here.

Let us know if you have any questions or would like to discuss in more detail

Hesham Shaaban, CFA

@HedgeyeInternet