Conclusion: We had previously bought into the popular thought process suggesting that LULU was too expensive to be an LBO, and it had the wrong financial and style characteristics for a private buyer. In the ‘strategic outcome bracket’ below, we assigned it only a 10% chance of happening, behind an all-out strategic acquisition (20%), and Chip selling his stock outright (35%). But after running through some LBO math, we’re more inclined to think that an LBO actually makes financial sense. Do we think that a deal will be announced tomorrow with the stock at $39? Probably not -- although the math would support it. But for those like us who are trying to get a handle on where the real downside support is in this stock, we think this helps show that it is in the low-$30s. The risk/reward on the long side still looks really favorable here to us.

Here are some key considerations in our analysis.

1. A Traditional LBO is Not In The Cards. The IRR makes sense for a traditional LBO, but the leverage characteristics do not. Our analysis below suggests a 20% premium from the current price, 35% equity, an exit multiple 25% below entry multiple, and that margins come down below 18% over the modeling time horizon. All of that suggests an IRR of just over 20%. Overall, that’s reasonably attractive. But the problem is with leverage.

*Click image for larger view

2. This chart shows the leverage ratios for the highest levered deals in the market over the past decade. The highest leverage ratios occurred in 2007/08 just before the recession, and those numbers topped out at 8.2x debt/EBITDA. A standard, run-of-the-mill Private Equity buyout would imply leverage of 8.8x. That’s simply way too high for us to view as any margin of support.

Source: Forbes

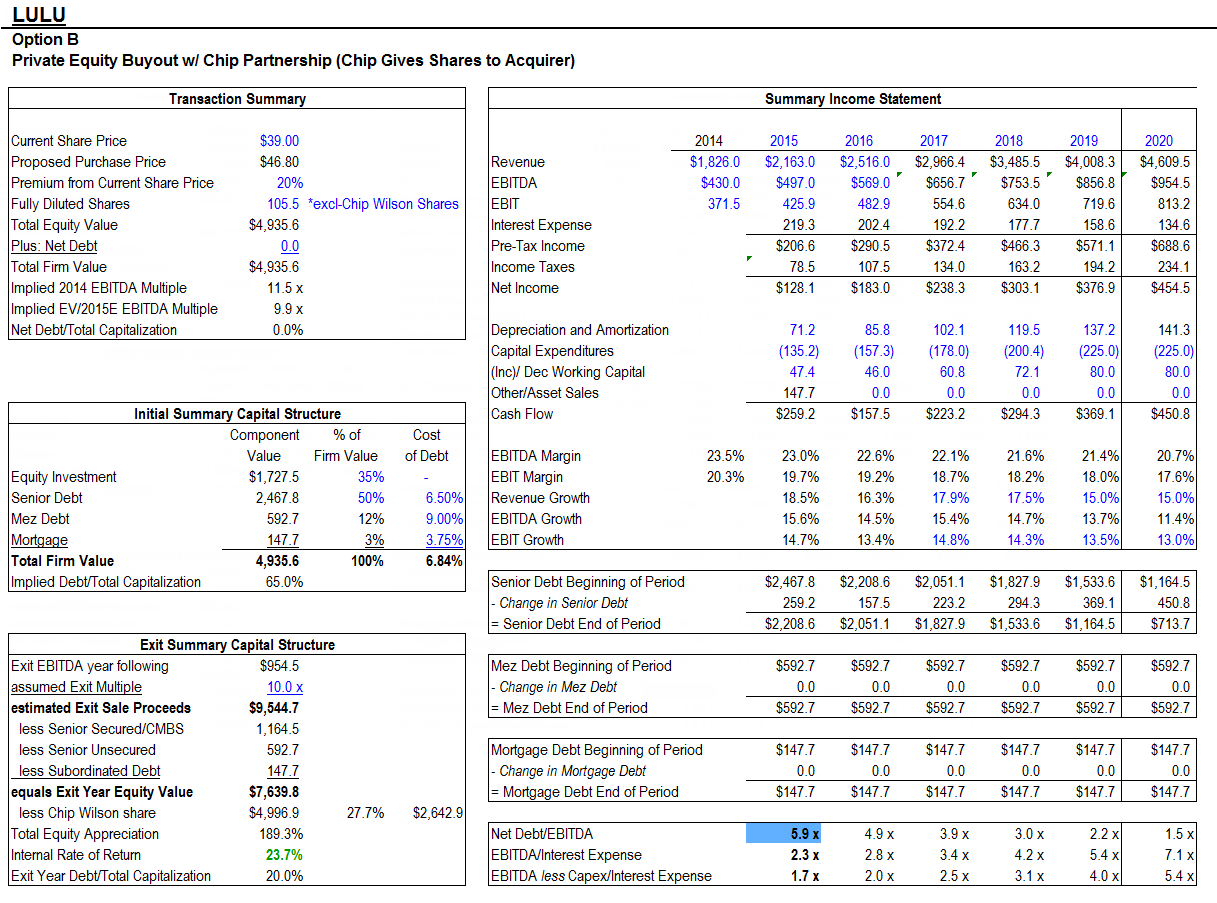

3. But, here’s where Chip can help. The fact is that the guy owns 27.7% of the common equity. There’s no reason he cannot team up with a private buyer in a way where he contributes his stock to the partnership, and gets the same return as the financial buyer on the way out. In effect he becomes a de-facto creditor to a financial buyer. That way, the combined entity still puts up $6.8bn for LULU, but one of the sources of financing is Chip’s $1.9bn in stock. That brings the leverage ratio for a deal down to 6.1x, which is right in line with the 5.7x rate we’ve seen year-to-date for LBOs.

4. Here’s the revised model assuming that Chip facilitates this transaction with his own stock. Assuming the same operational inputs in the model described above, this suggests an IRR closer to 24%, but importantly, with palatable leverage.

*Click image for larger view

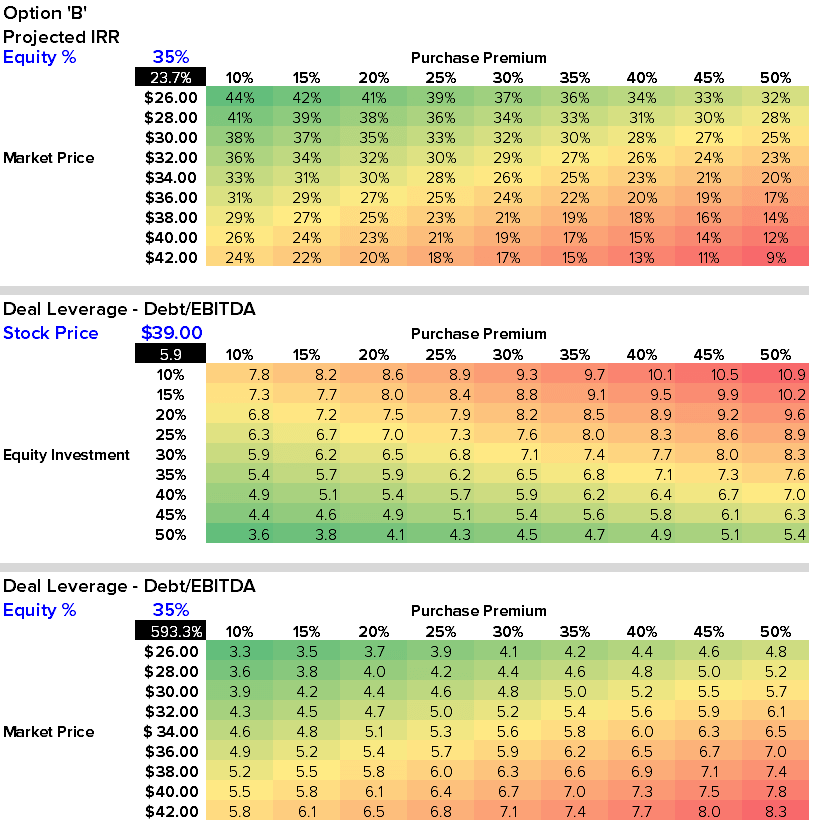

5. Here’s a sensitivity analysis that we use to triangulate price, leverage, and IRR. The punchline is that a deal works with the stock (before takeout premium) anywhere starting with a $3-handle. Obviously, the return gets a lot more attractive as the stock nears $30. But for that reason, it might never get there.

*Click image for larger view

6. We used a 20% premium for no other reason than it has been the gold standard for retail names over the past decade. Some would argue that we need a bigger premium given how much LULU has declined over the past year. But truth be told, all LBOs are beaten down before they’re bought. It’s the nature of the beast. We shouldn’t think of LULU any differently.

Source: SSRN

HERE'S OUR NOTE FROM JUNE 25th ON WHY WE ADDED LULU TO OUR BEST IDEAS LIST AS A LONG

Conclusion: Today we hosted a conference call to discuss the rationale behind why we added LULU to our Best Ideas list as a long after the stock’s latest collapse. As we’ve said before, the call right now has nothing to do with our confidence in the business or the team running it. This is a company in a defendable category with an outstanding brand, a $95bn addressable market, and a realizable $4-$5bn revenue stream over 5-years. But the catch is that it’s still sitting on a $500mm management team and operating structure. The good news is that never in LULU’s history has there ever been a path to creating value, and that’s due to the sometimes painful, and usually embarrassing presence of its founder, Chip Wilson. But we think that the Board structure that he created will ultimately lead to him outright failing in his current attempt to regain control of the company. That is likely to be a catalyst for one of many forms of change, which we explored in our presentation and deck. We plucked out a few of the more salient slides that we think are worth considering. Let us know if you’d like the replay and the full materials.

The LULU Bracket

This diagram is noisy. It’s supposed to be. Start reading it on the left with the decision of whether or not Chip Wilson wins control of the Board We very generously gave him 20% probability. But in reality he’ll be lucky to get 10%. If he loses, which he will, we think that one of two outcomes is most likely; a) he sells his stock (35% chance) – representing 27.7% of shares outstanding, or b) there’s a deal – 10% likelihood of a buyout, or 20% chance of an acquisition. When all is said and done, about 80% of the outcomes get us to a price well above $41.

Outcomes, As We See Them

1) Management Team Upgrade (49% probability): Each scenario results in a potential management upgrade, but the biggest likelihood is if Wilson sells his stock. All in, we get to a 49% chance of a meaningful change in management (including putting in place a high caliber CEO). This company needs better executives, and a lot more of them. This is a team that we think would proactively invest in systems needed to more appropriately discount product – something LULU sorely needs – and tackle its competitors head on instead of clinging on to a ridiculous hope of a perma 55% Gross Margin. The way it is being run today, the company is on its way to becoming Coach. We firmly believe changing that path is not a very difficult one. All in, this scenario gets us back to the discussion of $3-$4 in earnings power, or a $60-$100 stock (20x $3.00, and 25x $4.00).

2) Deal (30% probability): The biggest barrier to a deal getting done in the past has been that Chip didn’t want it to happen. Now he’s likely searching for one. Our sense on Wilson is that he feels handcuffed by LULU. He’s not allowed to participate in anything having to do with the company aside from attend Board meetings, but he’s too big a shareholder to go off and start another brand (something he’s actually very good at) due to his non-compete. If he can’t gain control, he could look to get the company sold. We think that a buyout with a PE partner is not very likely – as there’s not a ton of private buyers that would take out a high margin company at 15x EBITDA. But we think that the set of strategic buyers is a) far more expansive and b) less price-sensitive.

3) Status Quo (21% probability): This outcome pretty much stinks. The reality for LULU is that a status quo management team and status quo operating plan results in a far less than status quo stock price. We see about $10 downside to $30-32 if this is the case ($1.50 in EPS – 15x p/e and 10x EBITDA). This is the outcome that would cause us to pull the plug on our call – though we don’t think this will come to fruition.

Board Considerations

There’s a few reasons why Chip will likely not regain control of the Board.

1) Giving up the title of Chairman in late 2013 is the worst thing Chip could have done. We think that was one of the final moves in a game of chess the real Board was playing with him. He agrees to step down from being Chairman if Laurent Potdevin gets the green light to be CEO. Potdevin is likely not the guy for this job, but it was a great move in hindsight by the Board.

2) Why? Only the CEO, Chairman or a majority of the Board can call a special vote at LULU. Chip cannot do it. He literally has a better shot at selling the company outright than he does in calling a simple special Board meeting.

3) There are 10 Board members, and three are clearly on ‘Team Chip’. But the Board has an offensive weapon in that it is authorized to have between 3 and 15 Board seats. All the Board needs is a simple majority (which Chip likely will not be included in) and it can appoint up to five new Directors -- none of whom are likely to be aligned with Wilson.

4) Better yet, there are staggered seats with three year terms. So if Board members are appointed today, he or she doesn't have to be voted on by shareholders until 2017.

5) All in, Chip’s ownership has been steadily shrinking, but his influence has been shrinking faster. He knows this. All the more reason to make a move to get out.

Who’s A Buyer?

We think that there’s a lot of companies that want to own LULU, but unfortunately, not a lot of companies can afford to do the deal at $8bn. We calculated the leverage for a host of suitors pre and post transaction, and also looked at year 1 accretion and dilution for each company. The punchline for us is that LULU is not likely to be bought by an American company. We’re thinking German, French or Japanese.

a) Nike: NKE won’t buy what it thinks it can build for less money. Whether you agree with them or not is irrelevant. They think they can beat LULU organically, so they won’t buy it.

b) Adidas: AdiBok needs it, can afford it, and couldn’t care less about near-term dilution. This makes a ton of sense.

c) UnderArmour: This makes zero sense strategically or financially. I’m surprised I’m asked this so often.

d) VFC: This would be a big nut for VFC to digest, but they could afford it – barely. VFC has gotten less value-conscious in recent years (i.e. TBL) so maybe it’s a possibility. But a dark horse for sure.

e) PVH: This is a company that needs a deal like LULU, but it would crush PVH financially. Tough luck Manny.

f) Fast Retailing: The Japanese owner of Uniqlo is looking to aggressively expand into the US, and needs to diversify away from its mall retail fashion push. The fit makes sense, the accretion is a no brainer even past $70, and let’s not forget that Fast was almost on the hook for buying J Crew in March for $5bn until it saw how bad Mickey’s business was trending.

g) Kering: CEO is on the tape saying he wants to buy sports brands to augment Puma, Tretorn and Volcom. KER could digest LULU in a heartbeat. French company might keep Laurent on board, as well.

h) GPS: This one is another consideration – albeit a long shot. It would take GPS’ debt to total capital to about 65%, which is likely far above the Fisher family’s comfort level. Perhaps GPS will be content chipping away at LULU with Athleta, which is crushing it.