RAI Announces LO Acquisition; Surprise on Share Price and Sale of blu E-cigs!

Today we are removing long LO from our Best Ideas list. After adding LO on 2/26/14 at $47.74 and months of rumors that it would be taken out, this morning RAI announced its intention to buy LO in a cash-and-stock transaction currently valued at $68.88, or a total of $27.4B (including debt).

The price is significantly below our share target of $80, and it’s worth note that there is significant runway before the deal is expected to close in 1H 2015. That said, this has been a fantastic position for us. Based on last night’s closing price the stock is up over 40% from where we added it as a Best Idea.

Before we dive into the specifics of the announcement, we want to underline that beyond RAI we do not see another competitive bidder for LO. Further, given that we expect a lengthy regulatory approval process on anti-trust considerations this deal is still a long way from closed and may present a further investment opportunity.

As the market expected, Imperial was transformative in aiding this deal. It’s committed (pending shareholder approval) to buy RAI’s menthol brands of KOOL, Salem, and Winston, and well as LO’s Maverick and e-cig business blu for $7.1B or $4.4B after tax. This would make Imperial the third largest U.S. tobacco company.

The menthol divestiture is seen as a key consideration for regulatory approval (FTC is the main governing body), however the willingness of RAI to part with blu caught us by surprise. As we outlined in our Best Idea call in early March, we viewed blu as a key driver lifting the total company’s sales growth and accounting for 31% of EPS by 2018. The e-cig business therefore significantly factored into our share price estimates for an RAI acquisition.

Given blu’s leading U.S. market share in e-cigs (~ 45%), we believe that RAI is telling the market that 1) it squarely believes in its own e-vapor business (VUSE) and 2) is showing regulators that its portfolio is pro competitive (across both combustible and non-combustible). RAI’s VUSE is still in its infancy – the company launched in initial test state markets earlier in the year, and is in the process of national distribution in its first phase to roll out in 15,000 stores.

So what are the hurdles that remain?

- LO and RAI shareholder approval remain outstanding. BAT appears to be a very committed partner - it agreed to maintain its 42% ownership in RAI through an investment of ~ $4.7B, agreed to vote its shares in favor of the transaction, and with RAI has agreed in principle to pursue an ongoing technology-sharing initiative for the development and commercialization of next-generation tobacco products, including heat-not-burn cigarettes and vapor products.

- Regulatory. the FTC will decide on anti-competitive regulatory issues, however we think RAI took appropriate steps to divest its menthol exposure, create a viable U.S. competitor in Imperial, and signals a pro-competitive stance on the e-cig/e-vapor category by selling blu. The process by which the FTC makes a judgment may be drawn out (hence RAI targeting 1H 2015). We maintain that menthol presents a minimal regulatory risk, assigning less than a 20% over the longer term, and believe that RAI’s acquisition proves out an environment of limited risk.

RAI + LO Boost Market Share to 34%

We are bullish on the combined power of RAI + LO as the 2nd largest U.S. tobacco company to compete with #1 MO (~51% share). RAI + LO will compete for the top spot across industry categories:

- Newport, Camel, Pall Mall and Natural American Spirit in combustible cigarettes

- Grizzly in smokeless tobacco

- VUSE in the e-cigarette market

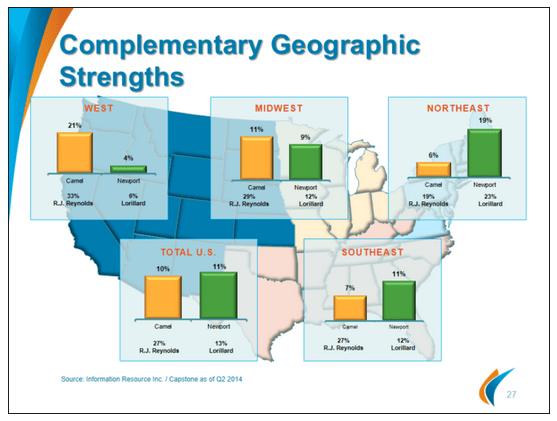

As was central to our Long LO call we continue to like menthol’s superior fundamentals to traditional tobacco. Newport Menthol is the #1 U.S. menthol brand (37.4%) and is the #2 U.S. cigarette brand, with overexposure to urban areas and the eastern U.S. RAI expects to reap $800M in cost savings over two years and we think the strong sales and brand equity of LO’s portfolio is complemented well by the strength in RAI’s non-menthol brands like Camel, and its more western U.S. geographic exposure. The combined company’s ability to leverage a larger sales force, attain more shelf space and compete for higher margin (premium and above premium cigarettes and smokeless) should prove very profitable.

Additional Acquisition Details

- Under the terms of the transaction, which has been approved by the boards of directors of both companies, Lorillard shareholders will receive, for each Lorillard share, $50.50 in cash and 0.2909 of a share in RAI stock at closing, representing $68.88 per share based on RAI's closing share price yesterday. Upon closing, Lorillard shareholders will own approximately 15% of RAI.

- Following the transaction, RAI is projected to have over $11B in revenues and approximately $5B in operating income

- RAI expects the transaction to be accretive to earnings in the first full year, with strong double-digit accretion in the second year and beyond (on a percentage basis).

- As part of the divestiture, Imperial will acquire certain assets owned by Lorillard including its manufacturing and R&D facilities in Greensboro, N.C., and approximately 2,900 employees, including a national sales force.

- Once the transaction is completed, a transition period will commence during which R.J. Reynolds will contract manufacture KOOL, Salem and Winston for Imperial and Imperial will contract manufacture Newport for R.J. Reynolds.

- The RAI/Lorillard transaction and the Imperial transaction are scheduled to close substantially at the same time, 1H 2015.

- Lorillard will continue its existing dividend policy until the deal closes. RAI plans to maintain its current dividend policy until the transaction closes (~80%) and is targeting a dividend payout ratio of 75% going forward.

- RAI will generate significant cash flows and expects to maintain its investment grade credit rating following the transaction.

- RAI has secured fully-committed bridge financing and expects to issue permanent financing for the transaction.

- Susan Cameron will remain RAI's president and CEO after completion of the acquisition while LO CEO Murray Kessler will join RAI's board after the transaction closes.

Howard Penney

Managing Director

Matt Hedrick

Associate

Fred Masotta

Analyst