What is Retail Sales?

It’s a trivial, but not an insignificant question.

In casual conversations with investors, particularly those who aren’t Macro centric, I’d say a majority don’t technically know what Retail Sales encompasses. Superficially, the term “Retail Sales” kind of connotes that it’s a broad measure of the 70% of the economy that is consumer spending – and most people take it that way.

In fact, retail sales is an estimate of spending at department stores, food service providers, auto dealers, and gas stations. In other words, it is largely an estimate of spending on goods.

In other, other words, while it’s a timely, insightful barometer of the prevailing state of domestic consumerism, it doesn’t include spending on services, which comprises the lion’s share of consumption at ~2/3 or household spending and ~45% of GDP

The numbers are also volatile on a month-to-month basis, subject to significant revision and reported on a nominal basis – making it difficult at times to distinguish whether sales trend changes are due to prices or volumes.

Anyway….

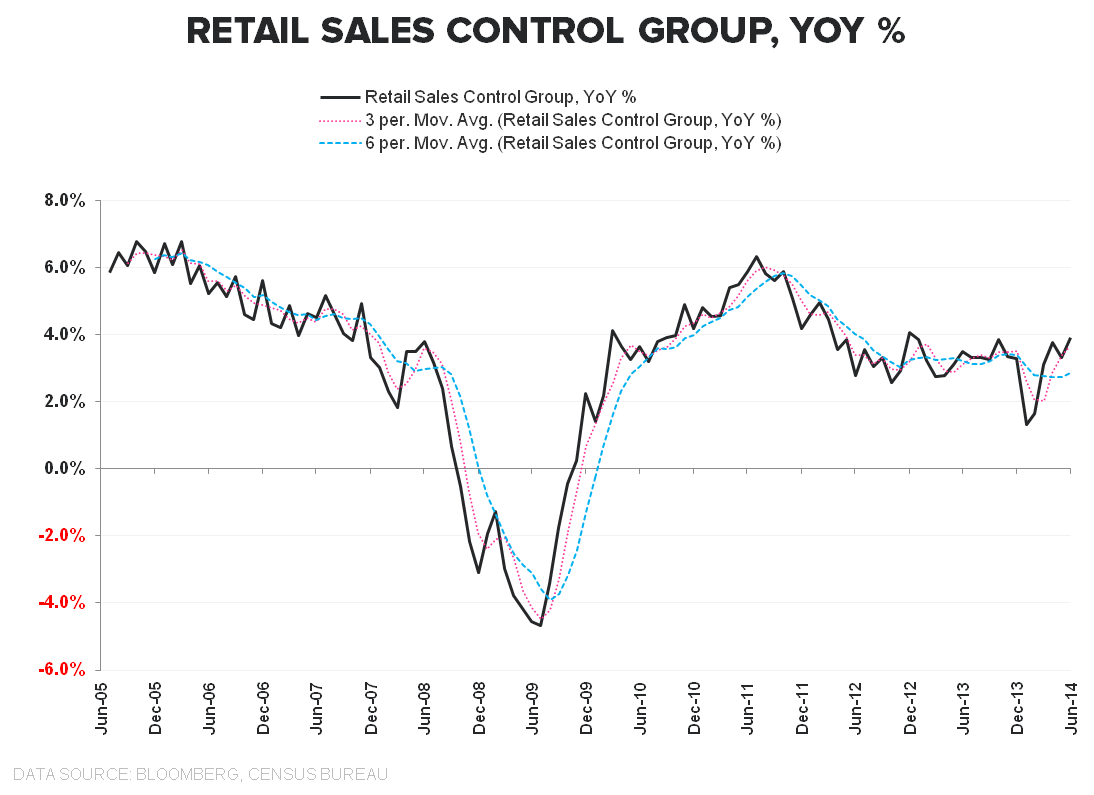

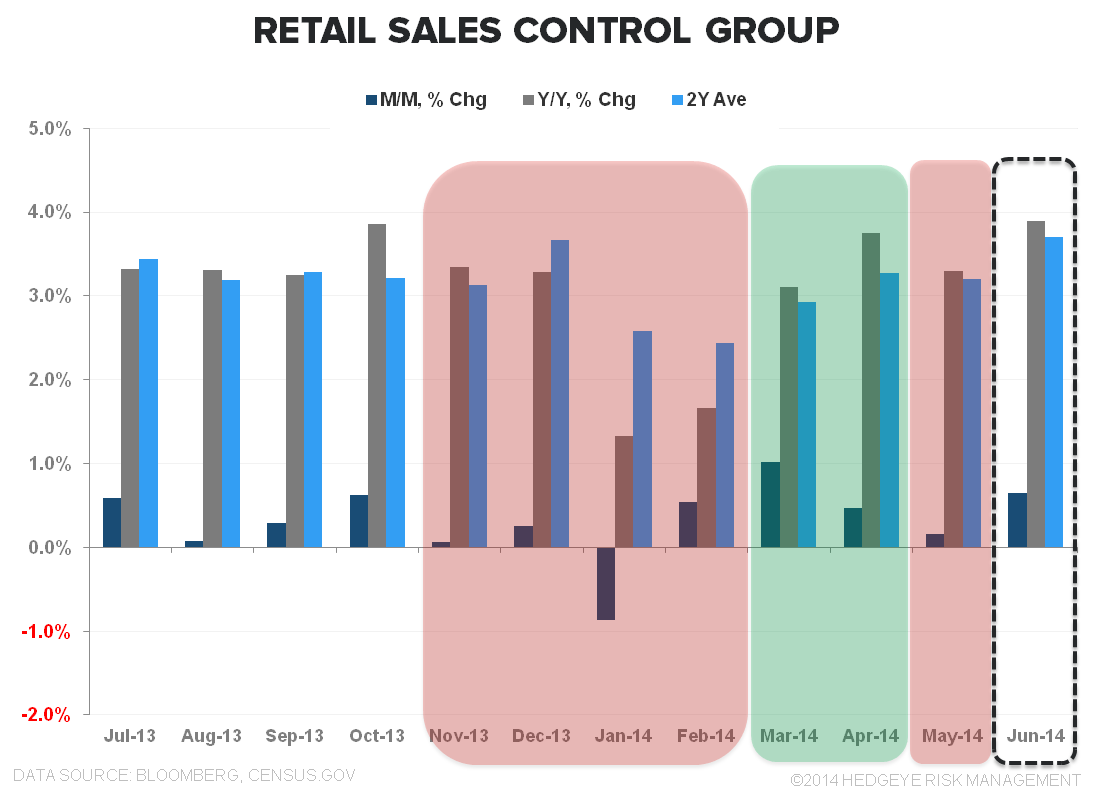

DECENT HEADLINE, CONTROL GROUP RETRACES MAY DECLINE

Retail sales in June rose 0.3% MoM, decelerating -30bps sequentially to +4.3% YoY. Strong reported auto sales in June again buttressed headline growth, although the miss vs expectations suggests pricing was probably weak.

Under the headline, the Retail Sales Control Group (Retail Sales ex Food, Auto Dealers, Building Materials & Gas Stations, which feeds GDP) accelerated modestly on a MoM, 1Y, and 2Y basis after decelerating across all three measures in May.

General Merchandise, Personal Care, and Nonstore/Electronic Sales (the E-sales proxy) led gainers while 9 of 13 categories improved MoM.

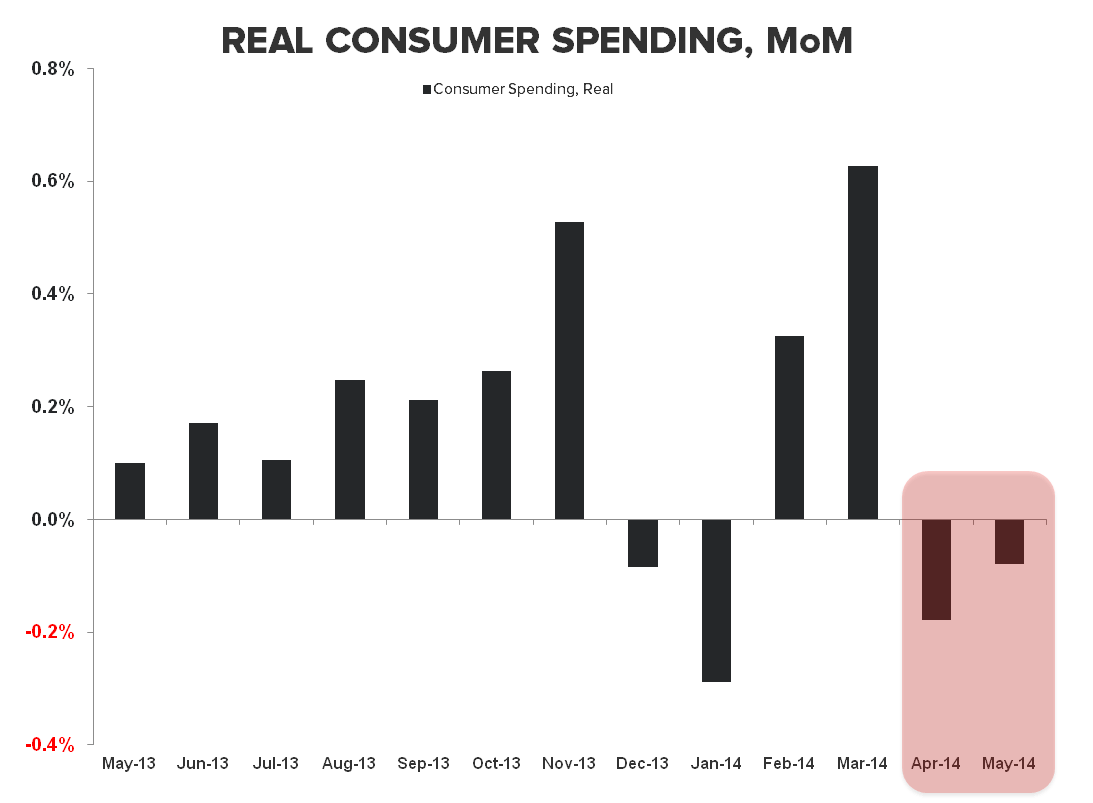

Overall, “decent” is probably an apt descriptor for the June data, particularly in the wake of negative MoM growth in Real Consumer spending in both April and May.

Relatedly, Consumer Credit Growth Continues To Improve….

We previously highlighted the Fed G.19 Data from April which showed US revolving consumer credit balances rose at a month-over-month annualized rate of +12.3%, the fastest rate of growth since 2001 and a positive inflection relative to the steady, ~0-1% growth reported the last few years.

On the back of the jump in revolving credit in April, the recently released May data showed a +2.1% MoM annualized increase, the third straight month of sequential, above-trend growth.

So, credit growth (credit cards, autos, C&I) is showing some positive mojo of late and the ever increasing reality of our modern, consumption economy remains: credit = spending = the marginal driver of growth.

Whether the nascent credit acceleration can support and/or catalyze a breakout in domestic growth remains to be seen.

With #InflationAccelerating, Real Wages decelerating, and the consumption data middling-to-slowing, the early read through appears to be that consumers are tapping credit to maintain consumption levels in the face of compressing household margins.

Christian B. Drake

@HedgeyeUSA