TODAY’S S&P 500 SET-UP – June 26, 2014

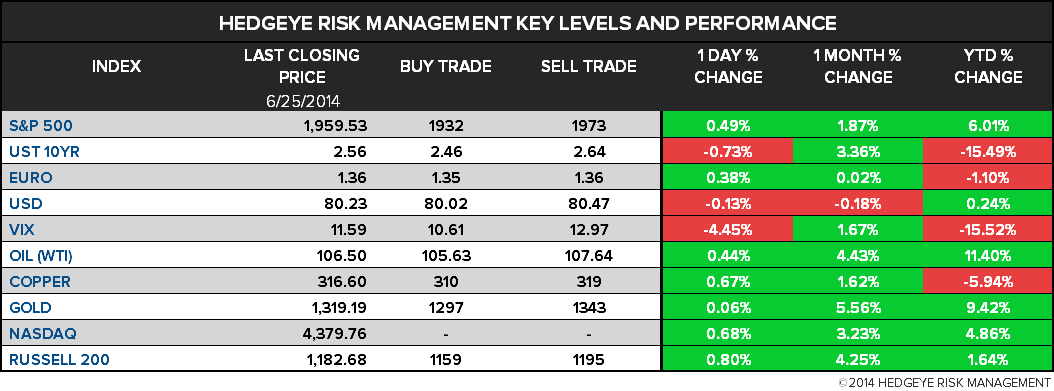

As we look at today's setup for the S&P 500, the range is 41 points or 1.40% downside to 1932 and 0.69% upside to 1973.

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.08 from 2.08

- VIX closed at 11.59 1 day percent change of -4.45%

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: Initial Jobless Claims, June 21, est 310k (prior 312k)

- 8:30am: Personal Income, May, est. 0.4% (prior 0.3%)

- 8:30am: Personal Spending, May, est. 0.4% (prior -0.1%)

- 9:45am: Bloomberg Consumer Comfort, June 22 (prior 37.1)

- 11am: Kansas City Fed Manufact., June, est. 10 (prior 10)

- 8:30am: Fed’s Lacker speaks in Lynchburg, Va.

- 10am: Freddie Mac mortgage rates

- 10:30am: EIA natural-gas storage change

- 1:05pm: Fed’s Bullard speaks in New York

GOVERNMENT:

- House, Senate in session

- Israeli Pres. Shimon Peres to receive Congressional Gold Medal

- 9:15am: House Financial Services panel holds oversight hearing on SEC’s division of trading and markets

- 9:30am: Senate Judiciary Committee markup of S. 2454, Satellite Television Access Reauthorization Act; S. 517, Unlocking Consumer Choice/Wireless Competition Act

- 10am: Senate Finance Cmte Chairman Ron Wyden markup for proposal to shore up highway trust fund through end of year

- 10:30am: Senate Appros Cmte markup of DHS appropriations bill

- U.S. ELECTION WRAP: Election Night Preserves Old Guard

WHAT TO WATCH:

- LSE to buy Frank Russell for $2.7b to boost indexes, ETF

- Philip Morris cuts earnings forecast amid currency headwinds

- BNP said to face yr-long dollar-clearing curb in U.S. case

- Nabors unit, C&J Energy Services to combine in $2.86b deal

- GoPro IPO raises $427m as shares price at top-end of range

- China finds $15b of loans backed by false gold trades

- Ukraine peace deal optimism wanes as cease-fire deadline looms

- IRS’s Lerner weighed audit involving Grassley, e-mails show

- BHP considers opportunities to export oil condensate from U.S.

- Supreme Court to issue rulings

EARNINGS:

- Accenture (ACN) 7:01am, $1.21

- ConAgra Foods (CAG) 7:30am, $0.55

- Empire (EMP/A CN) Bef-mkt, C$1.22 - Preview

- Lennar (LEN) 6am, $0.51 - Preview

- McCormick (MKC) 6:30am, $0.62

- Nike (NKE) 4:15pm, $0.75 - Preview

- Progress Software (PRGS) 4:15pm, $0.34

- Schnitzer Steel Industries (SCHN) 8:30am, $0.06

- Shaw Communications (SJR/B CN) 8am, C$0.49 - Preview

- Steelcase (SCS) Bef-mkt, $0.16

- Winnebago Industries (WGO) 7am, $0.39

- Worthington Industries (WOR) 8:25am, $0.67

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- China Finds $15 Billion of Loans Backed by Falsified Gold Trades

- Brent Trades Near One-Week Low as Iraq Supplies Rise; WTI Holds

- U.S. Corn Glut Expanding at Fastest Pace Since 2005: Commodities

- Cotton Futures Fall After Entering Bear Market on Global Supply

- Gold Falls as Investors Weigh U.S. Economy Amid Slower Purchases

- Aluminum Users Stick With LME as Alternative Yet to Gain Volume

- Steel Rebar Climbs as Ore Posts Record Gain on China Property

- China’s Gold Imports From Hong Kong Drop as Yuan Rate Swings

- Stronger Indian Gold Demand to Support Prices in 2H: Macquarie

- Goldman Says Shale Gas Boom Driving Fear Out of Market: Energy

- Danske Bank Says Brent May Slip to $110/Bbl as Iraq Oil Stable

- Iraq Crude Untouched by Violence Means Options Seen Too Bullish

- El Nino Has 60% Chance of Starting by End of August, UN Says

- California Drought Means Record Produce Prices: Chart of the Day

- Rubber in Tokyo Climbs to 2-Month High as China Inventory Falls

CURRENCIES

GLOBAL PERFORMANCE

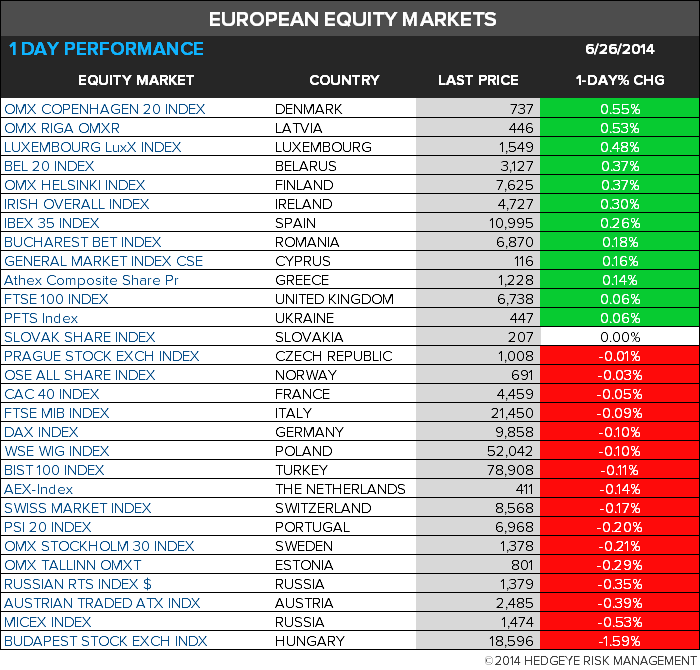

EUROPEAN MARKETS

ASIAN MARKETS

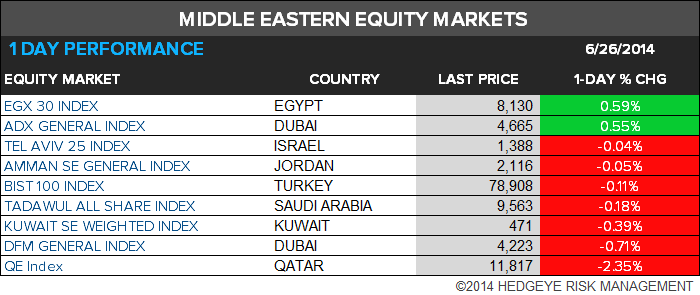

MIDDLE EAST

The Hedgeye Macro Team