Following June’s rather significant slowdown across the board, MCD reported July comparable sales growth that improved on a 2-year average basis in each of its geographic segments with global same-store sales up 4.3%. Relative to my expectations for the month, based on the company’s guidance and 2-year average trends, the 2.6% and 7.2% growth in the U.S. and Europe, respectively, came in strong.

The U.S. number surprised me somewhat as MCD was lapping a 6.7% number from last year. The quality of that growth will not be known, however, until we learn more about how margins are trending in the quarter because MCD increased its coffee promotions/giveaways during the month of July. These types of promotions are most likely helping traffic at the expense of average check and mix.

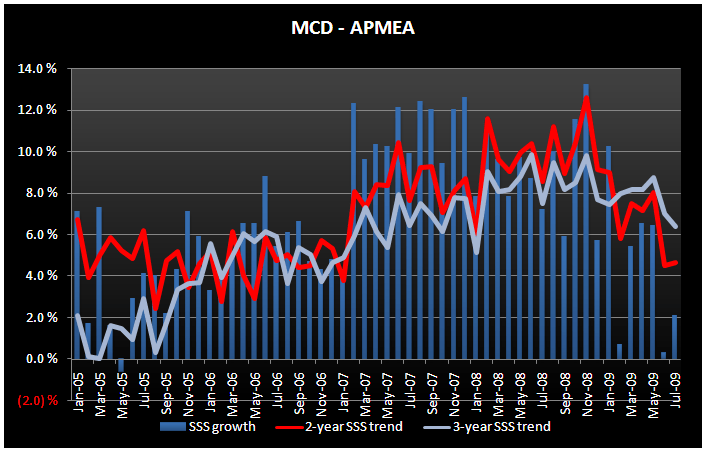

APMEA’s 2.1% comparable sales growth, although better on a sequential basis from June, is reflective of trends that remain weak relative to the segment’s recent performance as China continues to be a drag on results.

Systemwide sales declined 0.3% in July. The negative foreign currency impact of 6.5% moderated from the 8% impact in both Q1 and Q2 and should continue to moderate throughout the third quarter and turn positive in Q4.