This note was originally published at 8am on June 11, 2014 for Hedgeye subscribers.

“We hold these truths to be self-evident: that all men are created equal.”

-Thomas Jefferson

A big government central planning bureaucrat got his butt whipped down in the heartland of American Constitutionalism last night. Not unlike in the 1970s, when Nixonian Republicans and Cartering Democrats all started to sound the same on economic matters, Americans voted for change.

If Eric Cantor doesn’t make your skin crawl, you and I probably won’t be having beers at the Rangers/Kings Stanley Cup tilt tonight in NYC. This guy isn’t a free-market-liberal-conservative like me. On economic matters, he is a raging Keynesian.

Bring on the self-evidence that is the Policy To Inflate crushing at least 80% of Americans via cost of living and The Dave Brat. The winner of the 7th District of Virginia is a free-market economics professor! How cool is that? On days like this, even this proud Canadian wants to be American.

Back to the Global Macro Grind…

This is not a political statement. I don’t support the Tea Party inasmuch as I don’t support either the Republican or Democrat parties. This is an economic statement that is ringing as true in the United Kingdom today as it did in the Unites States of America in 2013. Strong Currency; Stronger Country.

If you have a Policy To Inflate (weaken your currency via both monetary and fiscal policy), you get what Harvard’s Marty Feldstein finally explained (WSJ Op-Ed yesterday) to the central planning wonks at the Fed: #InflationAccelerating.

And when you get inflation accelerating the cost of living in America to all-time highs, you aren’t going to get re-elected by lying to people and telling them otherwise. The truth is self-evident.

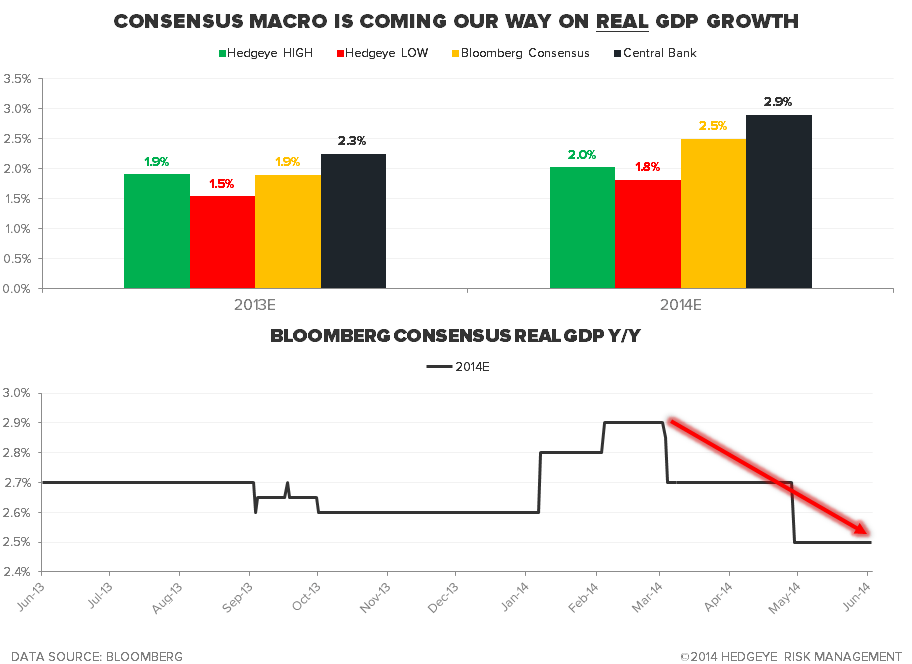

BREAKING: World Bank Cuts US GDP Growth Forecast

#nice

Finally someone, somewhere, in the land of officialdom-nod took their US GDP forecast closer to Hedgeye Risk Management’s. While the World Bank didn’t cut its GDP outlook by enough, the point is they had the spine to do what Consensus Macro research won’t, until it’s too late.

To review our call on US GDP Growth slowing into Q3 of 2014 – it’s math:

- Top line (GDP) acceleration in US GDP growth peaked in Q3 of 2013

- Inflation (the Deflator, which you subtract from nominal GDP) bottomed in Q2/Q3 of 2013

In other words, the year-over-year comparisons put Q3’s probability of inflation slowing US consumption growth at its highest level since Q1 of 2008.

“So”, don’t ask a linear-economist who missed calling either the Q1 of 2008 or Q1 of 2011 US #InflationAccelerating calls for their Top 10 reasons why they are still using the same models that haven’t proactively predicted real-world consumption slowdowns. Ask the bond market.

At 2.64% on the 10yr US Treasury Yield (down hard from 3.03% on January 1st, 2014), the entire construct of #OldWall consensus still thinks “it’s different this time” (i.e. that they were only wrong on both rates and GDP rising in Q1 because of the weather).

Every time the bond market sells off to higher-lows, you buy it. Every time US domestic consumption growth gets bid up to no-volume-lower-highs, you sell it. That is the Hedgeye Macro Playbook for US stocks vs bonds investing in 2014, and we are sticking to it.

Another way to position for what I just wrote is as follows:

- Buy Bonds via TLT, BND, or anything equities that looks like a bond (XLU, VNQ, etc.)

- Sell US Domestic Growth like Consumer Discretionary (XLY) and Housing (ITB)

If you didn’t buy puts on Cantor’s political message, you could have bought #InflationAccelerating via Oil and Gold futures too.

In other news, the SP500 had its 38th day of not moving more (+/-) 1% yesterday. That’s the 2nd longest streak of compressed complacency in 15 years. No worries though, everyone will be able to get out, at the same time, because “this time is different.”

In case you aren’t yet convinced that it is different this time:

- Fear (VIX) has never held below 10, ever (it’s at 10.99 this morning)

- II’s Bull/Bear Spread (survey) just hit fresh YTD highs at +4540 basis points wide to the Bull side

- One legged ducks still swim in a circle

Whether you are a bond bull, US growth bear, or a Brat from Virginia this morning, we stand together fighting the tyranny of mediocre minds trying to centrally plan us into thinking we need their inflation policies to live freely. We hold these free-market truths to be self-evident. They always have been.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.44-2.65%

SPX 1935-1959

RUT 1136-1184

VIX 10.78-13.34

Pound 1.67-1.69

Brent Oil 109.10-110.96

Gold 1240-1273

Best of luck out there today,

KM