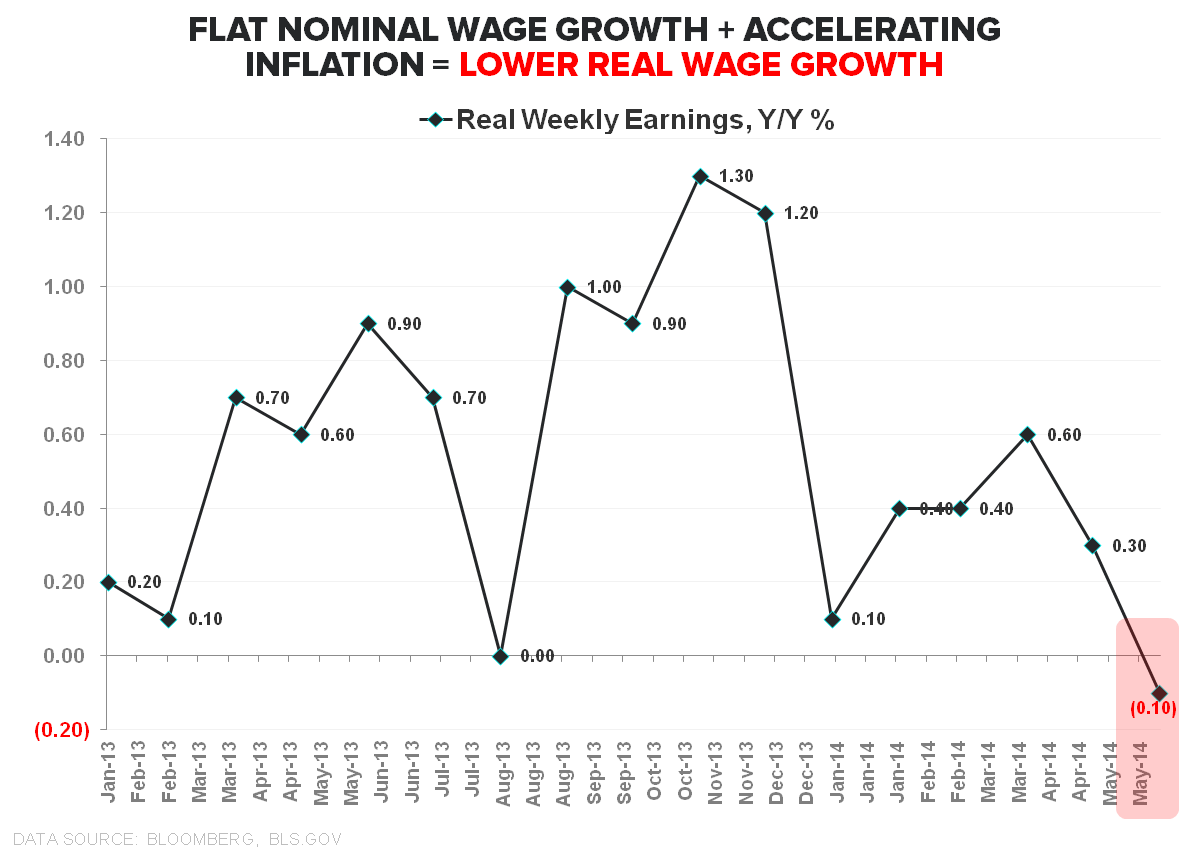

Takeaway: U.S. real-wages (what you get paid in terms of wage growth minus made-up gov't inflation) just went negative for the 1st time in 2 years.

Takeaway: U.S. real-wages (what you get paid in terms of wage growth minus made-up gov't inflation) just went negative for the 1st time in 2 years.

By joining our email marketing list you agree to receive marketing emails from Hedgeye. You may unsubscribe at any time by clicking the unsubscribe link in one of the emails.