“Here, our books are filled with numbers. We prefer the stories they tell. More plain. Less open to interpretation”

- Iron Bank of Braavos, Game of Thrones

After yesterday’s negative revision to 1Q14 GDP (see HOW LOW CAN YOU GO), this morning’s retail sales data should serve as another blow to forward growth expectations.

While full year growth estimates continue to get clipped with regular frequency, the collective cognitive dissonance over the outlook for consumption - in the face of overtly middling data - remains very much entrenched.

Indeed, looking across our Economic Summary table (below), the amount of sequential “Worsening” continues to belie the “accelerating recovery” narrative and sticky, 4%’ish, consensus GDP estimates.

We did see a modest, expected bounce across the breadth of manufacturing/confidence/labor data into 2Q and reported growth will accelerate sequentially but, essentially, we are what the numbers suggest.

Take the average of (soon to be revised lower) 1Q14 gdp and the (overly optimistic) 2Q14 estimate:

(-2.0% + 3.5%) /2 = More Muddle

The current domestic macro reality is that with Inflation accelerating (food, shelter, energy), housing decelerating, the labor market middling, and tougher growth/inflation comps through 3Q14, the intermediate-term trend for consumption growth is one of deceleration.

RETAIL SALES: Ugly April figures were revised higher, but back to deceleration in May.

Headline retail sales, supported by the significant jump in Auto Sales (+16.7M in May vs. 16.1M April), advanced 0.3% MoM in May (est. +0.6) while April numbers saw a positive revision to +0.5% from 0.1%.

Figures were more sanguine under the hood as more than half of industries saw negative MoM growth and decelerating YoY growth. Further, MoM growth in the Control Group (which feeds GDP) was slightly negative with growth decelerating -70bps and -10bps sequentially on and YoY and 2Y basis, respectively.

The broader takeaway from today’s data is largely the same as its been the last 6 weeks or so – the numbers are ‘okay’ but do not reflect a material acceleration or any significant rebound demand from deferred 1Q consumption

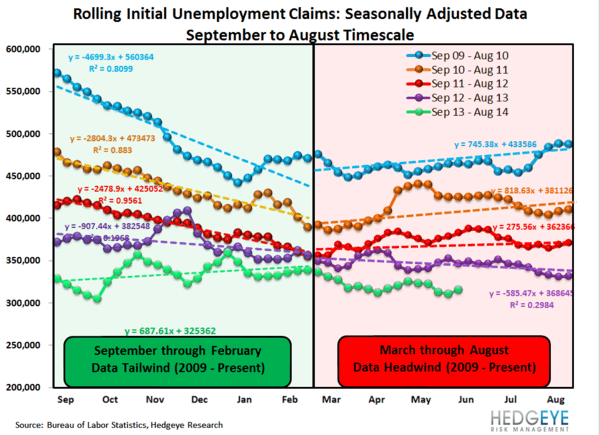

INITIAL CLAIMS: The labor market continues to positively clip along, but it's becoming an outlier amid an avalanche of negative evidence.

This morning’s initial jobless claims data showed a moderate, sequential deceleration in the rate of improvement, but the trend remains solid. The continued strength in the high frequency labor market data is becoming a bit of a positive outlier.

Our head of Financials research, Josh Steiner, aptly contextualized this morning’s data:

There's growing uncertainty over the macro outlook. Data seemingly in conflict includes labor data that appears to be solid, but housing and retail sales data that are showing signs of cooling off.

Our choice to use initial claims data as our macro weather vane stems from its accuracy in the last cycle at pinpointing both the top and bottom of the cycles on a real time basis. For example, in the last downturn initial claims began to move higher on a seasonally-adjusted basis in late 2007. Recall that the S&P 500 reached its peak level in October, 2007. Conversely, initial claims peaked and began to roll over sharply in March, 2009, also coincident with the trough in the market.

With that in mind, this morning's initial jobless claims data is good, though not great. Seasonally adjusted rolling claims are at 315k, which remains in bull market territory by historical standards. Meanwhile, the year-over-year change in rolling non-seasonally adjusted claims came in at -8.8%, also a strong print (though less strong than the week prior).

More #InflationAccelerating data on deck for tomorrow…..

Christian B. Drake

@HedgeyeUSA