What Once Was Old ...

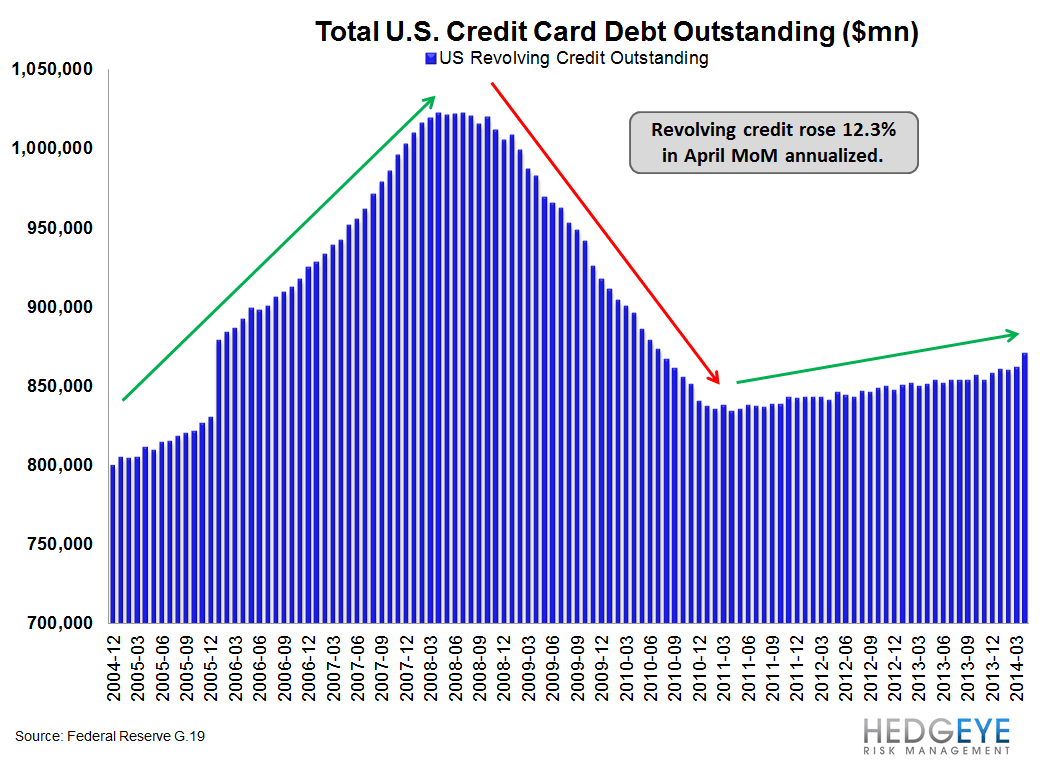

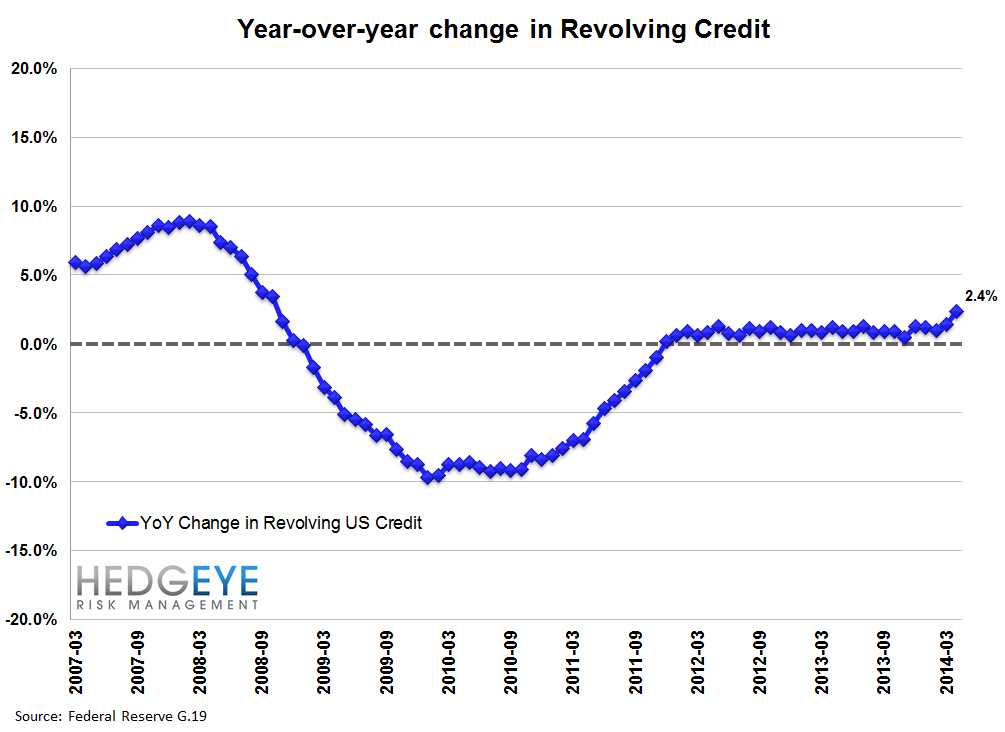

We haven't written about the Federal Reserve's G.19 consumer credit report in ages, and that's because there's been nothing to say. U.S. credit card loan balances have been muddling sideways at a 0-1% rate of growth for the last two and a half years. But in the last two months there's been an upturn, and suddenly it looks like it might be interesting.

One of our guiding principles is that we try and take note of inflection points in the rate of growth, i.e. the second derivative, since it's these second derivative changes that precipitate changes in the multiple.

Along those lines it's interesting to take a step back and consider whether the sleepy credit card space may have just entered such an inflection point.

On Friday afternoon of last week the Fed released its G.19 report for the month of April and it showed that US revolving consumer credit balances rose at a month-over-month annualized rate of +12.3%, the fastest rate of growth in, well, a really long time. In fact, you'd have to go back to the early/mid 1990s to revisit that rate of growth on a sustained basis. To be fair, we've followed the G.19 data for years and, speaking from experience, it's a very choppy and often-revised data series. We wouldn't get overly excited about it but for the fact that Capital One's numbers for the month of April also reflected a sharp upturn in the rate of growth in US credit card receivable balances.

We should know more on Monday next week when we get the May data from the various credit card companies.

In late January we issued a report arguing investors should get long Capital One following the 4Q earnings "blow-up". Our analysis showed that there was a quantifiable advantage to owning shares historically from the late January through mid-July timeframe. This owes largely to the fact that, like a clock, Capital One misses the 4Q numbers and beats the 1Q numbers every year. Our original intention was to exit the long trade ahead of reporting 2Q numbers, but now that growth is starting to show signs of life we may be interested in extending our duration. We'll know more on Monday.

Seriously?

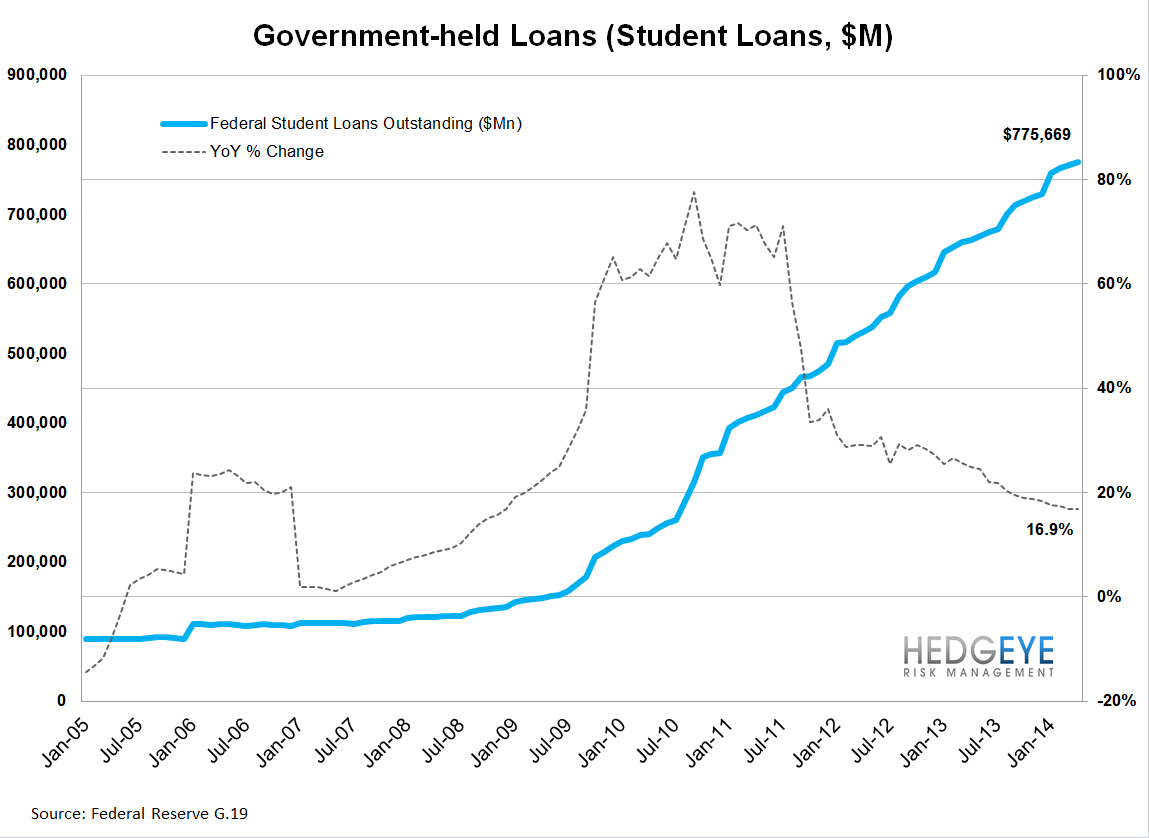

On a separate note, we just couldn't resist the temptation to flag the unstoppable force that is student loan growth in this country. The chart below, also taken from the G.19 data, shows the amount of federally-backed student loans sitting on the books of the United States. Currently the figure stands at $775 billion, up $112 billion (+16.9%) in the last 12 months. For those wondering why there seems to be no recovery in the first time homebuyer market we offer the chart below as "Exhibit A".

Joshua Steiner, CFA

Jonathan Casteleyn, CFA