This note was originally published at 8am on May 27, 2014 for Hedgeye subscribers.

“Although I’ve made this walk thousands of times, it never gets old.”

-Ed Catmull

That’s how the President of Pixar Animation Studios, Ed Catmull, describes his life in the introduction to an excellent book I started reading this weekend called Creativity Inc. Catmull is a computer scientist who was hired in the late 1970s by a 32 year old by the name of George Lucas.

Catmull went on to run Pixar alongside another American capitalist by the name of Steve Jobs. He is 69 now and his book isn’t as much a memoir as it is a lesson in learning how to be creatively destructive, as a team.

The book’s early chapters will sound quite familiar to those of you who embrace the principles of transparency and trust alongside practical applications of #math and #behavioral economics: “Honesty and Candor”, “Fear and Failure”, and “Change and Randomness.” #Solid summer time read.

Back to the Global Macro Grind…

Walking onto the independent research platform we built 6 years ago never gets old. It gets more interesting and exciting the more we empower new players on our team to be the change. All the while, as my hair gets greyer, I’m still banging out this Early Look note just trying to keep up!

Trying to keep up with no-volume rallies in the preferred hedging instrument of thousands of hedge funds (SPX and E-minis) never gets old either. “Why are we up?”, “Why can’t we go higher?”, “Why can’t I beat beta?” – the underlying whine to this whole thing can make a man want to go on vacation.

Setting aside that we have not been recommending short SPY (we’ve been making the call to short US Growth – i.e. the Russell 2000) here’s what’s going on with the emotion of it all:

- Friday’s no-volume-ramp to an all-time closing SPY high of 1900 came on one of the lowest volume days of the year

- Total US Equity Market Volume was -23% and -41%, respectively, versus its 1 and 3 month averages

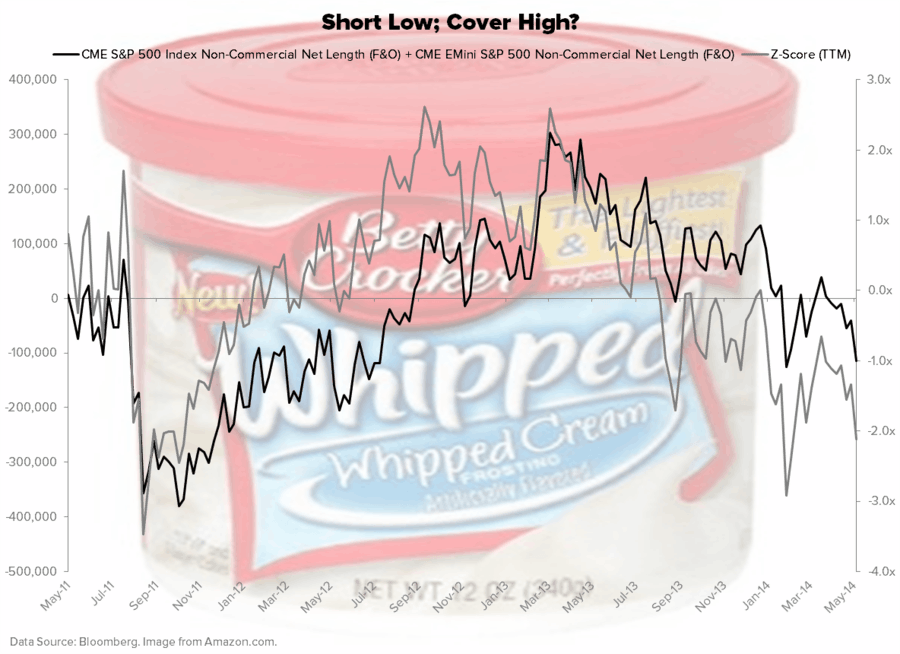

- CFTC futures and options contracts in SPX (Index + E-mini) ended with a net SHORT position of -114,248 contracts

In other words, with almost 9,000 hedge funds trying to manage an all-time high in AUM (assets under management) of $2.7 TRILLION in a no-volume market that goes straight up after they shorted it in April-May, the short-term game gets tougher.

Putting the -114,248 net short contract position (SPX Index + E-mini) in context is critical:

- That’s -73,347 contracts week-over-week (almost 60% shorter)

- Versus the 6 month average of +9,810 net LONG position, that’s bearish positioning

- Versus the 1 year average of +62,224 net LONG position, that’s really really bearish

Where time, price, and positioning is relative to where it was, across multiple-durations, is how we analyze things here @Hedgeye. It’s all about the rate of change. And it changes, both fast and slow.

Why would consensus be getting bearish on US Growth?

- 10yr US Treasury Yield was only up 1 basis pt last wk to 2.53% = down -50bps YTD and signaling US #GrowthSlowing

- Despite its no-volume +2.1% bounce to lower-highs last wk, the Russell2000 is still -6.8% since March and -3.2% YTD

- US GDP for Q114 could be revised to NEGATIVE (from its preliminary +0.11%) when it’s reported this Thursday

I know. Everyone nailed it. Everyone you read every morning made the call that US GDP would be negative in the first quarter (it would have been -2% btw if the US government used MIT’s Billion Prices Project measurement of +3.9% inflation) and the 10yr yield would be -17% YTD.

But that doesn’t matter this morning, because the name of the game isn’t intermediate-term TREND investing – it’s short-term performance chasing, baby! So what would get me to saddle up and ride the spooo-hoo bull?

- US Dollar Up

- Interest Rates Up

- Commodity and Cost of Living Inflation Down

Ex #3 (US rents hit an all-time high last week and the CRB Commodities Index was up another +0.8% to +10% YTD), we actually got some of that last week:

- US Dollar Index +0.4% last week to back in the black (of +0.4%) YTD

- 10yr Yield up a beep (1 basis point) to 2.53%

Buying the all-time-high price in anything just isn’t how I roll. But if that’s the sort of thing you are into from a “long-term investing” perspective, here’s some short-term positivity that Mr. Macro Market looks like he might chase – on a 15-day duration, the SPX and USD have POSITIVE correlation of +0.60.

Yep, that was last year’s risk management call on being long growth (Dollar Up, Rates Up, Equity Growth Multiples Up – Bond Bulls smoked). The 2014 call is much more aligned with the 90-day INVERSE correlation between SPX and USD of -0.62.

Right now, USD is overbought and the bond market couldn’t care less about no-volume stock market rallies. Get USD and Rates right, and you’ll probably get the TREND calls in long growth vs slow-growth right. Although I feel like I have written about this on 1,000 macro mornings – it never gets old.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.47-2.61%

SPX 1878-1906

RUT 1089-1135

Nikkei 13885-14658

USD 79.99-80.49

WTIC Oil 102.67-104.77

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer