“For most of us, failure comes with baggage.”

-Ed Catmull

Got baggage? I do. Over the years, it just piles up.

The way I see it, athletically, professionally, and personally, if I wasn’t always failing somewhere, I wouldn’t learn a darn thing.

The guys at Pixar like to say things like “fail early and fail fast” and “be wrong as fast as you can” (Creativity Inc., pg 109). I like that attitude. In this business, there’s nothing worse than being wrong and staying wrong. We just want to get on with getting it right.

Back to the Global Macro Grind…

For most of 2014, being long the Russell 2000 has been as wrong as being bullish on US GDP growth and/or interest rates. Last week, that wasn’t the case. On no-volume (Friday’s Total US Equity volume was -32% vs. the 3 month avg), the Russell 2000 was +2.7%.

After getting smoked on the short side pretty much every way you can over the course of my career, I have learned to wait and watch for my signal. Thankfully, I waited until Friday to re-issue the sell signal on the Russell 2000. I did it in the morning, so it’s -0.22% against me.

As far as my score goes, being wrong by 1 basis point is still being wrong – so the #1 question on my mind this weekend was whether or not I am going to be wrong and stay wrong this week?

In order to answer the US growth question, here are the signals I care about most:

- Long-term Interest Rates

- US Consumption Growth

- US Dollar Rate of Change

If you ignored the first 4-5 months of the year, on that scorecard things looked better than bad last week:

- US Treasury 10yr Yield was +12 basis points on the week to +2.60%

- US Consumer Discretionary Stocks (XLY) were +1.9% on the week

- US Dollar Index was up a whopping +0.1%

Not to be confused with the year-to-date TREND:

- UST 10yr Yield is still -43 basis points after starting the year at 3.03%

- US Consumer Discretionary and the Russell 2000 are both only +0.1% YTD

- USD hit its YTD low in May then v-bottomed when Europe opted for negative interest rates

In other words, who needs to learn from failing with Currency Devaluation Policies To Inflate, when all America has to do is wait for Europe or Japan to take a turn failing faster?

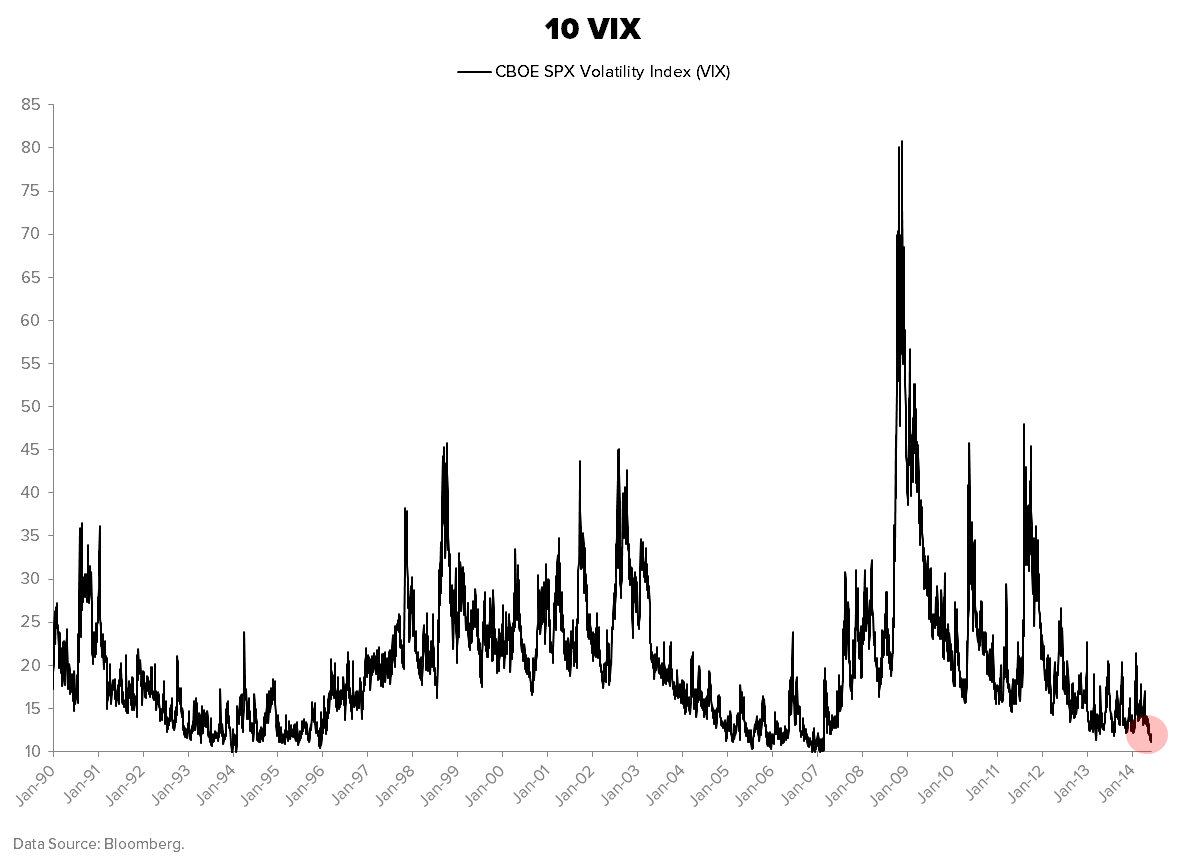

This is all quite sad to watch as we’re sucking every last lemming into buying, well, anything at 10 VIX. As you can see from our Chart of The Day, if you want to fail really, really, fast in this business, get your clients levered-long the US stock market at 10 VIX (US Equity Volatility Index).

I know, I know – they (as in the dudes on the Old Wall who had you chase them to all-time bubble highs in the summer of 2007 when the VIX was at 10 last time) say it’s different this time.

Really? Last week the VIX officially crashed (-5.7% to -21.6% YTD). All the while, that crowded hedge fund short position we’ve been writing about in the SP500 got squeezed. After peaking at -114,248 net short futures and options contracts (SPX Index and E-mini) on May 27th, the Pain Trade was higher.

So here’s your 2nd chance to sell everything US consumer and housing growth that you could have sold in JAN-FEB of 2014. If we’re right, you don’t want to make the same mistake twice. The VIX has never held, sustainably, below 10. Even for those of us with a lot of baggage, never is a very long time.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.41-2.61%

SPX 1

RUT 1130-1169

USD 80.02-80.73

EUR/USD 1.35-1.37

Best of luck out there this week,

KM

Keith R. McCullough

Chief Executive Officer