THE HEDGEYE EDGE

“The Perils of Falling Inflation.” Like clockwork, that phrase was on the cover of the November 9th – 15th issue of The Economist right after headline CPI bottomed at +1% YoY in OCT ’13. Fast forward to today, domestic consumer price inflation – on the government’s conflicted and compromised metric – is running +100% higher at +2% YoY (APR ’14).

Inflation doubled, lol!

Ok, that’s probably not very funny – especially if you’re a consumer that is feeling the pinch of rising inflation. Growth in real incomes in America has slowed from its cycle-peak of +1.3% YoY in OCT ’13 to +0.3% YoY as of APR ’14.

TIMESPAN

INTERMEDIATE TERM (TREND) (the next 3 months or more)

Luckily you, unlike the vast majority of Americans, can do something about it. In line with our #InflationAccelerating macro theme (introduced in JAN ‘14), we continue to anticipate that reported inflation will accelerate throughout 2014. There are three primary reasons we hold this view:

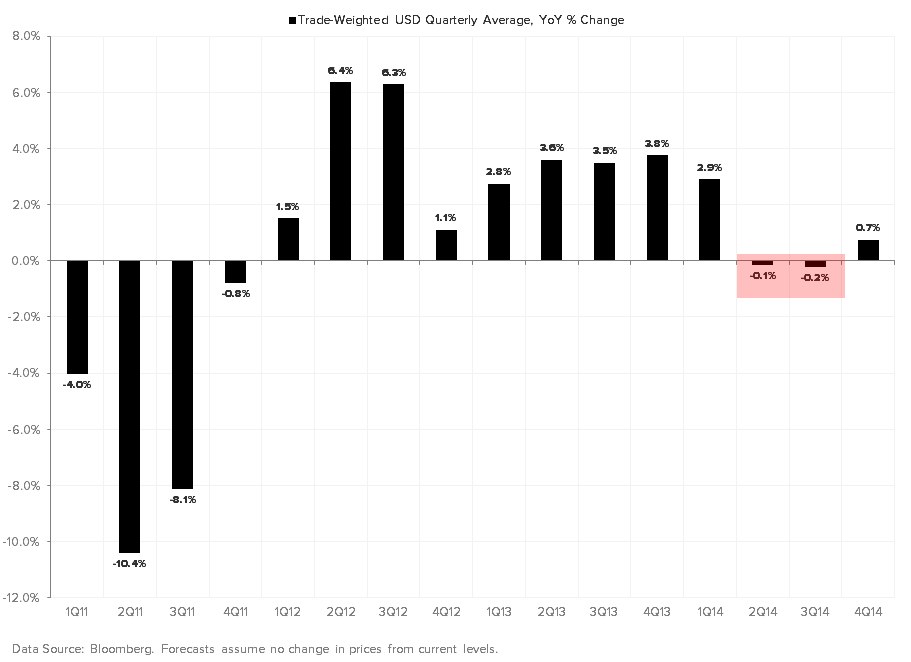

ONE: Holding current prices flat, the US dollar on a trade-weighted basis will dip into negative YoY territory in 2Q14E and will remain negative through 3Q14E, only returning to marginally positive by 4Q14E. This is a sharp deterioration from the +3-4% trend we’ve seen since the start of 1Q13. That should provide a material shock to the rate of change in import price inflation, which, at -0.3% YoY, is currently accelerating off the lows of late-2013 (-1.8% YoY in NOV).

TWO: We do not, however, think it’s prudent to hold current market prices flat. While most of Wall St. continues to anticipate higher rates amid tighter policy out of the Federal Reserve, we believe rising inflation will continue to slow consumption growth at the margins – which is ~70% of US GDP. That, coupled with the precipitous decline in both activity and price appreciation in the housing market, should eventually force the Fed to pare back their guidance on eventual monetary tightening. A cessation of their existing policy to taper is not out of the question by the third quarter. Commodities, which hold a -0.70 correlation to the USD (CRB Index vs. US Dollar Index; trailing 6M), should continue to grind higher. It’s worth noting that the CRB Index is up +9% YTD, besting the sub-6% return for the S&P 500.

THREE: If none of our market-based forecasts come to fruition, we still have confidence in CPI accelerating over the intermediate term – if for no other reason than base effects. Without getting too geeked out on differential calculus, “simple” math would suggest that as comparative base rates decline sequentially – which they do throughout the balance of the year – the probability that the rate of change accelerates from the base rate (i.e. t₀) increases substantially.

LONG-TERM (TAIL) (the next 3 years or less)

In line with our #StructuralInflation macro theme (introduced in APR ’14), we continue to think structural inflationary pressures are building up across the US economy. While we cede the point that considerable slack remains in the labor market, we do not think investors are paying nearly enough attention to the following supply-side pressures that are likely to perpetuate cost-push inflation over the long term:

- S = I. Savings equals investment. That’s the most basic, underappreciated formula in all of the borderline useless economic theory we’ve all had the “great privilege” of learning. With rates being held at zero for such a long time, it should come as no surprise that real nonresidential fixed investment is up only +3.3% on a trailing 5Y CAGR basis. That’s the slowest rate of growth this far into an economic expansion over at least the last 30Y.

- Again, when the central bank cuts rates to zero and leaves them there for the better part of six years, savings are naturally pulled from traditional investment vehicles that encourage investment (i.e. bank deposits) and into investment vehicles that actually encourage disinvestment – such as MLPs – in search of higher yields. Duh. Moreover, corporations – which have been increasingly rewarded by investors to buy back stock and ramp dividends – have largely done so in lieu of investing in their businesses. Now, as we approach what may be the end of economic cycle, many corporations streamlining trailing peak GDP growth rates and are scrambling to ramp up production into the inevitable result of seven years worth of broad SG&A deleveraging: limited production, transportation and storage capacity.

- Q: What happens when company A acquires company B in industry C? A: There are fewer companies operating in industry C, effectively creating marginal headroom for company A to hike prices on its customers. This phenomenon has been happening all throughout the post-crisis era and is now accelerating to a hilt here in 2014. The total number of domestic enterprises has declined -6% since the pre-crisis peak, with larger firms leading the decline at -10%. For example, Airlines and Hotels are two obvious industries in which consumers are feeling the pricing pinch of decreased competition. Newsflash to domestic equity bulls: you can’t be long the Airlines on a tired industry consolidation thesis and say that there’s [going to be] no inflation. That’s disingenuous at best…

CONCLUSION

Buy TIPS. Protect you and your loved ones from a likely acceleration in inflation. Please note that we are not making a hysterical call for hyperinflation born out of serial money printing. That’s not our style. Rather, our style is to call it like it is: the US economy is likely to experience a run-of-the-mill pickup in reported inflation. A 3-handle on headline CPI – which remains a conflicted and compromised calculation – is probable over the intermediate term.

Inflation tripling, lol!

Darius Dale

Associate: Macro Team

ONE-YEAR TRAILING CHART