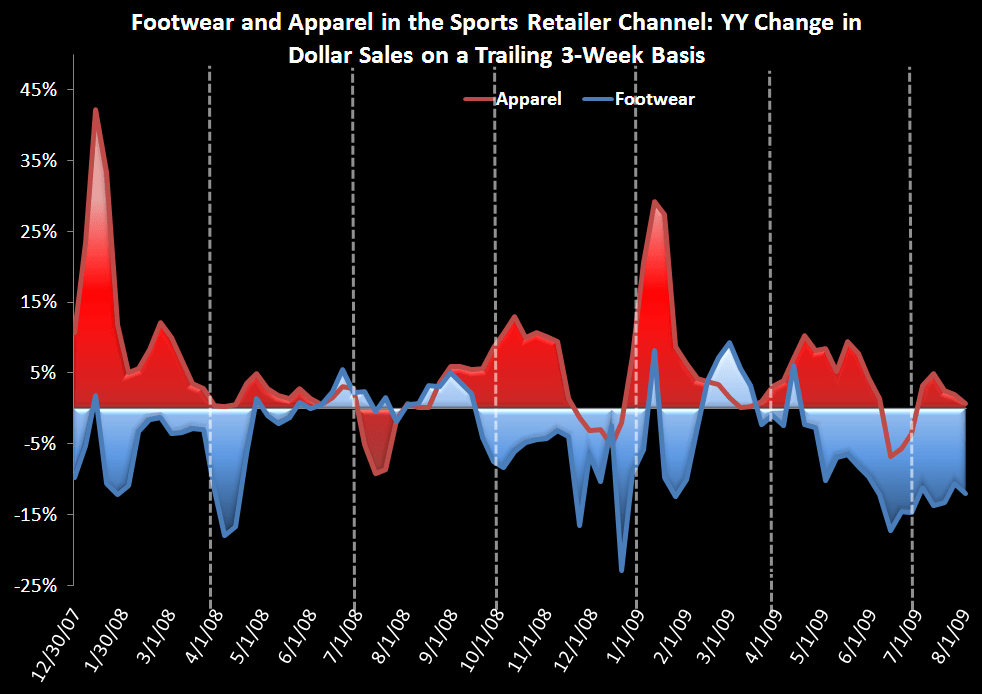

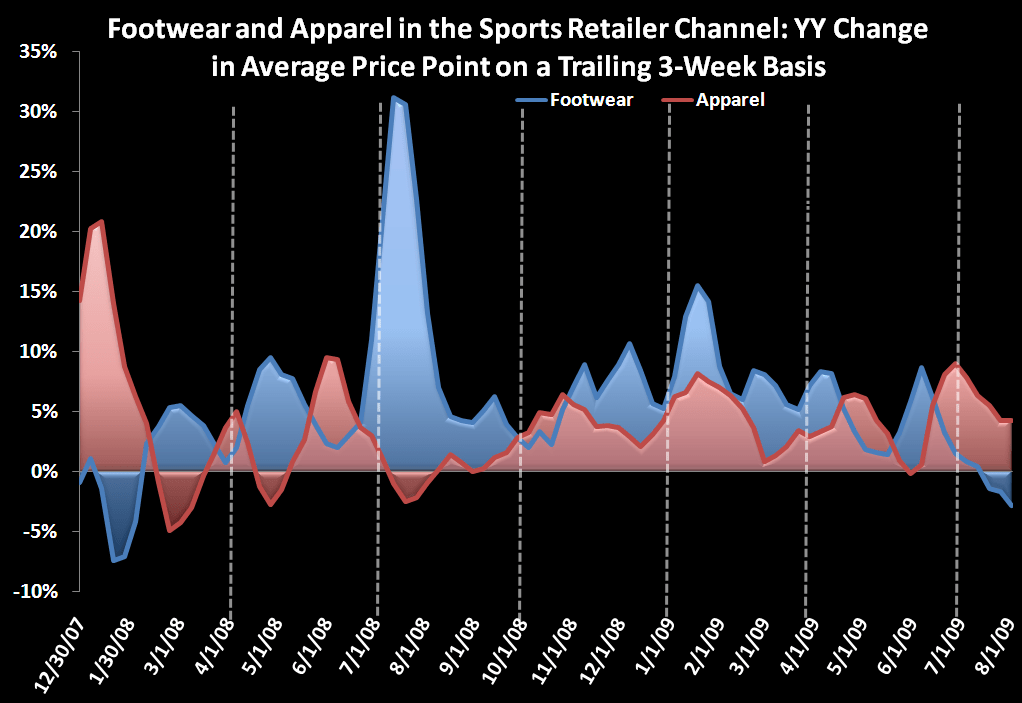

After getting a relatively positive read on athletic apparel earlier today, it appears that footwear did not follow suit. For the latest week, athletic footwear in the sporting goods channel decelerated significantly. Units and ASP’s both showed a sharp deceleration in trend vs. prior weeks. The move in ASP’s is a trend we’re watching closely. Anecdotally, the promotional environment as well as the major shifts in product mix remain stable. However, this data point certainly challenges these observations. It is still too early in the back to school season to suggest that promos will ramp up aggressively or beyond plans, but a prolonged negative trend in units and ASP’s would warrant some changes at retail. With inventories still tight on and off the mall, a promotional ramp up would be a large departure from the relatively “stable” environment we have enjoyed for the past two quarters.