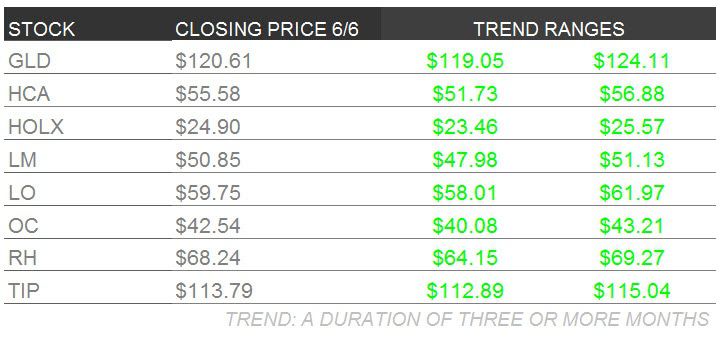

Below are Hedgeye analysts' latest updates on our EIGHT current high-conviction investing ideas and CEO Keith McCullough's updated levels for each.

*Please note we added TIP and removed ZQK from Investing Ideas this week.

We also feature three institutional research notes from earlier this week which offer valuable insight into the markets and economy.

Trade :: Trend :: Tail Process - These are three durations over which we analyze investment ideas and themes. Hedgeye has created a process as a way of characterizing our investment ideas and their risk profiles, to fit the investing strategies and preferences of our subscribers.

- "Trade" is a duration of 3 weeks or less

- "Trend" is a duration of 3 months or more

- "Tail" is a duration of 3 years or less

HEDGEYE CARTOON OF THE WEEK

IDEAS UPDATES

GLD – On Wednesday afternoon we reiterated our call to buy Gold ahead of the ECB meeting which was anticlimactic relative to expectations.

The ECB made the following rate cuts:

- Benchmark Rate Cut from 0.25% to 0.15% (0.10% estimated)

- Marginal Lending Facility from 0.75% to 0.40% (0.60% estimated)

- Deposit Facility from 0.0% to -0.10% (-0.10% estimated)

After the announcement at 7:45 a.m., the Euro (ETF: FXE) opened down -0.35% from its Wednesday close and moved higher throughout the day to close +0.43% on the session. Gold (ETF: GLD) rallied on the announcement and closed +0.75% on the day. Gold is up +0.55% week-over-week, and we remain long into the Fed policy meeting on the 18th.

Because we believe Gold is a hedge against the expectation for forward-looking dollar devaluation, Gold’s strong correlation to the Euro as soon as Mario Draghi mentioned a potential asset purchase program back in February is not the least bit surprising.

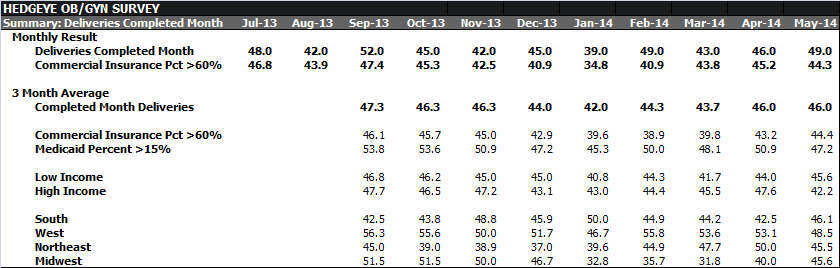

HCA – We’ve been attempting to measure deliveries with a monthly survey of OB/GYNs. Our May/June survey shows a modest improvement, but deliveries reported by the surveyed OB/GYNs continue to decline year over year. The results have been consistently showing a decline over the last several months despite comments from hospital companies, including HCA Holdings, and data from the US Census showing that births accelerated in 4Q13 with growth continuing into 1Q14.

The US Census will update their data for May by the fourth week of June, giving us what would appear to be the most accurate indication of maternity trends. We continue to track these data closely as maternity is the largest contributor to inpatient admissions.

HOLX – The monthly OB/GYN survey of Pap utilization shows we are on track with our estimate of an annual rate of decline of -10% for Hologic’s ThinPrep franchise. While some physicians are seeing volume decline at 20% or more in some cases, there are many others who are already compliant with the 2012 Cervical Cancer Screening Guidelines, or at the other extreme will never reach 100% compliance of testing every 3 years.

Patient volume weakened somewhat sequentially, particularly among commercially insured patients. Medicaid volume remained positive, likely supported by the ACA. Regionally, the Midwest was particularly weak relative to other regions.

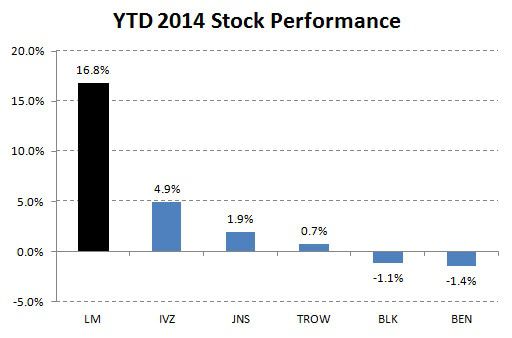

LM – Shares of leading bond fund manager Legg Mason had another good week rising 4% as the hunt for yield among stocks and bonds continued. With the European Central Banks cutting rates again, the outlook for most global paper brightened as when an important developed market lowers prevailing interest rates, existing fixed income can appreciate.

Legg Mason also sold a small sub-scale asset management division to Stifel & Co. during the course of the most recent 5-day period which relays that LM management is focused on delivering strong shareholder returns by selling non-core assets and executing share repurchases and dividend hikes. The year-to-date outperformance of an investment in Legg Mason is undeniable with LM shares now up over 16% in 2014, some 11 points higher than the next best performing asset management stock.

We still like the long position until Street consensus recognizes this out of favor investment.

LO – The stock pulled back off all-time highs this week on no new news events. For yet another week the investment community is wondering if Lorillard will be taken out, likely by Reynolds American (RAI).

We continue to suggest that investors hold this stock into potential news of the buyout or until our long-term fair value price of the stock at $80/share is realized. And we continue to assert that the company’s powerful earnings generation is anchored on its advantaged tobacco and e-cigarette portfolio.

Bottom line: we do not think LO will be imminently purchased and are staying long the stock that we added to Investing Ideas on 3/7/14.

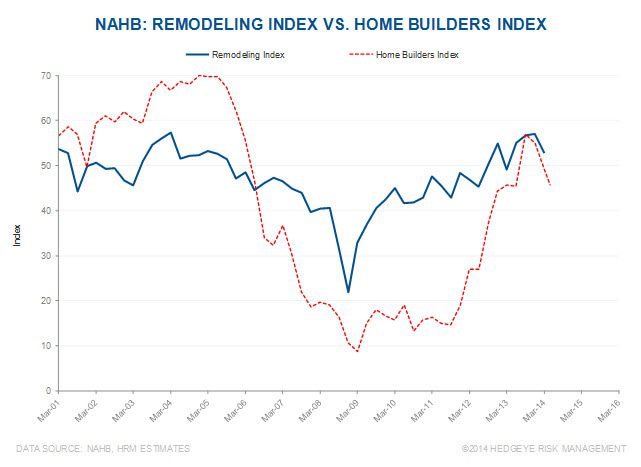

OC – Owens Corning’s roofing & insulation segments draws more revenue from the renovation/repair segment versus raw housing starts. This makes intuitive sense as weather, plus wear and tear, occurs more frequently than construction of new homes.

Looking at the graph below, the variance between NAHB’s Remodeling Index and the Home Builders Index is easily noticeable. The Home Builders Index fluctuated from 8 to 70 compared with 21 to 57 for the Remolding Index. In other words, the remodeling market is less cyclical than the housing market, which should provide Owens Corning with stable earnings compared to housing related names such as Lennar, D.R. Horton, and KB Homes.

RH – Restoration Hardware reports earnings Wednesday, June 11th after the close, and we are expecting revenue growth in the high teens. This is a tale of two halves for RH, with square footage growth weighted towards the back half of the year and the anniversary of the change in Source Book strategy starting in 3Q.

Our model is calling for low 20% revenue growth in the first half compared to high 20% in the back half, and 25% for the full year. That coupled with slight margin expansion puts us significantly ahead of the street for the both the first quarter and the balance of the year.

TIP – Hedgeye's macro team added the iShares TIPS Bond ETF to Investing Ideas this week. Click here to read the full report from macro analyst Darius Dale.

* * * * * * *

Click on each title below to unlock the institutional content.

Macro analyst Darius Dale takes a look at why it remains unlikely that he sees anything resembling meaningful monetary stimulus in China over the intermediate term.

Corelogic Data for May Show Housing Is Slowing Rapidly

Hedgeye's Housing team analyzes CoreLogic's May HPI report, which showed further marked deceleration in the rate of home price growth nationally.

Industrials analyst Jay Van Sciver explains why ISM Manufacturing new orders continues to imply that the 1Q 2014 slowdown was a bit more than just weather.