We pulled MCD from the Hedgeye Best Ideas list as a short on 2/14/2014 at $94.17/share, largely due to an underleveraged balance sheet and the potential for shareholder friendly financial engineering.

Today, McDonald’s management revealed several new initiatives the company will undertake to enhance shareholder value:

- Optimize the capital structure

- Optimize the ownership structure

- Scrutinize G&A

The company expects to return $18 to $20 billion to shareholders between 2014 and 2016 through a combination of dividends and share repurchases, representing a 10% to 20% increase over the amount of cash returned between 2011 and 2013.

McDonald’s CFO Pete Bensen stated, “Our 3-year cash return target is based on several activities including the significant free cash flow generated from our operations, as well as the use of cash proceeds from our debt additions and refranchising activity.”

Hedgeye — McDonald’s stated back in March that it was looking at ways to “optimize [its] capital structure” to create value. We find today’s news disappointing, as we believe the company could leverage its balance sheet significantly more. We have always felt that any financial engineering event would only be a temporary boost to the stock given the decelerating sales environment.

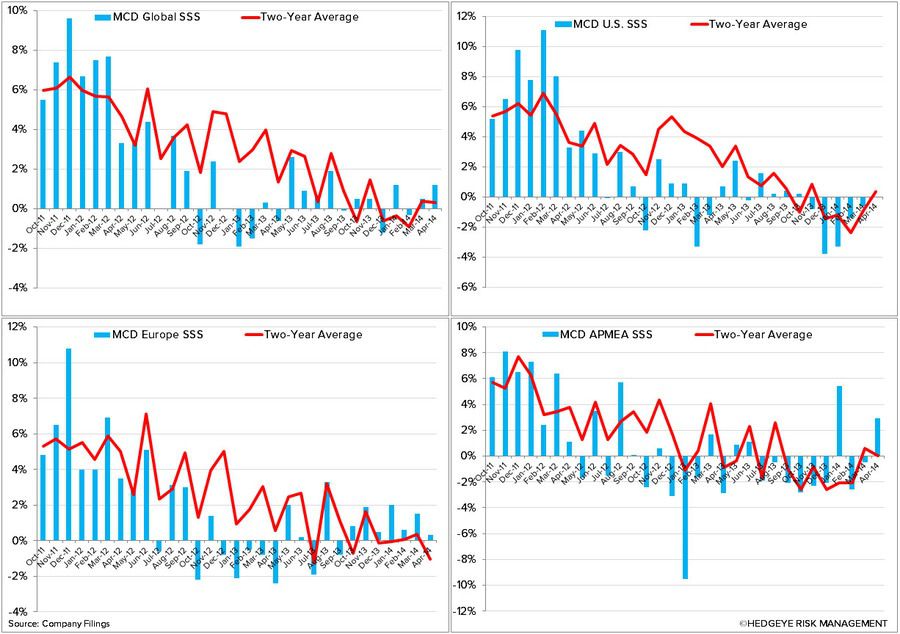

On June 9th, MCD will release its May sales data. Our current read is that sales trends will be uninspiring, even with the rollout of the high density tables. With the financial engineering news in the rear view mirror, we’d be tempted to revisit our short thesis in the coming months. The company plans to report 2Q14 results on July 22nd.

Howard Penney

Managing Director

Fred Masotta

Analyst