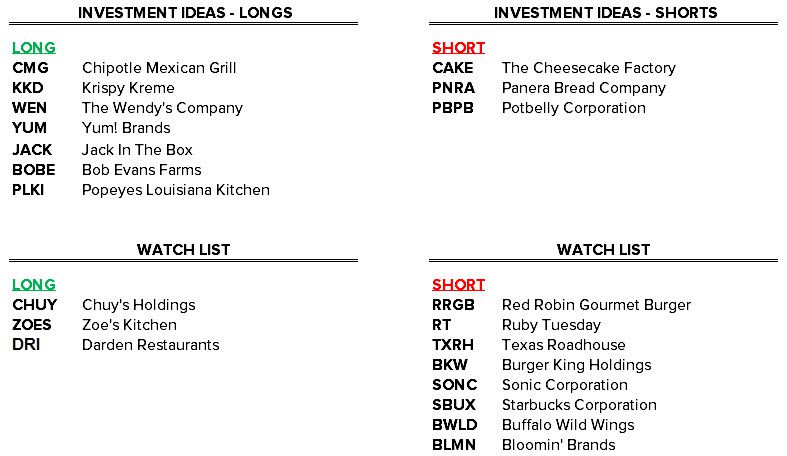

Investment Ideas

The table below lists our current Investment Ideas as well as our Watch List – a list of potential ideas that we are in the process of evaluating. We intend to update this table regularly and will provide detail on any material changes.

DRI: We’re relegating Darden to the Watch List as a long following the Red Lobster fire sale. We need to see the majority of senior management and the Board replaced before we can have high-conviction in our bullish thesis. Starboard will seek to replace the entire Board at the company’s annual meeting later this year and has nominated a highly qualified slate of replacements. While this may seem unusual and quite aggressive, we firmly believe Starboard could be successful in this attempt. Until then, however, we’d be cautious as FY14 and FY15 earnings estimates will be revised down and lingering uncertainty could be a drag on the stock.

Recent Notes

05/19/14 Monday Mashup: Darden Sells Red Lobster

05/20/14 BNNY: Reiterating Short Into Earnings

05/21/14 DRI: Simply Egregious

Events This Week

05/28/14 CBRL Earnings Call 11am EST

05/28/14 DIN Annual General Meeting 12am EST

05/28/14 WEN Annual General Meeting

05/29/14 PLKI Earnings Call 9am EST

05/29/14 CAKE Annual General Meeting 1pm EST

05/29/14 BNNY Earnings Call 5pm EST

05/29/14 RUTH Annual General Meeting

Chart of the Day

DFRG (15.02x TTM EV/EBITDA) two-year same-store sales have been on the decline since 3Q11, yet the fine dining steak chain is up +40.6% over the past year and trades at a substantial premium multiple to its most comparable peer RUTH (9.43x TTM EV/EBITDA).

Recent News Flow

Monday, May 19th

- BLMN closed debt refinancing, effectively lowering its interest rate. The Company expects cash interest savings of approximately $6.0 million in FY14. The savings from the refinancing will be used primarily to fuel the development of a second concept in Brazil, where Outback Steakhouse has had great success.

- DRI Barington Capital publicly opposed the Red Lobster sale, citing concerns with the cheap sale price and the highly tax inefficient transaction. Barington was clearly displeased with the Board, writing: “It is clear to us from the Board’s decision to pursue this imprudent transaction and its horrific record in the area of corporate governance, that Darden’s independent directors are neither focused on, nor responsive to, shareholder concerns. In over 14 years of investing, we have never seen a group of directors that have allowed a company to be run with such a blatant disregard for shareholder interests.”

- BWLD announced the opening of a multi-level, 15,000 square foot restaurant in Times Square.

- DNKN appointed Irene Chang Britt to its Board of Directors. Ms. Chang Britt is currently President of Pepperidge Farm and serves as Senior Vice President, Global Banking and Snacking for Campbell Soup Company. Prior to joining Campbell in 2012, she held senior positions with Kraft Foods and Kimberly-Clark.

- CAKE entered into an exclusive licensing agreement with Maxim’s Caterers to development at least 14 restaurants over the next 10 years throughout Hong Kong, Macau, Taiwan and the People’s Republic of China with the potential to expand into Japan, South Korea, Malaysia, Singapore and Thailand. According to the release, the first restaurant will open in FY15.

Tuesday, May 20th

- DRI Credit Suisse maintained its underperform rating and lowered its PT from $48 to $46 following the Red Lobster transaction.

- PBPB appointed Susan Chapman-Hughes, current Senior Vice President of U.S. Account Development Global Corporate payments at American Express Company, to its Board of Directors.

Wednesday, May 21st

- DRI Starboard Value announced its intention to replace Darden’s entire Board of Directors.

Thursday, May 22nd

- BJRI announced the opening of its newest, 8,500 square foot restaurant in West Palm Beach, Florida. BJ’s now has 17 restaurants in the state of Florida.

Friday, May 23rd

- TXRH announced a quarterly cash dividend of $0.15 per share and increased its share repurchase authorization to $100 million.

- WEN introduced a new summer-LTO, the Steakhouse Jr. Cheeseburger Deluxe. According to the release, “The new limited-time cheeseburger boasts a fresh, never frozen beef hamburger patty seasoned with steakhouse seasoning, melty cheese and a creamy garlic aioli sauce made with roasted garlic, onion and Dijon mustard. The hamburger patty is topped with sliced red onion, hand-cut tomato and hand-leafed lettuce.” The burger, which is part of the Right Price Right Size Menu, costs $1.49 at participating locations.

US Macro Consumption

The XLY (+2.1%) outperformed the SPX (+1.2%) in a convincing manner last week. However, both casual dining and quick service stocks, in aggregate, underperformed the broader XLY index.

The Hedgeye U.S. Consumption Model is signaling bearish for the second week in a row, flashing red on 7 out of 12 metrics.

XLY Quantitative Setup

From a quantitative perspective, the sector is now bullish on an intermediate-term TREND duration.

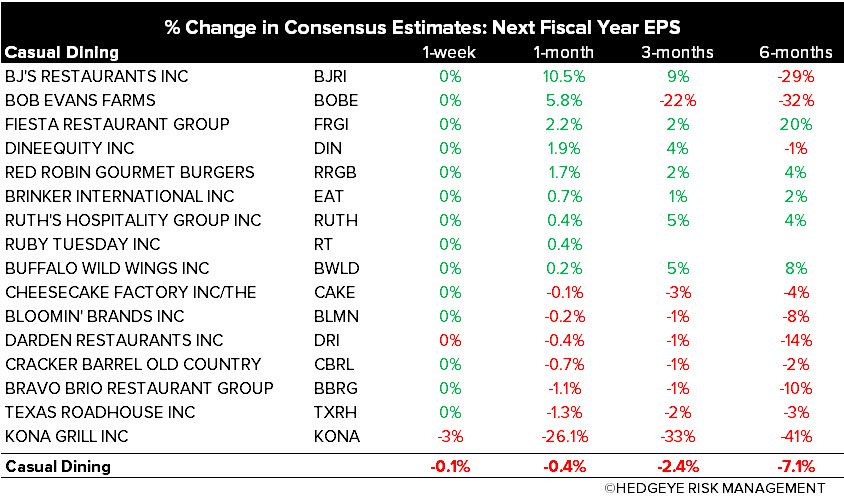

Casual Dining Restaurants

Quick Service Restaurants

Howard Penney

Managing Director

Fred Masotta

Analyst