Once again the weekly Macau numbers cannot be relied upon

According to the release, Macau generated HK$996m in average daily table revenue this past week, up 27% YoY, and bouncing back from last week’s daily of HK$886m. However, we believe both weeks were placeholders and cannot be relied upon. Week 2 of May generated revenues of HK$6.2m - the most common placeholder amount. This past week generated HK$6.975m which has also occurred too many times to be statistically random . We pointed out the placeholder concept in many notes over the past year. See "WE'VE BEEN PLACEHOLDERED!" from 04/29/14 for our latest thoughts.

Per usual when a month contains a placeholder week or two, the last week is volatile. If the month to date numbers were accurate, May would be tracking to finish the month up mid teens YoY. However, we expect a big catch up in the final week and still believe May could come close to our 20% growth target.

Anecdotally, we're hearing the Mass floors are busy and Premium Mass is doing well. Mixed reports on VIP but overall, volumes appear decent.

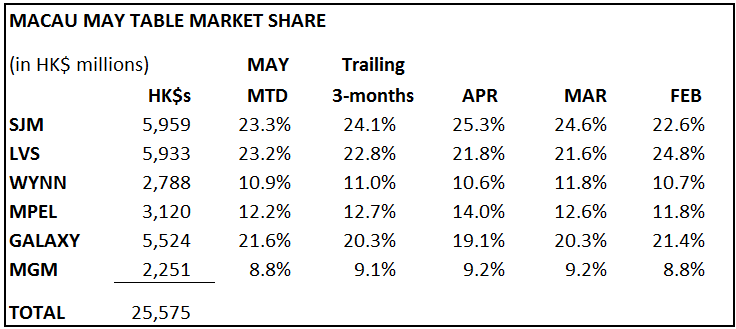

In terms of market share, Galaxy is the only significant outlier with share well above recent trend. MPEL and SJM remained below their respective 3 month average market share trend.