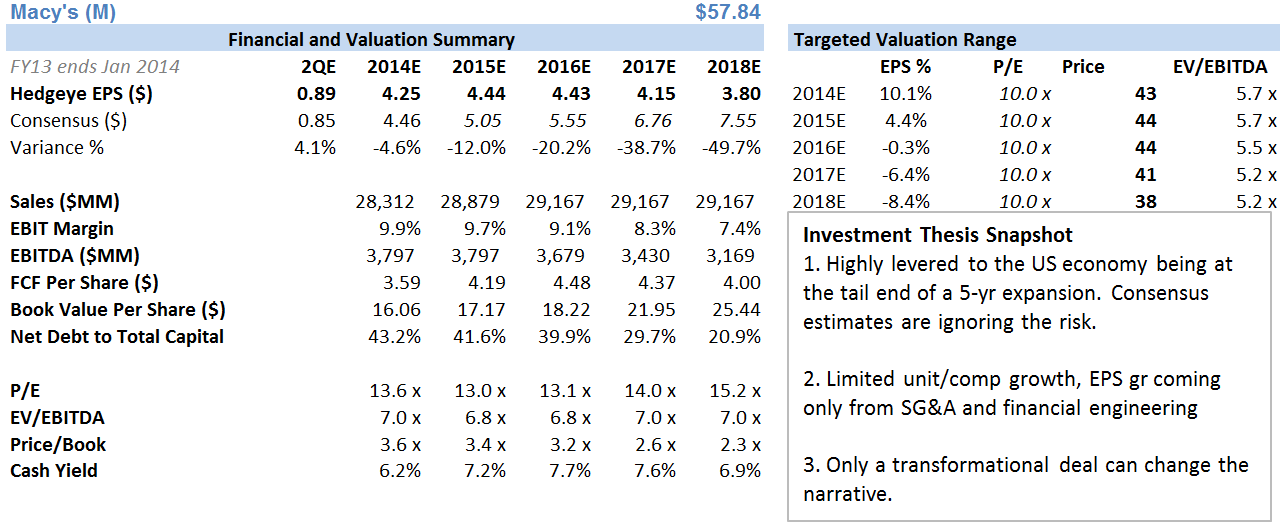

Conclusion: We think Macy’s is at a critical point in its decision tree. The company printed a 1Q growth algorithm that is typical with what we’d expect from a dinosaur department store – negative comps (-1.6%), lower gross profit dollars (-1.3%), but modest growth in EBIT (+1.8%) due to lower SG&A spending. All in, about 800bps of Macy’s 9.3% EPS growth came from financial engineering via share repo. The company is going to have a better 2Q due to the timing of a major promotion and what we agree will be a little snap-back in spending from depressed winter levels. We get the whole ‘best in breed’ thing (sort of), but past a good 2Q, we think that investors should be asking themselves what they’re really in this name for. Is this a breed you need to own? Even Macy’s CFO, who we actually think is very good, used the word ‘hope’ on the conference call not once, not twice, but FIVE times when referring to recovery in different parts of Macy’s business in 2H. They’re allowed to hope. But in modeling out a cash flow trajectory, we’re not. Once 2Q earnings is past us, we’d look to short this one aggressively.

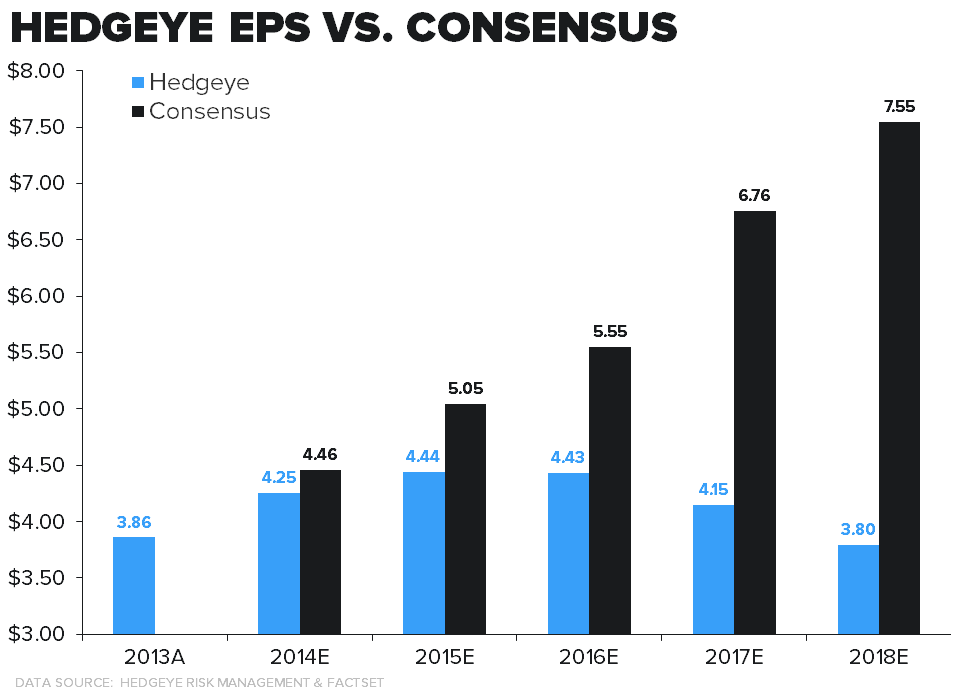

We’re coming in about 4.6% below consensus for this year – at $4.25. We think that M will beat 2Q, and then miss 2H. That’s something to keep in mind regarding near-term positioning. But it’s not the near-term that really worries us. We’re looking out across our five-year model, and we have EBIT down every single year, with stock repo and repayment of debt maturities making up the difference to keep EPS relatively flat. If we’re right, then we’re looking at an annuity of $4-$4.25 in EPS. Let’s capitalize that by a 10% cost of equity and it suggests a stock in the low $40s. If you want to use a 10x multiple instead, you get the same value (M has traded below 8x earnings in the past). This low $40s value comes out to about 5.7x EBITDA, which is hardly a trough level one might expect from a retailer with zero square footage growth.

We understand all the hype around company initiatives like My Macy’s, MAGIC, etc…these are all what makes Macy’s the leader in the space. But the reality is that we are officially in year six of an economic recovery, and the department store group has never gone more than five consecutive years of margin expansion without a material decline in margins.

The bigger concern is not a 5% EPS miss for this year, but a 50% miss in year 5. The Street’s numbers not only dismiss the potential for a near-term margin correction, but they assume we go ANOTHER five years with the business and retail cycle improving. If this actually happens, then yes, you will probably make a lot of money in Macy’s. But you’ll probably make more in high-quality growth names in the consumer space that have recently been annihilated.

One thing that we wonder about Macy’s is what it does strategically if a) this year does not pan out as planned, and b) 2015 looks even more challenging. In years past, whenever Macy’s ran into a problem, it acquired another department store chain to eventually assimilate under the Macy’s banner. It’s a strategy that worked. But with a National footprint, coverage at the high end (Bloomingdales) and in the middle/upper-middle (Macy’s), it really has no other physical retailer to buy. That’s what makes us think about the potential for Macy’s to either do a transformational dot.com merger, or gobble up smaller e-commerce business that have earned the consumer’s respect in a different segment. We’re thinking of names along the lines of GILT, Bonobos, and others (some which trade publicly). It’s unlikely that any such deal would be accretive for Macy’s given the multiple disparity, but we wouldn’t put it past M to go this route. Something to chew on.