Research Edge Position: Long Germany (EWG), Short Italy (EWI)

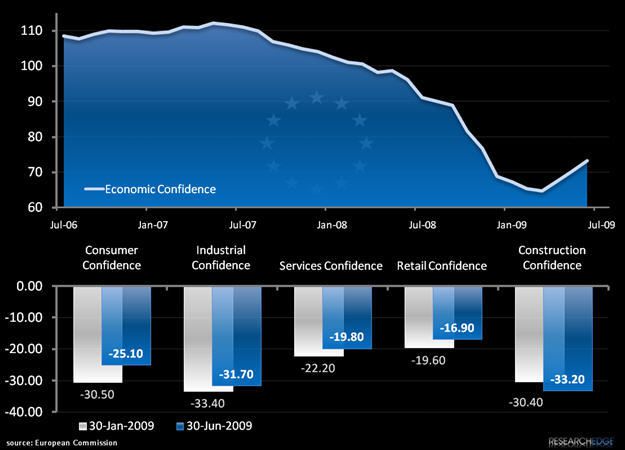

Today the European Commission reported that European confidence improved to 76 in July from 73.2 in the previous month, confirming the improvement in sentiment across many individual country indices that were released this week and adding a metric to compare the relative health of the region. We continue to hold that European countries will yield uncorrelated returns due to unique underlying fundamentals; we’re currently long Germany via the iShares etf EWG and short Italy via EWI in our model portfolio with the thesis that in aggregate countries with economic leverage will outperform those with financial leverage. [See our recent posts on the portal for more on our fundamental views on Germany and Italy.]

This week we noted in our post ‘”Shoots” in Europe?’ that PMI improved in the Eurozone for the manufacturing and service industries, and that Germany and France, the region’s two largest economies, registered improved consumer and business confidence numbers in July, with sequential improvement over the last three months. These forward-looking data points from the economic heavyweights are positive as European countries are highly tied to the Union as a main trading partner, yet we still expect slow improvement across the region. It’s worth calling out that European retails sales (a lagging indicator) fell for a 14th month in July. Individually, German retail sales rose, while sales in France and Italy fell, according to Markit Economics. We continue to hold that German and French consumers will benefit from a low CPI/interest rate environment as we move out in the intermediate term, with June CPI at 0.0% in Germany and -0.6% in France, whereas inflation in Italy came in annually at +0.6% in June .

Noteworthy, today Germany released that the number of people out of work increased by 52,000, yet the adjusted jobless rate remained unchanged at 8.3% in July. While we expect this number to push out in the intermediate term, the stability of the number (though lagging) is bullish. As a long term risk we continue to highlight Germany’s depressed export picture, yet an increase in Factory Orders at +4.4% M/M in May and demand from China are early positive indicators. Further, we believe that the country’s powerful manufacturing capacity remains a primary structural advantage when compared to its European peers. As of late there’s been increased speculation that lending in Germany could tighten as a result of the merger of the country’s big banks, Commerzbank and Dresdner Bank, due to obligations under European state-aid rules to shrink its balance sheet in return for the hand-out it received. We’ve seen no confirmation of this from the Bundesbank.

Our bearish view on Italy remains. Recently the Italian research institute Isae forecast the economy to contract 5.3% this year (matching an estimate by the OECD), from a previous estimate of 2.6%. Fundamentally we believe that Italy’s general government debt, which stands at over 100% of 2008 GDP as compared to 65.9% for Germany and 68.1% for France, will remain a stumbling block to its economic recovery. The spread on 10-year Italian Treasuries versus the German 10Y stands at 83bps, off from a high of 120bps for the month of July, but still suggest a risk aversion from investors.

And finally, UniCredit, Italy’s largest bank, may struggle to see a profit as it works through bad loans, which could have an adverse tail for lending. We’ll know more when the bank reports Q2 earnings on August 4th. From a quantitative set-up, the Italian ETF holds a substantial amount of Financials (43.10%).

As we continue to monitor the European patient we’ll be focused on the individual performance of countries. For now we’re paired off long Germany, short Italy.

Matthew Hedrick

Analyst