TODAY’S S&P 500 SET-UP – May 8, 2014

As we look at today's setup for the S&P 500, the range is 29 points or 0.92% downside to 1861 and 0.63% upside to 1890.

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.19 from 2.22

- VIX closed at 13.4 1 day percent change of -2.90%

MACRO DATA POINTS (Bloomberg Estimates):

- 7am: BOE benchmark rate decision; est. 0.5% (prior 0.5%)

- 7:45am: ECB benchmark interest rates decision; est. 0.25% (prior 0.25%)

- 8:30am: ECB’S Draghi holds press conf. after rate decision, see LIVE <GO>

- 8:30am: Initial Jobless Claims, May 3, est. 325k (prior 344k)

- Continuing Claims, April 26, est. 2.758m (prior 2.771m)

- 9:45am: Bloomberg Consumer Comfort, May 4

- 8:am: Fed’s Plosser speaks in New York

- 8:30am: ECB’s Draghi holds news conference in Brussels

- 9:25am: Fed’s Evans speaks at Chicago banking conference

- 9:30am: Fed’s Tarullo speaks at Chicago banking conference

- 9:30am: Fed’s Yellen testifies to Senate Budget Committee

- 10am: Freddie Mac mortgage rates

- 10:30am: EIA natural-gas storage change

- 2pm: Fed’s Bullard speaks at conference in St. Louis

GOVERNMENT:

- 9:30am: Yellen testifies before Senate Budget Cmte

- 9:30am: Time Warner Cable Chairman Marcus, Comcast EVP Cohen at House Judiciary Cmte on merger

- 10am: Treasury’s Lew annual testimony on intl finance system before House Financial Services Cmte

- 10am: Senate Health and Education Cmte hears from HHS Sec. nominee Sylvia Burwell

- 1:15pm: Agriculture Sec. Vilsack announces “historic” USDA support for local food systems on media call

- U.S. ELECTION WRAP: Chamber Beats Tea Party in N.C.; Ad Buys

WHAT TO WATCH:

- Fed Chair Janet Yellen testifies before Senate Budget Cmte

- FOMC’s Evans, Plosser, Tarullo to speak in Chicago, New York

- Barclays plans to cut 7,000 jobs at investment bank by 2016

- AT&T said to hold talks with DirecTV over acquistion

- Montebourg prefers Siemens alliance over GE takeover: FAZ

- JPMorgan wins dismissal of MBIA suit; case may be refiled

- Web cos. see grave threat with FCC’s fast-lane plan for ISPs

- Yahoo CEO sees more web traffic via mobile vs PC by end-2014

- Ford to buy back $1.8b in stock to offset grants, converts

- Samsung replaces mobile design execs. on flagging phone sales

- UPS seen matching FedEx’s size-based pricing formula

- Deutsche Telekom using cash for U.S. unit affects earnings

- Sheldon Adelson ready to put fortune against Internet gambling

- Macau casino cos. drop on capital-outflow restrictions report

- Cogent’s Schaeffer says Comcast-TW merger will mean mkt abuse

- April U.S. retail sales likely to be ‘good, not great’

- ECB will keep monetary policy unchanged, economists say

- U.S. disputes Putin claim of withdrawal from Ukraine’s border

- House Foreign Affairs Cmte holds hearing on Russia, Ukraine

AM EARNS:

- AES (AES) 6am, $0.27

- AMC Networks (AMCX) 7am, $1.14

- Ameren (AEE) 8am, $0.32

- American Realty Capital (ARCP) 6am, ($0.11)

- Apache (APA) 8am, $1.60 - Preview

- Athabasca Oil (ATH CN) 6am, (C$0.05)

- Cablevision Systems (CVC) 8:30am, $0.05 - Preview

- Canadian Tire (CTC/A CN) 7:46am, C$0.93

- Crescent Point Energy (CPG CN) 8am, $0.32 - Preview

- DISH Network (DISH) 6:01am, $0.44 - Preview

- Fortis (FTS CN) 7am, C$0.64

- Great-West Lifeco (GWO CN) 12:44pm, C$0.60 - Preview

- IntercontinentalExchange Group (ICE) 7:30am, $2.61

- Liberty Interactive (LINTA) 7:30am, $0.24

- Liberty Media (LMCA) 7:30am, $0.70

- Louisiana-Pacific (LPX) 8am, ($0.06)

- Mallinckrodt PLC (MNK) 7am, $0.77

- Nationstar Mortgage (NSM) 6am, $0.74

- Priceline Group/The (PCLN) 7am, $6.84

- Quebecor (QBR/B CN) 6am, C$0.30

- Regeneron Pharmaceuticals (REGN) 6:30am, $2.27 - Preview

- Sarepta Therapeutics (SRPT) 7am, ($0.81)

- Scripps Networks Interactive I (SNI) 7am, $0.81

- SNC-Lavalin Group (SNC CN) 8:27am, C$0.46

- SunEdison (SUNE) 7am, ($0.18)

- Synta Pharmaceuticals (SNTA) 6:45am, ($0.30)

- TELUS (T CN) 8:30am, C$0.61 - Preview

- Teradata (TDC) 6:55am, $0.47

- Valeant Pharmaceuticals (VRX CN) 6am, $1.72 - Preview

- Visteon (VC) 6am, $0.60

- Wendy’s Co/The (WEN) 7:30am, $0.05 - Preview

- WhiteWave Foods (WWAV) 6am, $0.19 - Preview

- Windstream Holdings (WIN) 6:15am, $0.09

- WP Carey (WPC) 8am, $0.62

PM EARNS:

- AuRico Gold (AUQ CN) 4:37pm, ($0.02)

- Canadian Natural Resources (CNQ CN) 5pm, C$0.80 - Preview

- CBS (CBS) 4:01pm, $0.74

- Computer Sciences (CSC) 4:15pm, $1.04

- Credicorp (BAP) 6pm, $2.47

- Darling International (DAR) 4:30pm, $0.26

- Fifth Street Finance (FSC) 4:37pm, $0.26

- Great Plains Energy (GXP) 5:10pm, $0.19

- Hain Celestial Group/The (HAIN) 4pm, $0.86

- Jazz Pharmaceuticals Plc (JAZZ) 4:05pm, $1.87

- Medivation (MDVN) 4:10pm, ($0.08)

- Monster Beverage (MNST) 4:05pm, $0.49

- News Corp (NWSA) 4:05pm, $0.03

- Nuance Communications (NUAN) 4:01pm, $0.23

- Pembina Pipeline (PPL CN) 4:05pm, C$0.35

- Salix Pharmaceuticals (SLXP) 4:01pm, $0.91

- Scientific Games (SGMS) 4:12pm, $0.03

- Silver Wheaton (SLW CN) 5:06pm, $0.22

- Spectrum Pharmaceuticals (SPPI) 4pm, ($0.19)

- Symantec (SYMC) 4:01pm, $0.42

- Ubiquiti Networks (UBNT) 4:05pm, $0.49

- Zogenix (ZGNX) 4:01pm, ($0.15)

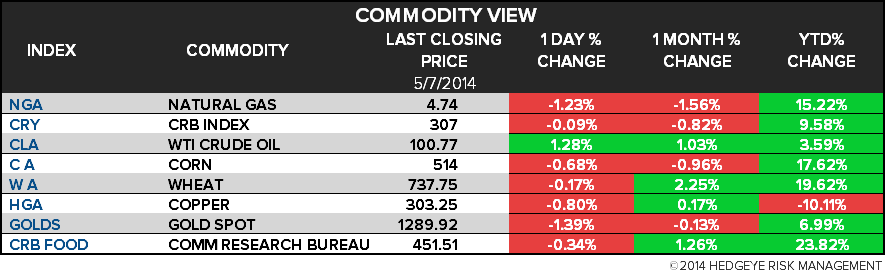

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Nickel at Two-Year High as Vale Suspension Fuels Supply Concern

- WTI Falls Most in Three Days After Supplies Drop; Brent Declines

- Wheat Surplus Eases Crop Risks From Ukraine to U.S.: Commodities

- World Food Prices Fall as Dairy to Vegetable Oil Costs Drop

- Gold Trades Near This Week’s Low as Yellen Weighed With Ukraine

- Wheat Extends Drop Before USDA Report as Ukraine Shipments Climb

- Coffee Drops as Rain Seen Helping Vietnamese Crop; Cocoa Falls

- World Ore Glut Outweighs Slowest China Growth Since ’90: Freight

- China Copper, Iron Ore Purchases Climb as Total Imports Increase

- Oil Industry Risks $1.1 Trillion of Investors’ Cash, Study Says

- Mine M&A May Double as China Returns in Coal to Copper Deals

- World Corn Harvest Seen Falling in 2014-15 by AMIS on U.S. Crop

- MORE: Russia’s Nickel Exports Declined 0.8% in 1Q as Values Fell

- Sugar Exports From India Slowing as Subsidy Delay Deters Buyers

CURRENCIES

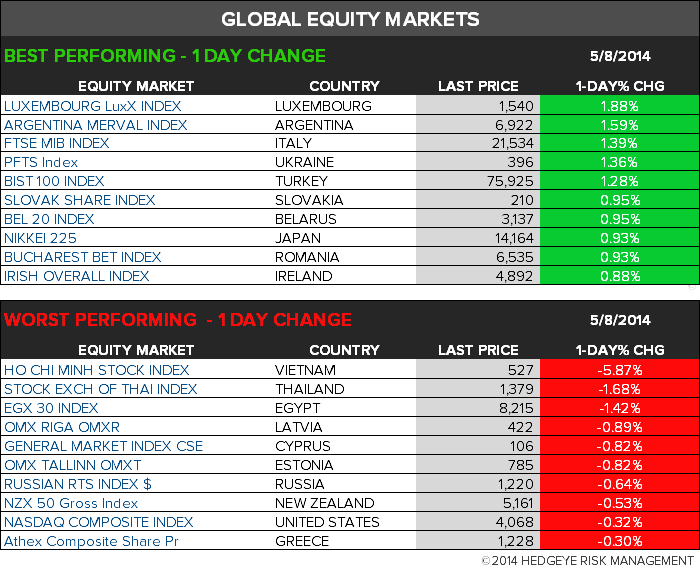

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team