*Reminder: We’re hosting a call with Pat Grismer, CFO of Yum! Brands, on Tuesday, May 6th at 11am EST to talk succession planning, Taco Bell breakfast and China.

Investment Ideas

The table below lists our current Investment Ideas as well as our Watch List – a list of potential ideas that we are in the process of evaluating. We intend to update this table regularly and will provide detail on any material changes.

BOBE – We’re adding Bob Evans to our Investment Ideas list as a long. Activist Sandell Asset Management has identified significant opportunities for value creation at the company. We, here at Hedgeye, tend to think BOBE would also benefit from a transition to an asset light model.

Recent Notes

04/28/14 Monday Mashup: Adding ZOES, BOBE to the Watchlist

04/30/14 PNRA: Much Noise, Little Clarity

05/01/14 YUM: Conversation with CFO About Succession Planning

05/02/14 New Best Idea: Long BOBE

05/02/14 Employment Data: Beyond the Headline Numbers

Earnings Calls This Week

05/05/14 TXRH earnings call 5:00pm EST

05/06/14 TAST earnings call 8:30am EST

05/06/14 ARCO earnings call 10:00am EST

05/06/14 FRGI earnings call 4:30pm EST

05/06/14 PBPB earnings call 5:00pm EST

05/06/14 CHUY earnings call 5:00pm EST

05/07/14 PZZA earnings call 10:00am EST

05/07/14 THI earnings call 2:30pm EST

05/08/14 WEN earnings call 10:00am EST

05/08/14 JMBA earnings call 5:00pm EST

05/09/14 BLMN earnings call 9:00am EST

Chart of the Day

Recent News Flow

Monday, April 28th

- PNRA downgraded to underperform at Longbow Research with a $138 PT.

- BOBE appointed new independent directors Kevin Sheehan, Kathy Lane and Larry McWilliams to its Board of Directors. Gordon Gee stepped down from the board effectively immediately, while Larry Corbin and Robert Lucas will be retiring from the board when their terms expire.

- BOBE Sandell essentially deemed BOBE’s announcement inadequate, calling it a “knee-jerk reactionary step.”

- PZZA Papa John’s aired a TV commercial featuring NBA All-Star Paul George of the Indiana Pacers promoting its new Sweet Chili Chicken Pizza.

Tuesday, April 29th

- THI launched its newest drink, Frozen Hot Chocolate, across all U.S. restaurants.

- PZZA declared a quarterly dividend of $0.125 per common share payable May 23, 2014 to shareholders of record at the close of May 12, 2014.

- DRI announced that Chief Restaurant Operations Officer, Dave Pickens, will retire effective May 23. DRI will not replace Pickens and plans to eliminate the position altogether.

Wednesday, April 30th

- RRGB announced it has signed purchase agreements to acquire 32 franchised restaurants in the U.S. and Canada for approximately $40M.

- NDSL announced the opening of its first MA location in Shrewsbury with franchisee operator, Hamra Enterprises.

Thursday, May 1st

- PNRA was upgraded to positive at Susquehanna with a $184 PT.

- YUM announced that Chairman and CEO David Novak will become Executive Chairman on Jan. 1, 2015, transitioning from his current role. At this time, Greg Creed, Preisdent of Taco Bell, will become the next CEO of Yum! Brands. Novak will then form the Office of the Chairman, which will include Sam Su (YUM Vice-Chairman and Chairman/CEO of the China Division) and Greg Creed. According to the press release, "This new Office of the Chairman will partner as a triumvirate on overall corporate strategy and leadership development to propel continued growth."

- JMBA is re-introducing its Fruit Refreshers with coconut water for the summertime. The Fruit Refreshers are available in three flavors: Pina Colada, Tropical Mango and Island Strawberry.

- KKD upgraded to buy at Sidoti.

Friday, May 2nd

- BAGL board authorized a $20M repurchased program.

- WEN new product team was honored with the Hot N’ Juicy Award for its Pretzel Bacon Cheeseburger.

- FRSH Papa Murphy’s IPO priced at $11.00 per share, at the low end of the expected $11.00 to $13.00 range and had an underwhelming day trading, up only +0.46% at the close.

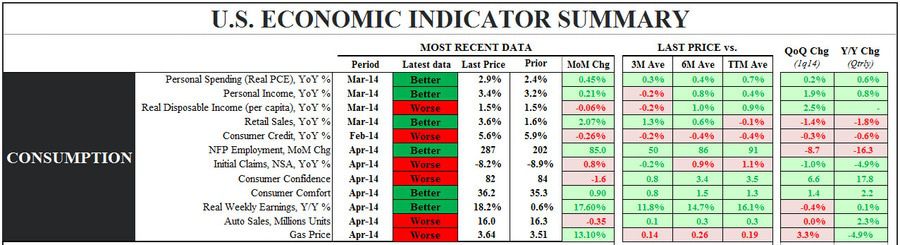

U.S. Macro Consumption

It was a bit of a bounce back week for consumer discretionary stocks. Following several weeks of underperformance, the XLY (+1.3%) outperformed the SPX (+1.0%) last week. In aggregate, casual dining stocks outperformed the broader index, while quick service stocks underperformed. The Hedgeye U.S. Consumption Model reverted back to neutral, now flashing green on 6 out of 12 metrics.

XLY Quantitative Setup

From a quantitative setup, the sector remains bearish on an intermediate-term TREND duration.

Casual Dining Restaurants

Quick Service Restaurants

Howard Penney

Managing Director

Fred Masotta

Analyst