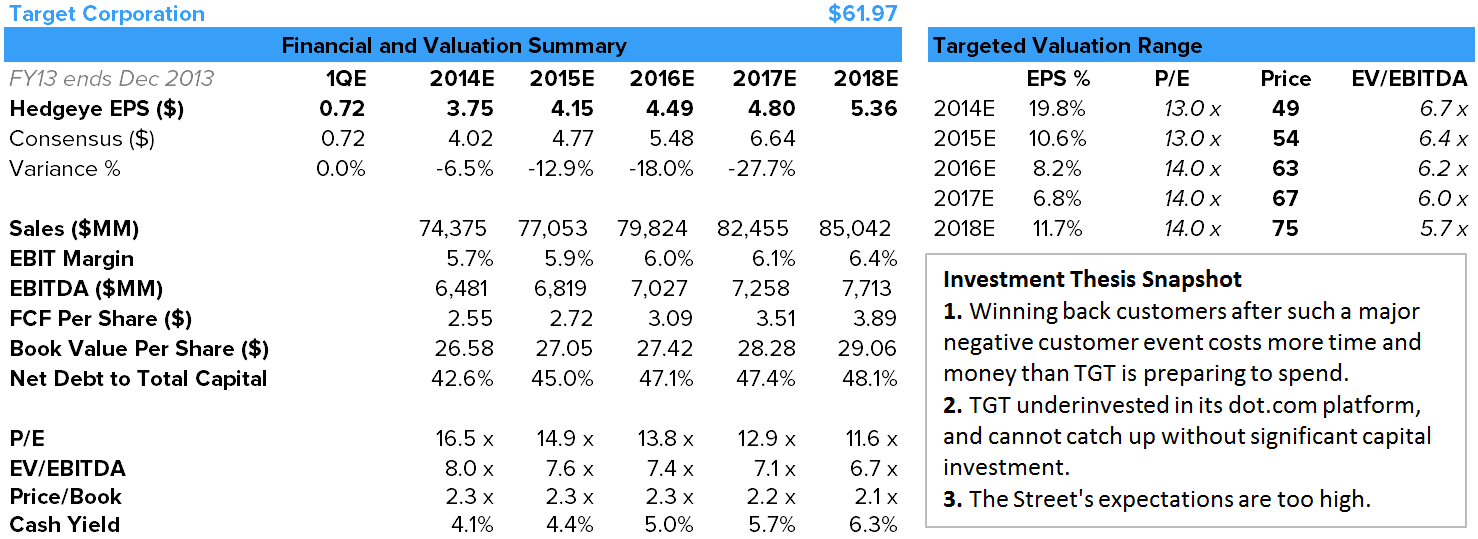

Conclusion: We’re short Target. We think that the model that management is selling to the Street leaves no room for error. Everything has to go right, and nothing can go wrong. We’re in the twilight of a department store margin cycle, margins are at peak, our proprietary survey shows that visitation at Target stores is down materially, and worse yet, the share appears to be going to Wal-Mart. We could make a case that target.com is one of the worst e-commerce businesses in retail, and it is certainly not making up for the shortfall in stores. Lastly, Canada expectations are extremely high, and our analysis of demographics around new Canadian stores leaves us with the view that management growth and profitability expectations are a pipe dream. In the end, we’re 27% below the consensus in year 3 of our model – which is a huge delta for this company. We get to downside to the high $40s ($13/14) if we’re right, but about $5/$6 upside if we’re wrong – that’s nearly 2.5 to 1. We’ll take that anyday on a sleepy mega cap retailer like Target.

Earlier this week, we published our 47-page deck on why we think Target is a short. We can’t print all the slides here, but here are five that we think are among the most notable.

1. The Macro Setup is not pretty. We just finished the fifth year of a margin expansion cycle for department stores. When we look back historically, we don’t think that there’s ever been a ‘year 6’. And by a country mile, we’re trading at peak valuations on these margins. The core of the TGT call goes far beyond this, but this is an extremely uninspiring backdrop.

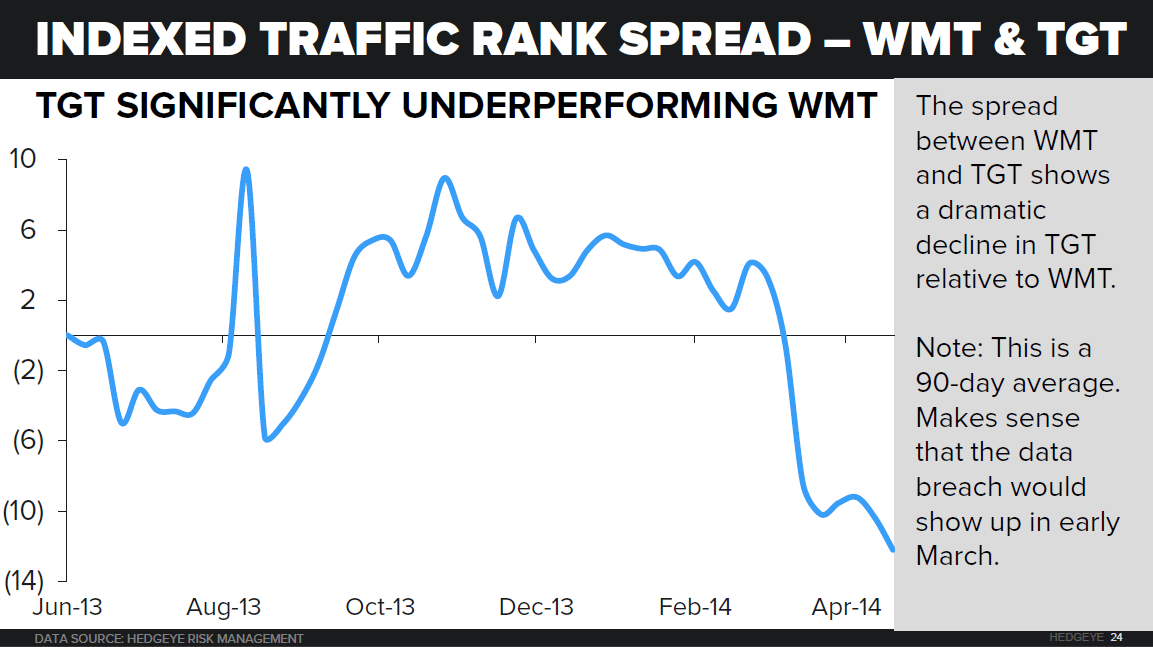

2. Visitation is down. We’re all tired of hearing about the Data Breach. But the reality is that the fallout is extremely notable. We just conducted our third Department Store consumer survey and we can gauge sequential changes in visitation intent on an absolute basis, and relative to other retailers. This shows how TGT went from 13 visits (TTM) in 3Q, to near 14 in 4Q (pre-Breach), to 11 today. That might not seem severe, but that’s 20% by our math.

3. Share is going to Wal-Mart. Not exactly the retailer we’d want to lose share to if we were Target. When WMT takes share, it has a tendency to not give it back. We have a lot of research in our deck that shows how consumers rank them on price, discounts, and product quality. The trends are compelling.

4. Dot.Com can’t save TGT. When other retailers get into trouble with their stores, often e-commerce makes up the difference. Our analysis of target.com’s traffic trends suggest that dot.com is performing just as poorly as the stores – if not worse. Based on our research, we can make a case that Target has one of the worst e-commerce businesses in all of retail.

5. Canada can’t save Target, either. We pulled up the lats and longs for both Canada and US stores, and then analyzed demographics in a 20-minute driving radius. Canada lacks the density and income characteristics around its stores that Target enjoys in the US. That’s not to mention that there is a cannibalization issue given that 11% of target customers already shop in Target US stores. Consensus revenue estimates assume that Target Canada outstrips share of wallet levels Target has in the US. The company’s guidance assumes productivity levels above US levels. We think both are extremely unrealistic.

Call replay can be accessed by clicking the link below:

Replay: CLICK HERE