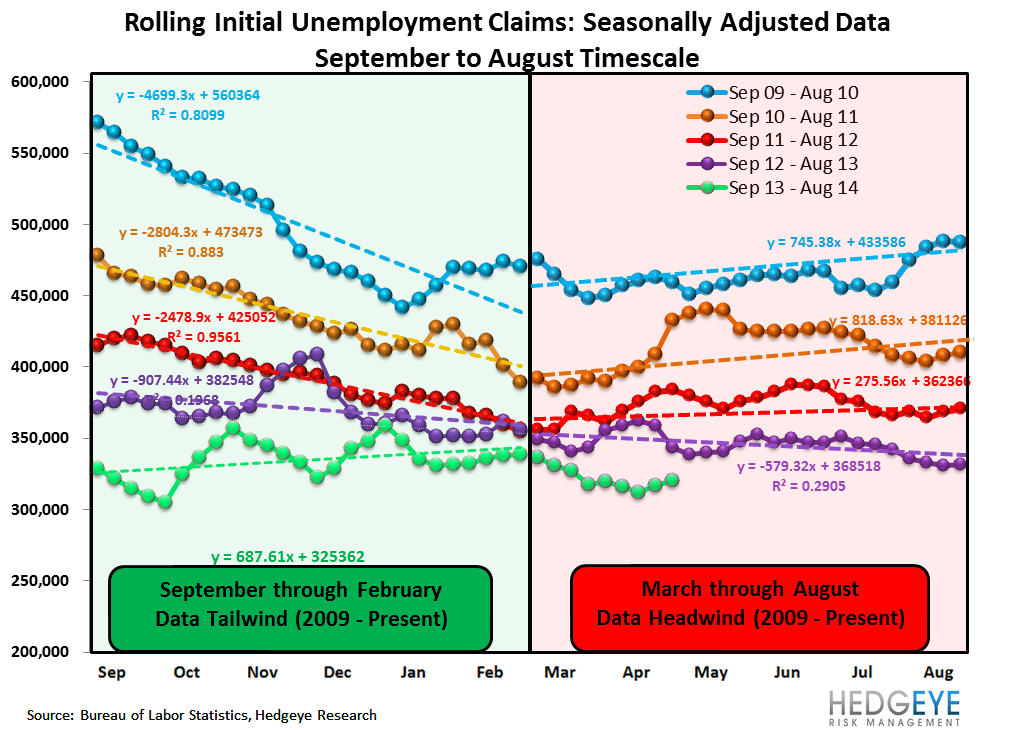

Labor Data Hits a Speed Bump

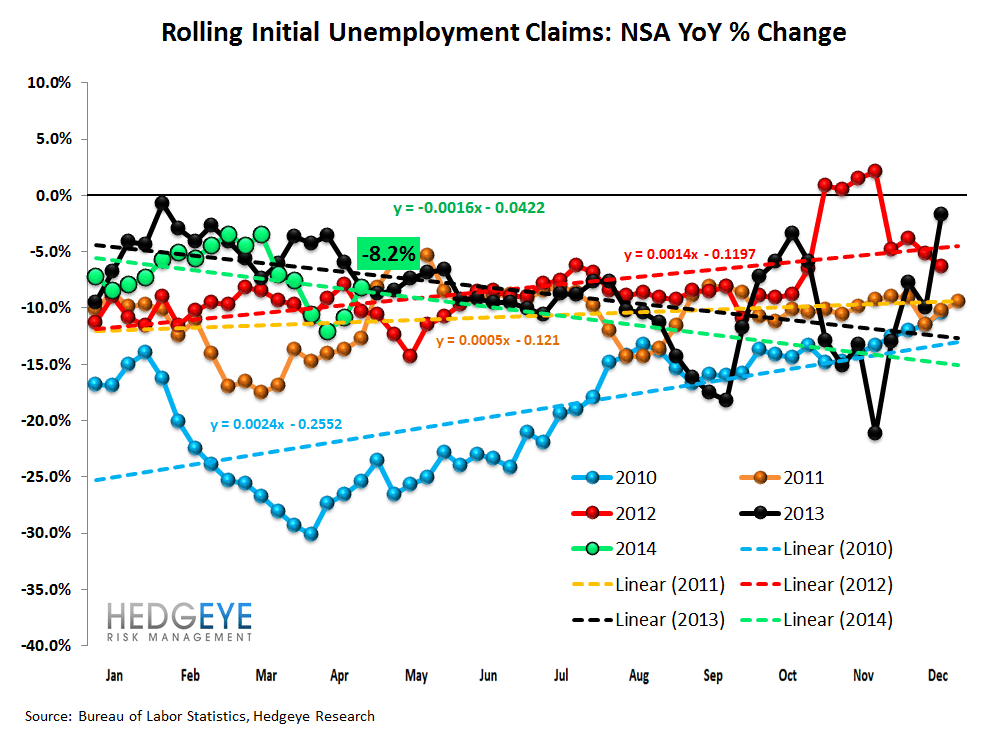

As we pointed out last week, Easter week is notoriously choppy from a data standpoint so investors should take the data with a grain of salt. Based on this distortion, we've seen significant volatility in the data in the last couple weeks. For instance, on a y/y NSA basis, this week claims were up 5.1% as compared with down 8.3% in the prior week. The 4-week rolling average, the better measure, showed a decelerating rate of improvement, moving to -8.2% from -10.9% on a y/y basis.

We're not overly concerned by the sudden deterioration in this week's print as the ADP number for April was reasonably strong and the Challenger report, while up slightly m/m, was in-line with recent trends. That said, should we see a continuation of this week's print in next week's data that would be more disconcerting.

For now, it appears the labor market recovery remains on track, albeit at a moderately decelerating rate of improvement.

The Data

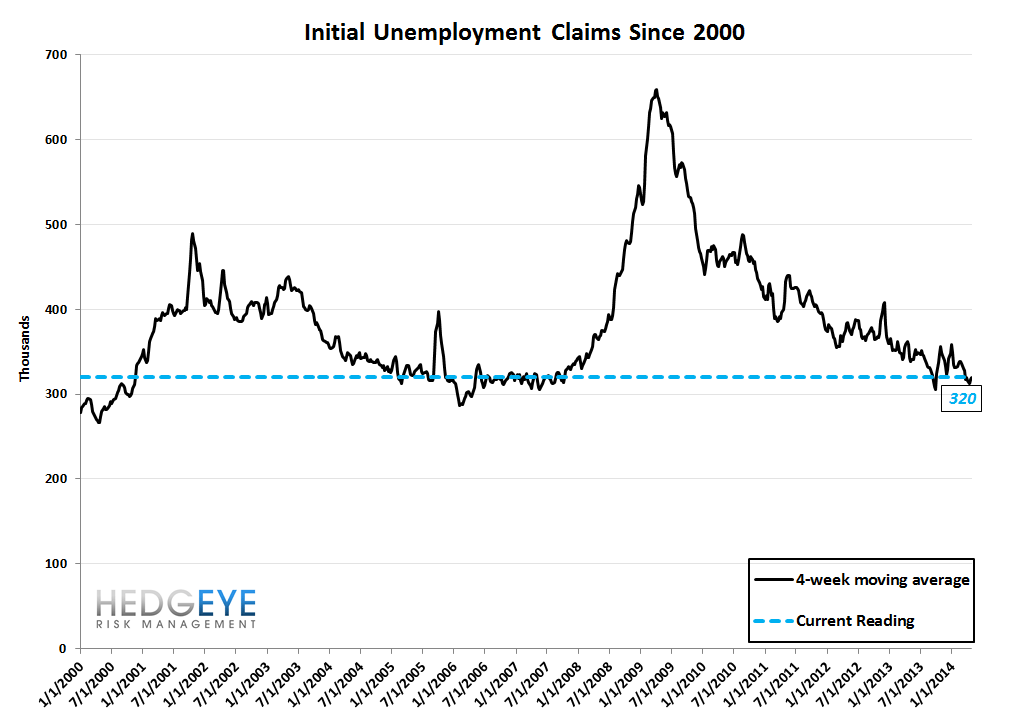

Prior to revision, initial jobless claims rose 15k to 344k from 329k WoW, as the prior week's number was revised up by 1k to 330k.

The headline (unrevised) number shows claims were higher by 14k WoW. Meanwhile, the 4-week rolling average of seasonally-adjusted claims rose 3k WoW to 320k.

The 4-week rolling average of NSA claims, which we consider a more accurate representation of the underlying labor market trend, was -8.2% lower YoY, which is a sequential deterioration versus the previous week's YoY change of -10.9%

Yield Spreads

The 2-10 spread fell -2 basis points WoW to 224 bps. 2Q14TD, the 2-10 spread is averaging 229 bps, which is lower by -10 bps relative to 1Q14.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT