TODAY’S S&P 500 SET-UP – April 25, 2014

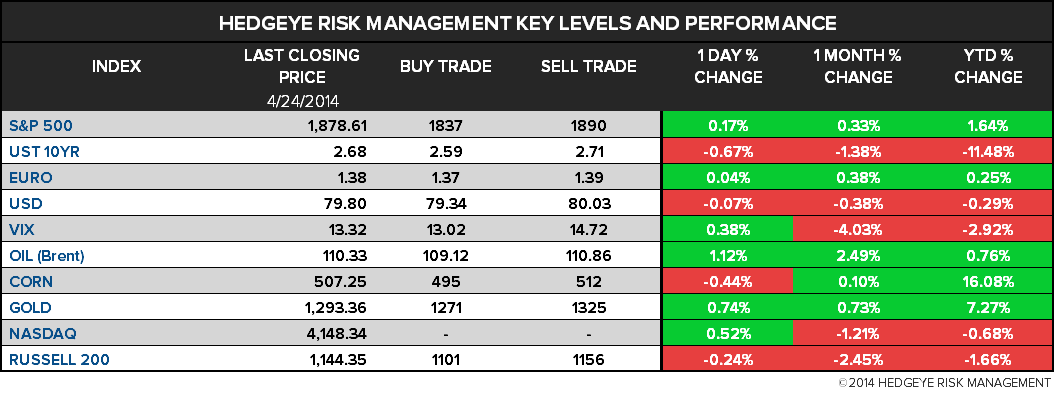

As we look at today's setup for the S&P 500, the range is 53 points or 2.21% downside to 1837 and 0.61% upside to 1890.

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.23 from 2.24

- VIX closed at 13.32 1 day percent change of 0.38%

MACRO DATA POINTS (Bloomberg Estimates):

- 9:45am: Markit US Composite PMI, April (prior 55.7)

- Markit US Services PMI, April, est. 55.5 (prior 55.3)

- 9:55am: UofMich Confidence, April final, est. 83 (prior 82.6)

- 1pm: Baker Hughes rig count

GOVERNMENT:

- House, Senate on recess

- 9am: Day 2 of Ex-Im Bank conf. in Washington speakers incl.:

- Tesla CEO Elon Musk

- Frmer Treasury Sec. Larry Summers

- Commerce Sec. Penny Pritzker

- Agriculture Sec. Tom Vilsack

- Energy Sec. Ernest Moniz,

- John Podesta, counselor to President Obama

- Ex-Im Chairman Fred Hochberg

- 11am BofAML’s Anne Finucane, global strategy and marketing officer, speaks at Brookings Institution

- WASHINGTON RECESS: Sec. Hagel, Forest Whitaker, New Coffee

- US ELECTION WRAP: Paul Beats Clinton in Poll; Democrats’ Funds

WHAT TO WATCH:

- Kerry warns Putin on Ukraine as Russia begins troop drills

- Russia debt rating cut to step above junk at S&P on Ukraine

- Gazprombank said to ready for U.S. sanctions on Ukraine

- Alstom board said to plan meeting today to discuss GE deal

- BofA said to face more than $13b demand in U.S. RMBS case

- Backbone of U.S. equities trading said to be closer to upgrade

- Relational Investors amasses 9.08% stake in Clean Harbors

- China tells Nike shoemaker to fix striker benefits by today

- Apple, Google, Intel, Adobe said to reach $324m accord

- Glaxo, Novartis may receive EMA decisions

- Navient, Under Armour to Replace SLM, Beam in S&P 500

- Obama visits South Korea as North shows nuclear test signs

- Cabinet members, Elon Musk speak at Ex-Im Bank conference

- Oregon may close $303m health site to join U.S. exchange

- U.K. retail sales unexpectedly rise; sign of growing momentum

- U.S. Jobs, Fed Meeting, BOJ, U.K. GDP: Wk Ahead April 26-May 3

EARNINGS:

- Aaron’s (AAN) 7:30am, $0.53

- AbbVie (ABBV) 7:47am, $0.68 - Preview

- Alaska Air Group (ALK) 6:01am, $1.24

- American Electric Power (AEP) 6:57am, $0.93

- Aon PLC (AON) 6:30am, $1.18

- Autoliv (ALV) 6am, $1.43

- Brookfield Office Properties (BPO CN) 7am, est. n/a

- Burger King Worldwide (BKW) 7am, $0.19

- Canadian Utilities (CU CN) 7:40am, C$0.75

- Colgate-Palmolive Co (CL) 7am, $0.68 - Preview

- Covidien (COV) 6am, $0.95 - Preview

- Dana Holding (DAN) 7am, $0.38

- DTE Energy Co (DTE) 7:15am, $1.47

- FLIR Systems (FLIR) 7:30am, $0.27

- Ford Motor Co (F) 7am, $0.31 - Preview

- IDEXX Laboratories (IDXX) 7am, $0.87

- ImmunoGen (IMGN) 6:30am, ($0.26)

- Laboratory of America (LH) 6:34am, $1.58

- Lear (LEA) 7am, $1.69

- LifePoint Hospitals (LPNT) 6:30am, $0.65

- Moody’s (MCO) 7am, $0.91

- State Street (STT) 7:30am, $1.00

- Tyco Int’l (TYC) 6am, $0.41

- Ventas (VTR) 7:10am, $1.07

- VF (VFC) 7am, $0.63 - Preview

- WABCO Holdings (WBC) 6:30am, $1.23

- Whirlpool (WHR) 6am, $2.31

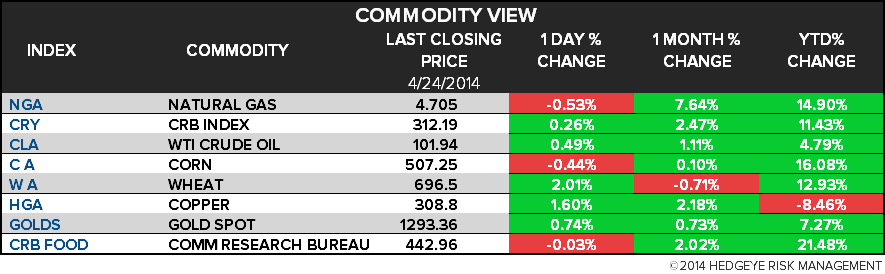

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Eating Less Beef Seen Way for Farming to Reduce Carbon Emissions

- WTI Set for Weekly Loss on Stockpiles, Widens Discount to Brent

- Sunken Gold Off U.S. Coast Lures Treasure Hunters: Commodities

- Copper Declines as Equities Slump Amid Tensions Over Ukraine

- Wheat Climbs Fourth Day as Ukraine Tension Raises Supply Concern

- Gold Rises a Third Day as Ukraine Keeps Traders Wary About Sales

- Rebar in Shanghai Pares Weekly Advance on China Output Gain

- Rubber in Tokyo Falls for Sixth Week on China Demand Concerns

- World Cup Power Cut Fears Spur Record Brazil LNG Buying: Energy

- China Shale Boom Seen by Honghua as Pollution Cuts Coal Use

- FCA Said to Observe London Gold Fixing as Scrutiny Increases

- Anglo Plans Move Away From Labor-Intensive Platinum Mining

- Gold Remains a Currency Central Bankers Don’t Control

- Palm Heads for Second Week of Advance as Demand Seen Rebounding

CURRENCIES

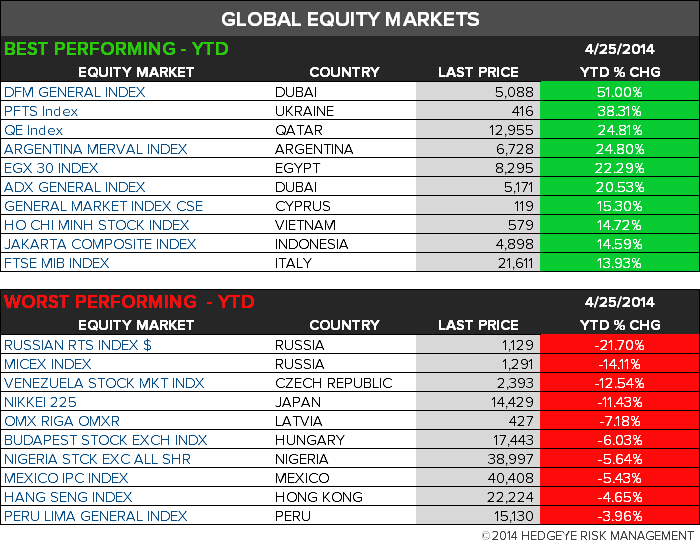

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

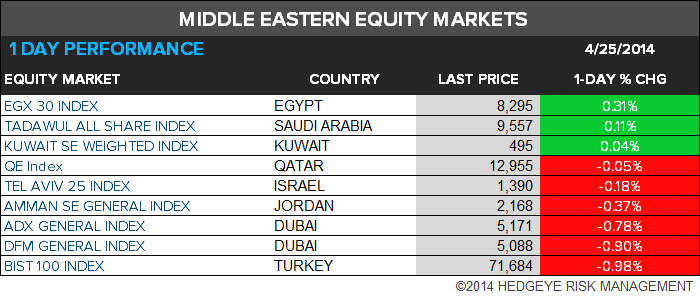

MIDDLE EAST

The Hedgeye Macro Team