Comps: CMG delivered +13.4% comp growth in the quarter, beating estimates of +8.8%. Management upped its FY14 comp guidance from low to mid-single digit growth up to high-single digit growth. Revenues of $904.163mm came in 3.5% higher than consensus estimates.

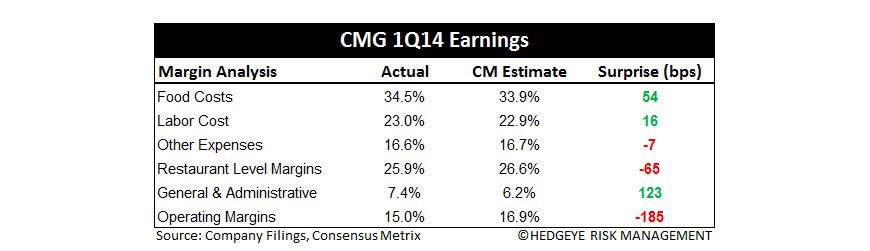

Margins: Despite accelerating top line trends, margin pressure continues to squeeze profits. Food costs accounted for 34.5% of revenue, up nearly 150 bps YoY, due to higher beef, steak, avocado and cheese prices. Restaurant level margins came in at 25.9%, down 40 bps YoY. G&A expenses accounted for 7.4% of revenue in the quarter, up 130 bps YoY due primarily to higher non-cash compensation exp. and litigation costs. Operating margins came in at 15%, down nearly 150 bps YoY.

Earnings: EPS of $2.64 came in light, missing consensus estimates by approximately 8% as the aforementioned margin pressure weighed on profits.

Analysis: While the majority of the restaurant industry continues to blame poor weather for disappointing comps, Chipotle delivered +13.4% comp growth primarily on the back of traffic gains. Chipotle continues to take market share in an increasingly competitive environment.

Declining margins are a concern, but are not insurmountable. Food inflation is weighing heavily on the cost of sales line, as beef, steak, avocado and cheese prices continue to surge. In order to combat this pressure, management announced they will take a mid-single digit price increase in 2H14. This should help mitigate food costs, which are expected to run above 36% of revenues (excl. any price increase) for the full-year. Management indicated they have ample pricing power and we tend to agree. In our view, Chipotle’s loyal and growing customer base will be willing to look past a $0.24-0.40 increase in the price of a burrito. People are willing to pay for a premium product.

Even with this margin pressure, Chipotle still operates a best in class business model and the demand for the product appears as strong as ever before. Faster throughput contributed meaningfully to the quarter, as restaurant saw an average increase of seven transactions at both peak hour lunch and peak hour dinner times. A unique and differentiated marketing/advertising approach helps keep CMG top of mind and continues to drive incremental traffic. Catering, though immaterial, continues to be a potential sales driver. We expect this to pick up steam in 2Q as graduation season commences.

CMG typically trades up on strong comps post-earnings, even when EPS misses, but an uncertain margin outlook has weighed down the stock. We believe same-store sales momentum and a price increase will effectively mitigate oncoming pressure, leading CMG to deliver +20% EPS growth over the next two years. Longer-term, international, ShopHouse and Pizzeria Locale continue to provide CMG with a strong growth runway.

Catalysts:

- CMG continues to poach market share from competitors as same-store sales and same-store traffic momentum persists.

- Marketing/advertising drives incremental traffic as the “Better Ingredients” campaign rolls out to 30 different markets in 2Q.

- Catering ramps up.

- Management accelerates its share buyback program.

Risks:

- Increasingly difficult comps for the remainder of the year.

- Food costs continue to surge.

- Consumers aren’t as receptive to a price increase as anticipated.

- Margin pressure erodes earnings.

Howard Penney

Managing Director

Fred Masotta

Analyst