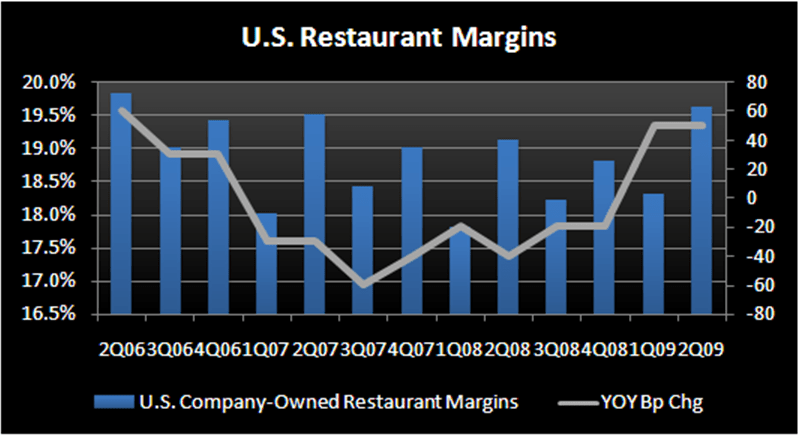

In Q209, MCD’s U.S. margins held up despite the sequential slowdown in comparable sales growth. Margins improved 50 bps during the quarter following 50 bps of expansion in Q1. These two quarters of growth show a marked improvement from the prior two years of decline. Moderating commodity costs helped to offset weaker sales as the company’s overall basket of commodities increased 4.4% in Q2 relative to the 6.7% increase in Q1. MCD expects this favorable cost environment to continue and even improve in the back half of the year with commodity costs forecast to grow only 1%. Management revised its U.S. commodity costs outlook for the full-year to up 3%-3.5% from its prior 5%-5.5% range.

MCD is going to need this increased cost favorability to offset continued softness in top-line numbers as July same-store sales are expected to be “similar or better” than June’s reported 1.8% increase. Management very clearly stated that Europe and APMEA July sales trends are running better than June, which leaves me to believe that the U.S. is the segment that is currently running similar to June.

Despite the sequentially slower sales in the U.S., MCD still grew market share on a year-to-date basis, gaining 50 bps of the formal eating out category, according to the company. For reference, the overall formal eating out category was negative in June.

MCD is experiencing some pressure on its average check. Specifically, management stated that average check accounted for about 65%-70% of sales in some quarters last year, but has come down to 50% and could move below that level as we move into 2010. Management attributed the increased pressure on average check to some trading down by consumers and the decreased level of promotion from the company around its higher priced products. Management expects operating margins to be stronger in the latter half of the year, but increased trading down could offset some of the company’s expected commodity benefit, particularly with the company saying it is less likely to take as much pricing as it has in prior years.

Regarding the recently launched Angus burger, the company has not yet launched a national advertising campaign around the product and admitted that the “timing’s not perfect on Angus.” I have communicated my concerns around the direction of MCD’s recent product launches, primarily the Angus burger and McCafe, which don’t focus on the company’s core consumers, so it was encouraging to hear that management recognizes as well that the timing is off for the Angus burger. Additionally, management said that due to lower media costs this year and a slight increase in the company’s level of investment in advertising, MCD has been able to advertise behind its core menu, largely the Big Mac, while also promoting the McCafe launch. This continued focus on the company’s core menu is necessary in this environment and alleviates some of my concerns about the Angus burger; though I do not think it will do much to benefit average check or margins in the near-term.

That being said, I am still not convinced that McCafe will provide the lift to sales that investors are expecting. Even with management saying that McCafe results are exceeding expectations and that the national advertising launch in May drove significant incremental unit movement, I am not yet a believer. June same-store sales numbers (and similar trends thus far in July) are not making me feel any better about McCafe. In response to a question, management said yes, it is on track to achieving $125K in incremental revenues per restaurant with its entire new beverage platform. This statement does not provide any real evidence of the success of McCafe, however, because the $125K goal includes fruit smoothies, crushed ice drinks and frappes, which have not even been launched yet. The fact that MCD is moving forward on reaching that $125K goal does not really quantify the current performance of McCafe. I know it is still early, but it’s important to remember that implementing McCafe into the entire MCD system required a high level of investment (about $100K per restaurant). I do not yet have the proof that McCafe is yielding the necessary returns.