Key Callouts:

What a difference a week makes. The ongoing collapse of high-flying social media tech names coupled with weaker-than-expected earnings from JPMorgan on Friday led to a 4.0% rout in the XLF last week. That makes Financials the second-worst performing sector YTD behind only consumer discretionary (down 2.65% through Friday's close). Utilities, for reference, are the best performing sector at +9.80% YTD.

Earnings thus far have been a mixed bag. Though we only have a handful of reports in hand at this point, three of the four "big uglies" have reported. Two of the three, Citi and Wells, have come in better than expected, while JPMorgan was a disappointment. We'll get results from the fourth horseman, BofA, on Wednesday morning.

As far as the risk monitor is concerned, we continue to see a fairly benign backdrop characterized by modest widening in sovereign and bank-specific swaps, but no real change in interbank systemic risk measures. Some of the main callouts are:

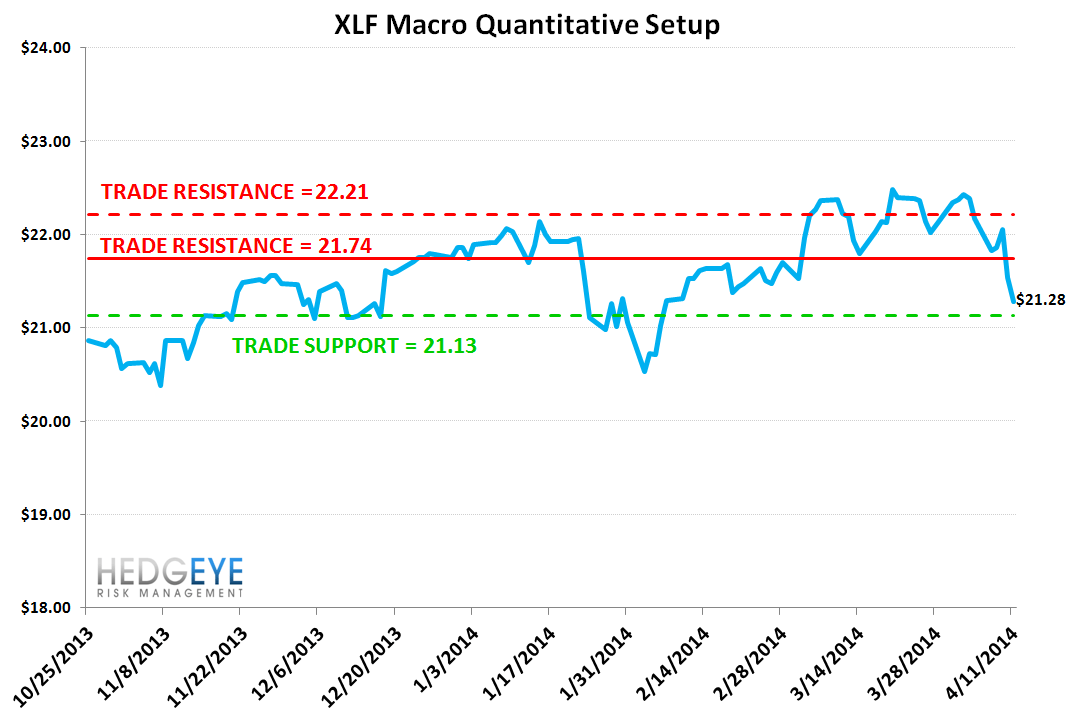

* XLF Macro Quantitative Setup – Our Macro team’s quantitative setup in the XLF shows 4.4% upside to TRADE resistance and 0.7% downside to TRADE support.

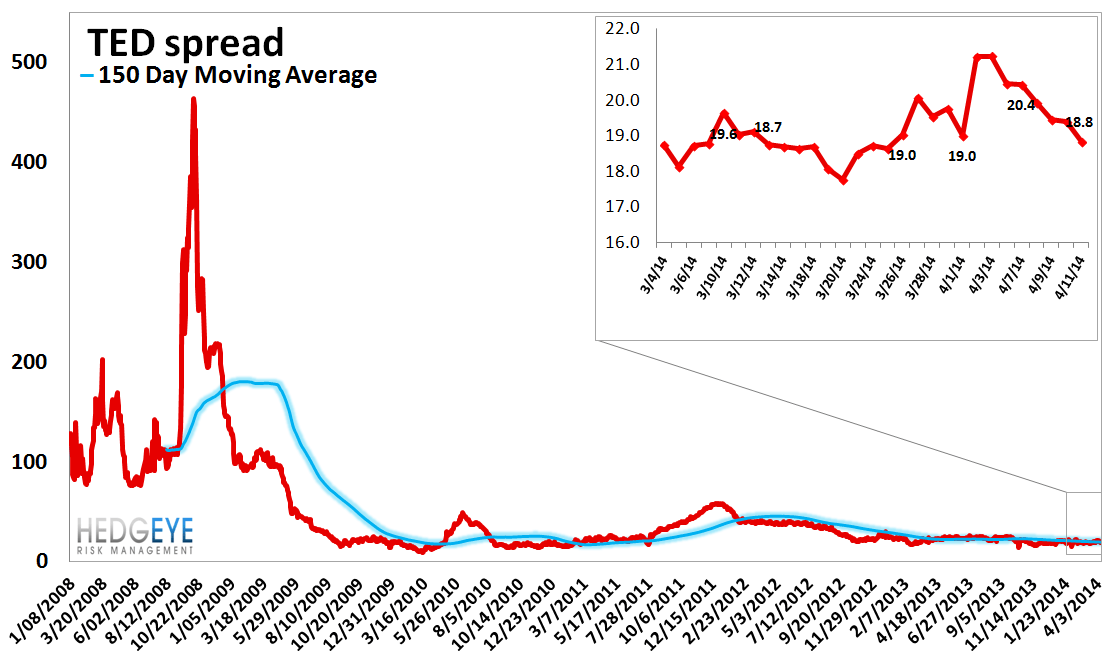

* TED Spread – The TED spread fell 1.7 basis points last week, ending the week at 18.8 bps this week versus last week’s print of 20.46 bps.

* U.S. Financial CDS - Swaps widened for 21 out of 27 domestic financial institutions. The Global US banks were all wider, by an average of 4 bps w/w, but remain tighter by 4 bps on a m/m basis. The specialty finance companies we track were wider on the week and on the month with the biggest moves coming from the mortgage insurers, MTG & RDN and Sallie Mae. The US insurers were little changed aside from the bond guarantors, MBIA and Assured Guaranty, where swaps widened out 60 and 32 bps, respectively w/w and are now wider by 106 and 62 bps m/m.

* European Financial CDS - Swaps across Europe's banking system were little changed (median change = 0 bps), but the Greek banks continue to tighten notably, dropping an average of 40 bps in the past week and 185 bps in the past month. This morning's news that GS & MS will be leading a secondary offering for National Bank of Greece doesn't hurt either.

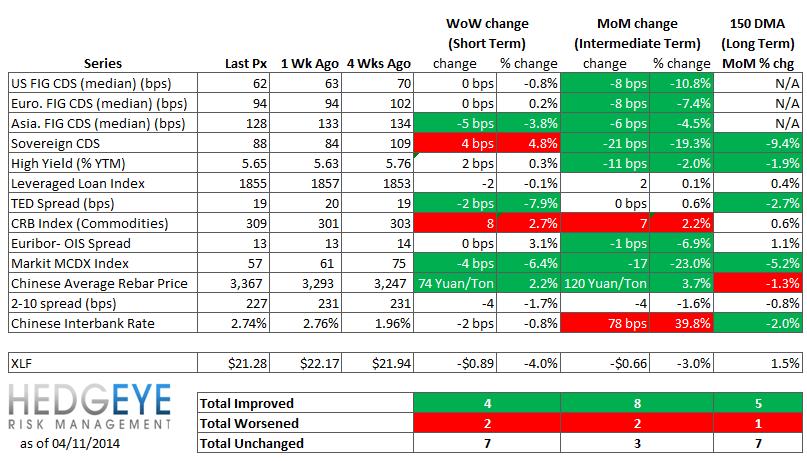

Financial Risk Monitor Summary

• Short-term(WoW): Positive / 4 of 13 improved / 2 out of 13 worsened / 7 of 13 unchanged

• Intermediate-term(WoW): Positive / 8 of 13 improved / 2 out of 13 worsened / 3 of 13 unchanged

• Long-term(WoW): Positive / 5 of 13 improved / 1 out of 13 worsened / 7 of 13 unchanged

1. U.S. Financial CDS - Swaps widened for 21 out of 27 domestic financial institutions. The Global US banks were all wider, by an average of 4 bps w/w, but remain tighter by 4 bps on a m/m basis. The specialty finance companies we track were wider on the week and on the month with the biggest moves coming from the mortgage insurers, MTG & RDN and Sallie Mae. The US insurers were little changed aside from the bond guarantors, MBIA and Assured Guaranty, where swaps widened out 60 and 32 bps, respectively w/w and are now wider by 106 and 62 bps m/m.

Tightened the most WoW: AON, CB, AIG

Widened the most WoW: MBI, WFC, AGO

Tightened the most WoW: MET, GNW, UNM

Widened the most MoM: MBI, AGO, TRV

2. European Financial CDS - Swaps across Europe's banking system were little changed (median change = 0 bps), but the Greek banks continue to tighten notably, dropping an average of 40 bps in the past week and 185 bps in the past month. This morning's news that GS & MS will be leading a secondary offering for National Bank of Greece doesn't hurt either.

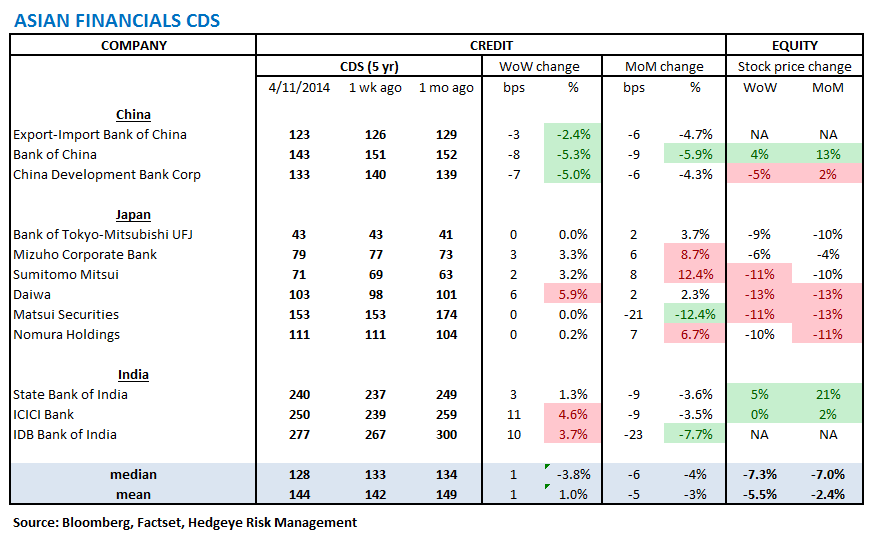

3. Asian Financial CDS - It was a mixed bag for Asian financials last week as Chinese banks tightened nominally while Japanese and Indian financials were generally wider.

4. Sovereign CDS – Sovereign swaps mostly widened over last week. Irish sovereign swaps tightened by -2.7% (-2 bps to 71 ) and Spanish sovereign swaps widened by 7.1% (6 bps to 93).

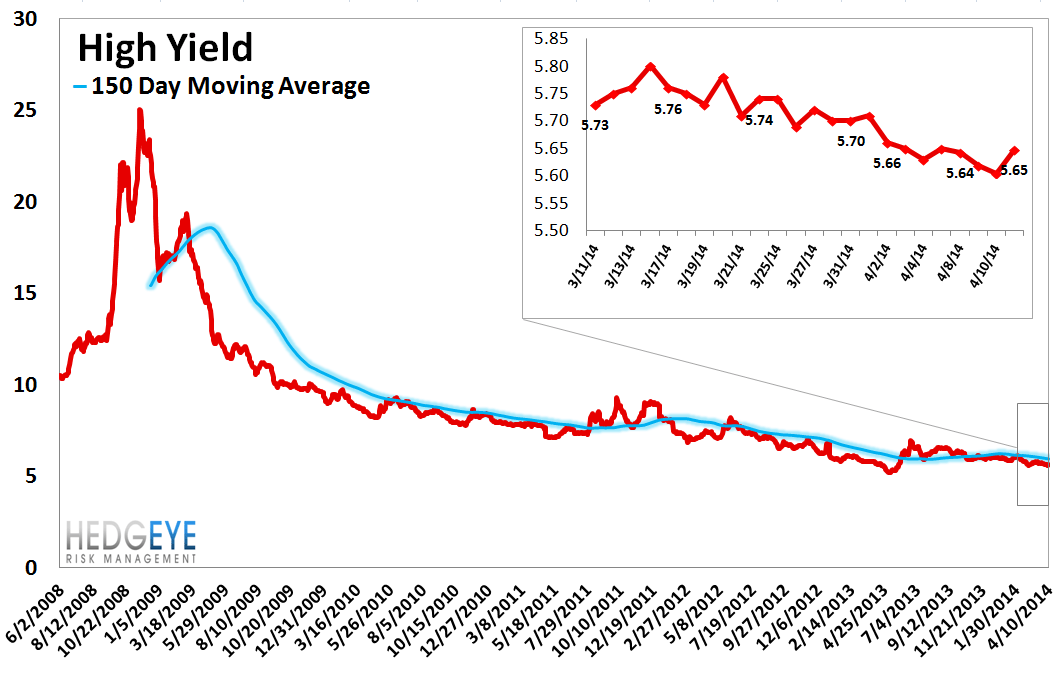

5. High Yield (YTM) Monitor – High Yield rates rose 1.7 bps last week, ending the week at 5.65% versus 5.63% the prior week.

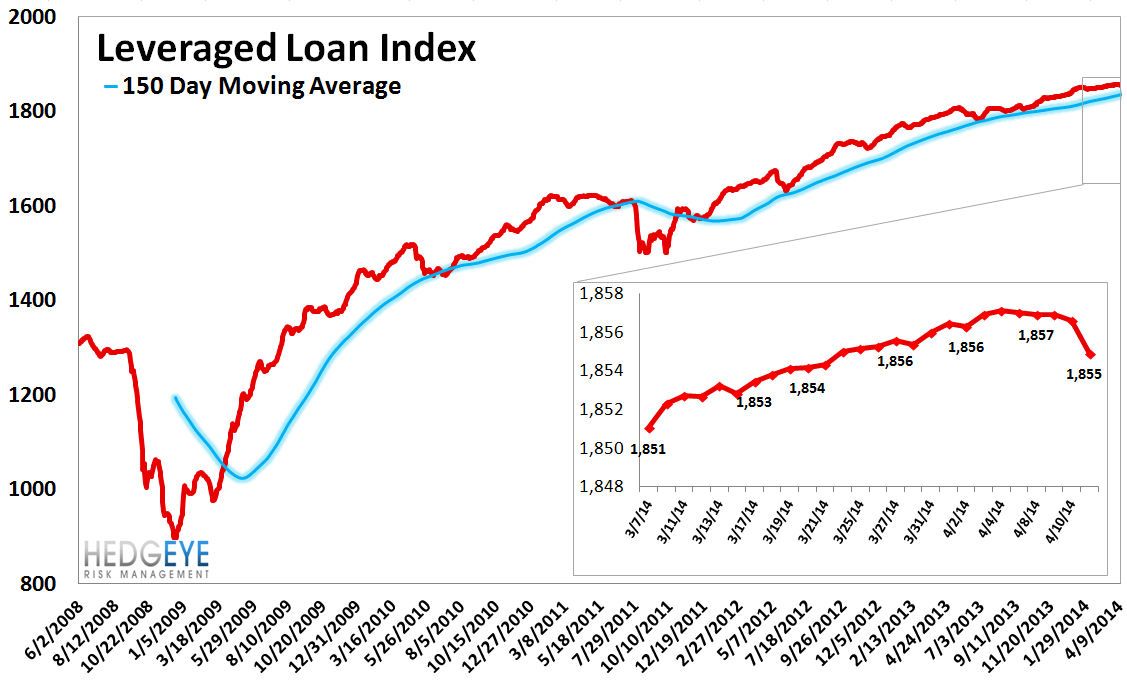

6. Leveraged Loan Index Monitor – The Leveraged Loan Index rose 2.0 points last week, ending at 1855.

7. TED Spread Monitor – The TED spread fell 1.7 basis points last week, ending the week at 18.8 bps this week versus last week’s print of 20.46 bps.

8. CRB Commodity Price Index – The CRB index rose 2.7%, ending the week at 309 versus 301 the prior week. As compared with the prior month, commodity prices have increased 2.2% We generally regard changes in commodity prices on the margin as having meaningful consumption implications.

9. Euribor-OIS Spread – The Euribor-OIS spread was unchanged week-over-week at 13 bps. The Euribor-OIS spread (the difference between the euro interbank lending rate and overnight indexed swaps) measures bank counterparty risk in the Eurozone. The OIS is analogous to the effective Fed Funds rate in the United States. Banks lending at the OIS do not swap principal, so counterparty risk in the OIS is minimal. By contrast, the Euribor rate is the rate offered for unsecured interbank lending. Thus, the spread between the two isolates counterparty risk.

10. Chinese Interbank Rate (Shifon Index) – The Shifon Index fell 2 basis points last week, ending the week at 2.74% versus last week’s print of 2.76%. The Shifon Index measures banks’ overnight lending rates to one another, a gauge of systemic stress in the Chinese banking system.

11. Markit MCDX Index Monitor – Last week spreads tightened -4 bps, ending the week at 57 bps versus 61 bps the prior week. The Markit MCDX is a measure of municipal credit default swaps. We believe this index is a useful indicator of pressure in state and local governments. Markit publishes index values daily on six 5-year tenor baskets including 50 reference entities each. Each basket includes a diversified pool of revenue and GO bonds from a broad array of states. We track the 16-V1.

12. Chinese Steel – Steel prices in China rose 2.2% last week, or 74 yuan/ton, to 3,367 yuan/ton. We use Chinese steel rebar prices to gauge Chinese construction activity, and, by extension, the health of the Chinese economy.

13. 2-10 Spread – Last week the 2-10 spread tightened to 227 bps, -4 bps tighter than a week ago. We track the 2-10 spread as an indicator of bank margin pressure.

14. XLF Macro Quantitative Setup – Our Macro team’s quantitative setup in the XLF shows 4.4% upside to TRADE resistance and 0.7% downside to TRADE support.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT