This note was originally published at 8am on March 31, 2014 for Hedgeye subscribers.

“People don’t just share information, they tell stories.”

-Jonah Berger

Per Jonah Berger in his new best selling #behavioral book, Contagious, that’s one of six principles that “cause things to be talked about, shared, and imitated” – storytelling. Some of the others you might want to consider are things like “social currency”, triggers, and emotion (page 23).

What makes research content #contagious? That will be topic #1 at our company meeting day @Hedgeye HQ tomorrow. All 52 of our employees will get a copy of the book and be asked to answer that question in 140 characters or less.

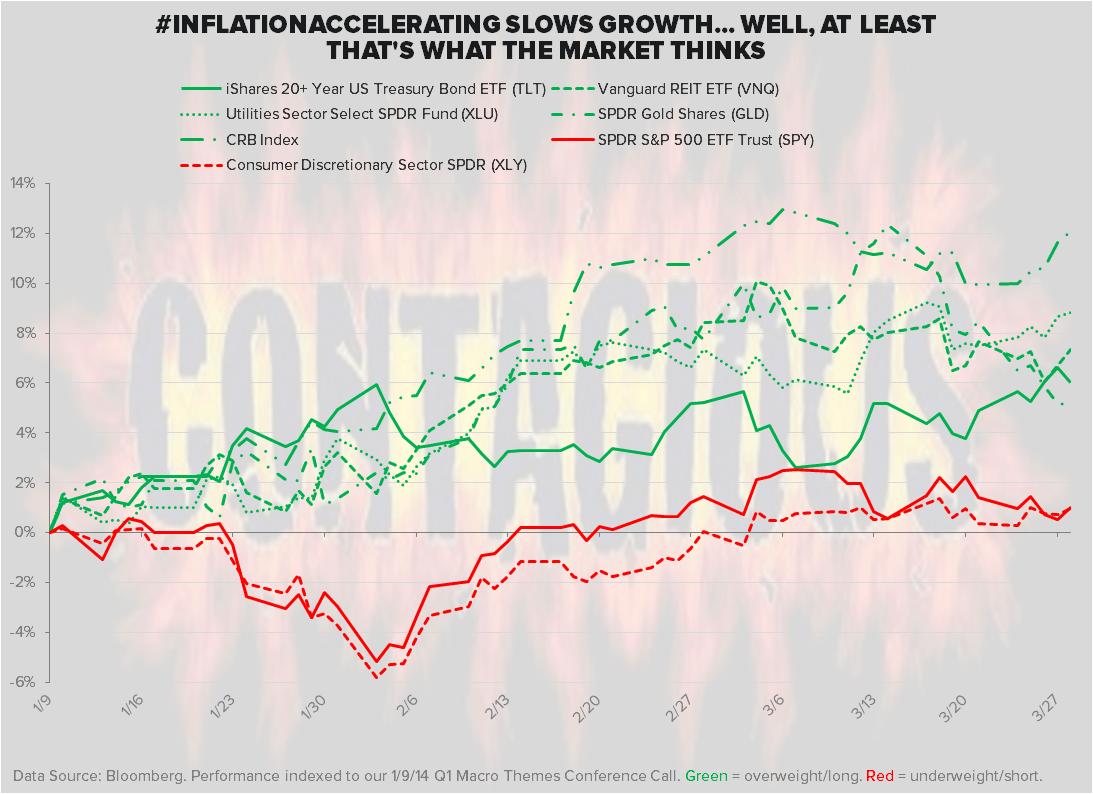

So tell me a story about what’s happening in markets for 2014 year-to-date. It’s the end of the 1st quarter, so don’t forget to augment your story with last price. After all, storytelling in our profession starts with a rear-view looking score.

Back to the Global Macro Grind …

“What broader narrative can we wrap our idea in?” –Berger (pg 24). Given the US economic data and how markets have scored it YTD, I think the answer to that is pretty straightforward: inflation slows growth.

That, of course, is the opposite of where consensus was when 2014 started. Virtually all of the #OldWall and Washington economists and strategists were taking up both their US GDP and SP500 forecasts. On inflation, the cover of the (Keynesian) Economist (NOV 2013) was titled “The Perils of Deflation.”

Instead, 3 months into the year:

- #InflationAccelerating = CRB Commodities and Food Indexes +8.9% and +19.3% YTD, respectively

- #GrowthSlowing = 10yr UST Bond Yield -31bps YTD to 2.72%

- YTD US Stocks = Dow Jones -1.5%, Russell2000 -1.0%, Nasdaq -0.5%, and SP500 +0.5%

Not to be confused with the Italian Stock Market (MIB Index), which has been the recipient of a #StrongCurrency Tax Cut (CPI in March fell to +0.4% y/y), and is up another +0.7% this morning to +14.2% YTD, the US consumer side of the US stock market has been flat out ugly.

Within the SP500’s roaring +0.5% YTD gain there’s a significant amount of #SectorVariance:

- US Consumer Discretionary (XLY) down another -2.1% last week to -3.8% YTD

- Whereas slow-growth #YieldChasing Utilities (XLU) were +1.2% in a down SPX tape last wk to +8.0% YTD

While we realize that both the (un-elected) Fed and the (elected) US Government say there is no impact on America when food inflation accelerates, we’ll still keep reality on your radar:

- Coffee prices were up +5.5% last week to +59.9% YTD

- Corn prices were up +2.7% last week to +14.4% YTD

- Soy prices were up +2.0% last week to +12.5% YTD

Oh, that would be in US Dollar terms.

Yes, dear linear-economists, I have a non-fiction story for you - inflation is priced locally (i.e. in local currency). So, if you get the rate of change (slope of the line) in a country’s currency right, you’ll get inflation right. If you get the slope of inflation right, you’ll get the rate of change in real growth right.

With the US Dollar Index still below our long-term TAIL risk line of $81.17, maybe that’s why we are starting to see a resurgence in the mother of all Burning Buck trades – Emerging Markets. Yep, as in the ones in Asia and Latin America that hit all-time highs when the US Dollar Index hit all-time lows (2011).

With Facebook (FB) face planting last week, look at what Emerging Markets did:

- MSCI Emerging Markets Index = +3.2% on the week to -2.7% YTD

- MSCI Latin America Index = +5.2% to -1.9% YTD

Yep, the squirrels in Brazilian Equities are running wild again as Latin America goes nuts for an alternative to being long a US social-media-bubble stock that lost 30-40% of its value in a month!

So would you rather be long socialism or social media? Tell me a story.

With a 3-5 year old story about “Flash Boys” (machines front-running monkeys) being popularized by Michael Lewis and 60 Minutes last night, I’m looking for something no one has borrowed from someone else. I’m looking for a broader narrative that can make us money by being early, instead of popular.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.64-2.81%

SPX 1846-1878

VIX 13.89-15.49

USD 79.55-80.41

EUR/USD 1.36-1.38

Gold 1278-1324

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer