TODAY’S S&P 500 SET-UP – April 14, 2014

As we look at today's setup for the S&P 500, the range is 46 points or 1.64% downside to 1786 and 0.90% upside to 1832.

SECTOR PERFORMANCE

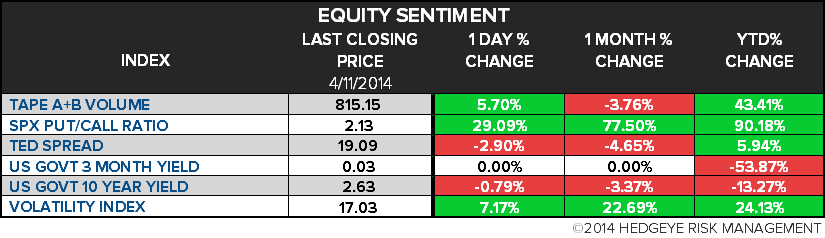

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.27 from 2.27

- VIX closed at 17.03 1 day percent change of 7.17%

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: Retail Sales m/m, March, est. 0.9% (prior 0.3%)

- 10am: Business Inventories, Feb., est. 0.5% (prior 0.4%)

- 11am: Fed to purchase $900m-$1.15b in 2036-2044 sector

- 11:30am: U.S. to sell $25b 3M, $23b 6M bills

- 12:45pm: Fed’s Tarullo, ECB’s Noyer speak in New York

GOVERNMENT:

- Treasury Sec. Jack Lew, Ukranian Finance Minister Oleksandr Shlapak discuss situation in Ukraine, U.S. pledge of support for $1b loan guarantee: 9:30am

- Congressional Budget Office plans to issue new baseline deficit projections: 11am

- President Obama attends Easter prayer breakfast

- House, Senate out of session on 2-wk recess

- U.S. Election Wrap: GOP Forms Joint Fund; Rep. Petri to Retire

WHAT TO WATCH:

- Citigroup earns: Higher fee income, elevated expenses seen

- Citigroup said to cut up to 300 jobs in global markets unit

- East Ukraine clashes turn deadly as Russia seeks UN meeting

- U.S. stocks seek to rebound after worst week since 2012

- CME gave high-frequency traders peek at market, suit claims

- High-frequency traders set for curbs in EU

- Minmetals Group to buy Glencore Peru mine for $5.85b

- Memos show regulators held back as evidence grew of GM defect

- Amazon.com to introduce smartphone in June: WSJ

- UBS Chair Weber sees lev.-ratio rules tightening globally

- KKR to sell Ipreo stake for $975m, FT reports

- Goldman Sachs countersues client over commodities stocks rout

- Apollo’s Momentive files for bankruptcy with exit financing

- China tightens oversight of trust as risk of defaults increases

- Brazil’s Mantega calls for alternatives to U.S. OK on IMF

- Renewables, nuclear should triple to save climate: UN panel

- Corn planting behind schedule for second straight yr

- ’Captain America’ tops ‘Rio 2’, leads N.A. cinemas a 2nd wk

EARNINGS:

- Bank of the Ozarks (OZRK) 6pm, $0.64

- Citigroup (C) 8am, $1.14 - Preview

- JB Hunt Transport (JBHT) 8:30am, $0.61

- M&T Bank (MTB) 8:01am, $1.61

- Pinnacle Financial (PNFP) 5:30pm, $0.46

- Sensient Technologies (SXT) 4:34pm, $0.66

- Sirius XM Canada (XSR CN) 4pm, C$0.05

- Triangle Petroleum (TPLM) 5:58pm, $0.13

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Goldman Predicts Commodity Declines Amid Rally in Bullion, Crops

- Brent, WTI Crudes Pares Gains as Libya Offsets Ukraine Tensions

- Gold Bears Bet Wrong Again as Fed Talk Favors Bulls: Commodities

- Nickel Rises to 14-Month High as Goldman Sachs See More Gains

- Palladium Climbs to Highest Since 2011 on Ukraine as Gold Rises

- Wheat Climbs as Ukraine Tensions Boost Supply Disruption Concern

- Commodities Rally to Highest in Six Weeks on Crisis in Ukraine

- Sugar Climbs as El Nino Seen Threat to Brazil Crops; Cocoa Slips

- Nickel May Rise to $20,000 If Indonesian Ban Stays, Goldman Says

- Hedge Funds Boosting Bullish Crude Wagers on Output Drop: Energy

- CME Gave High-Frequency Traders Peek at Market, Lawsuit Claims

- Rebar in Shanghai Unchanged as Spot Price Gains, Inventory Falls

- China Soybean Defaults Rattle Copper Traders, Markets: Bear Case

- Goldman Stands By $1,050 Gold Target on Outlook for Recovery

CURRENCIES

GLOBAL PERFORMANCE

EUROPEAN MARKETS

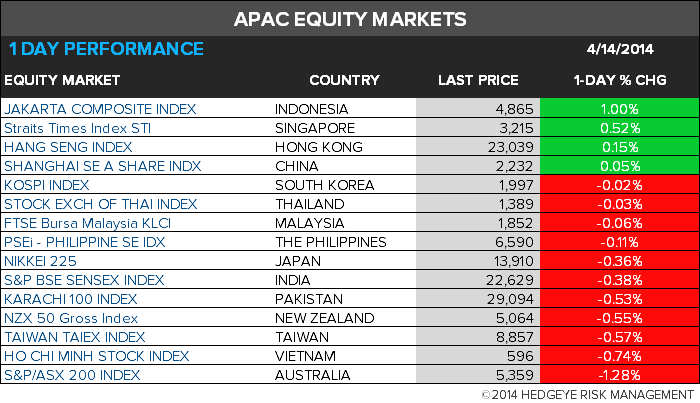

ASIAN MARKETS

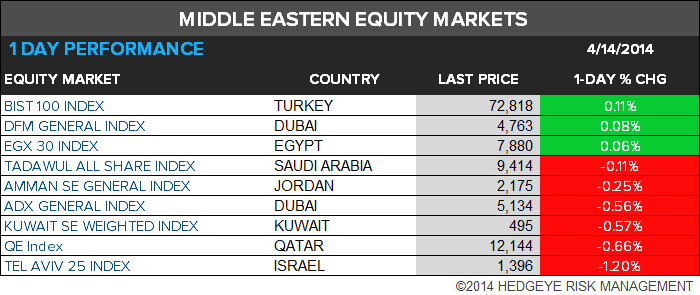

MIDDLE EAST

The Hedgeye Macro Team