“They complain that I’m robotic, abrupt, I’m not cheerful and smiley, and you know what? That’s not my problem,”

- Arthur Chu

On the back end of a 14-hour work day yesterday, after dinner time, bath time, story time, bed time and the host of other daily, toddler parenting “times,” I swilled back some late night espresso and fired up the DVR to watch something I’ve been itching to review for a while now - Jeopardy!.

Jeopardy is still on? The White House Petition to deport Justin Bieber only got 275K signatures? ….that fat guy is the kid from The Sixth Sense?

The story is a bit stale now, but if you didn’t follow its procession last month, controversial Jeopardy contestant, Arthur Chu, emerged out of the arithmetic ether like some sort of sagely, evil game-show probabilist savant.

Using math and a game theory based playing strategy, he managed an 11-game win streak and ultimate winnings of $298K – good for 3rd all-time (Wikipedia).

Alongside terseness and less than conventional congeniality, Chu’s most noteworthy exploit was his innovative use of the “Forrest Bounce” - whereby you jump quickly from category to category – across the bottom three rows of the board in an attempt to locate the “daily doubles”.

The daily double sits as the singularly largest source of uncertainty in the early rounds of the game. If that uncertainty can be systematically eliminated, the odds of winning increase provided one’s knowledge of the other trivia is marginally better than that of the other two contestants.

Here's the clip of Chu ferreting out a daily double, dismissively betting $5, answering “I dunno” after 1 second and summarily continuing on.

Chu’s challenge of conventional contestant etiquette inspired the ire of Jeopardy ‘purists’ nationally who took to social media en masse to voice their discontent and defend the game’s storied, 3-decade tradition from the emergent nihilist.

Applied mathematical innovation challenging preconceived wisdoms and conventional orthodoxy…..sound familiar?

Fortunately, in the end, #Evolution has a sneaking ability to overcome both antiquated conventionalism and institutional (ivory tower) obstructionism.

Back to the Global Macro Grind….

When hearing economists discuss markets in terms of rational agents, benevolent dictators, and other nonsensical simplifying assumptions, the economy becomes something largely abstract and intangible.

Certainly, the dynamic, complex system that is globally interconnected macro is difficult to comprehend (let alone forecast) in full, but a coherent understanding of the drivers of significant parts of the economy over defined periods isn’t inaccessible.

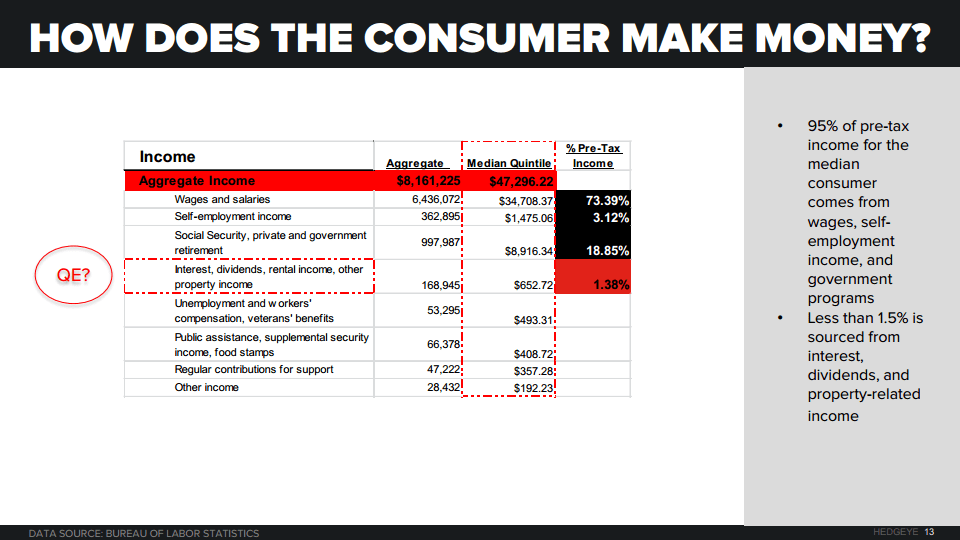

Consider the largest part of the domestic economy – consumption, in the short run.

Broadly speaking, the drivers of Consumption aren’t overly complicated. In short, consumer spending growth is a function of the growth in income, the marginal propensity to consume or save that income, and the net change in household credit.

Asset appreciation and credit growth matter, but they are somewhat indirect drivers. We discuss the wealth effect further below and leave the discussion and analysis of credit for another missive.

So, what do income and savings trends tell us about the slope of consumption growth?

Together, growth in disposable income and the change in the savings rate explain most of the change in nominal consumption (PCE) growth. Indeed, over the last 30 years, the multiple regression between PCE growth vs. nominal Disposable Income growth and the change in the Savings Rate produces an R-squared of 0.99. #tight

While that ultra-strong correlation doesn’t provide much insight into how to actually go about fostering significant, sustainable real income growth, it does provide a means of reasonably nowcasting the 68% of the economy that is consumption.

For instance, under a baseline assumption that the 3 primary input variables (Disposable Income growth, the Savings Rate and PCE inflation) come in at their respective QTD averages in March, the regression model suggests year-over-year real consumption growth of 2.2% in 1Q14 – down 10bps sequentially from 4Q13, but +20bps ahead of the TTM average

Nothing revolutionary or proprietary there - just the gravity of a few numbers to which consumption growth remains inextricably hostage.

What about the Wealth Effect?

The wealth effect ‘theory’ posits that when real wealth increases, consumer spending permanently increases by some fraction of that wealth increase in every subsequent year.

Consumers, on balance, don’t immediately convert 100% of a wealth increase into current consumption. Instead, in annuity like fashion, they tend to spread that ability for increased consumption out over their lifetime.

In general, studies examining the marginal propensity to consume show that consumer spending increases between 2 and 7 cents for each dollar of wealth increase.

It makes intuitive sense that an increase in real wealth, be it from housing or financial asset appreciation, lends itself to increased consumption.

Again, when hearing analysts and pundits discuss it in the media, one is left feeling that the wealth effect occurs via some mystical monetary transubstantiation whereby higher net wealth is somehow cleanly and instantaneously transformed into higher consumption.

In reality, a number of key, very mechanical conditions must be satisfied for increased housing/financial asset wealth to translate into higher consumer spending on non-housing related goods and services

Practically, increased real wealth needs to drive a behavior shift such that households decrease savings or other investments, increase home equity/other collateralized borrowing, or downsize to a cheaper residence (liquidity event freeing up cash for spending), for that wealth increase to be effective in driving higher consumption growth.

With the value of corporate equities and the aggregate housing stock up $3.52T and 2.0T, respectively, in 2013, the case for wealth effect spending has some residual legs. However, with equities down YTD and housing in the midst of a discrete deceleration, we expect wealth effect support to consumption to continue to ebb.

While consensus continues to make the pro-growth, pro-consumption call that should have been made last year, we think the consumer slows sequentially in 1H14. We layed out ‘the why’ in our 2Q Macro themes call on Tuesday. Ping if you’d like the replay/presentation.

Like Alex Trebek’s facial hair, the forward slope of consumption growth remains the subject of ongoing conjecture and speculation. Both continue to fascinate and confound consensus onlookers on a regular basis. Understanding both will remain central to generating global macro alpha in 2014.

Be the mustache, don’t be consensus…..or something like that.

Our immediate-term Global Macro Risk Ranges are now as follows:

VIX 14.72-16.67

Nasdaq 4007-4203

UST 10yr Yield 2.61-2.73%

SPX 1

Gold 1

Enjoy the weekend.

Christian B. Drake

Associate