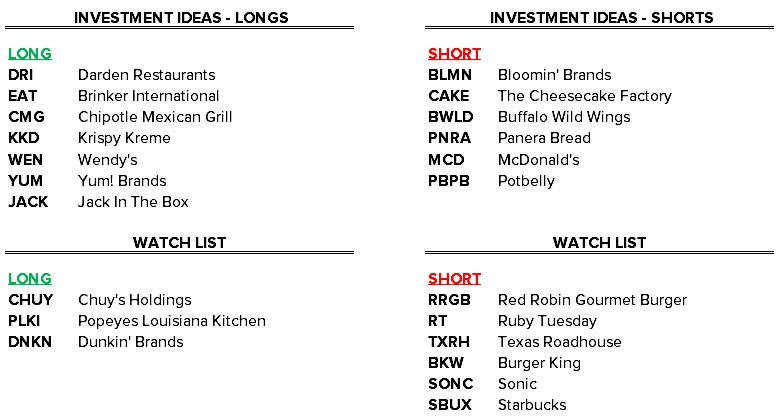

RECENT NOTES

03/31/14 Monday Mashup: PNRA, BLMN and More

04/01/14 DRI: Management Exposed

EVENTS THIS WEEK

Wednesday, April 9

- RT earnings call at 5:00pm

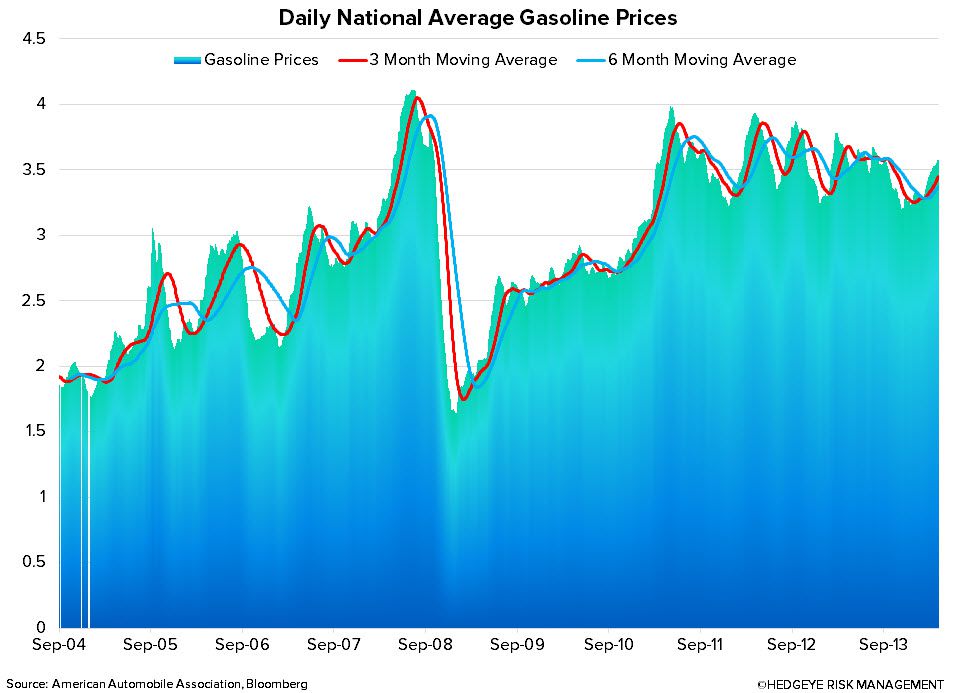

CHART OF THE DAY

Gasoline prices recently reached an eight-month high.

RECENT NEWS FLOW

Monday, March 31

- FRGI pushes its expansion west of the Mississippi, opening its first Texas location in the Dallas-area.

- PNRA upgraded to outperform at Wedbush Securities with a PT of $215

- CMG announced the lineup for its 2014 Cultivate Festival with events planned in San Francisco, CA, Minneapolis, MN and Dallas-Ft Worth, TX.

Tuesday, April 1

- DRI Starboard Value released an investor presentation, detailing its analysis of Darden management and the proposed Red Lobster spin-off. Starboard believes Darden’s real estate portfolio is worth approximately $4 billion and that separating Red Lobster and its real estate from Darden’s portfolio would destroy approximately $850 million in value. The presentation was deservedly critical of Darden’s current management team and is a must-read for interested parties. We highlighted what we believe are the key takeaways from the 100+ page deck in a note to subscribers and an exclusive HedgeyeTV video.

- DRI Darden responded to the public scrutiny by releasing a statement reiterating their confidence in the initiatives they have in place and once again urging shareholders to vote against a Special Meeting.

- SBUX announced it plans to bring back a number of its old breakfast favorites as La Boulange products have been generating some pushback from customers for their smaller portions.

Wednesday, April 2

- BWLD held its annual analyst day, reiterating FY14 guidance of 20% EPS growth and outlining its longer-term plans to sustain high earnings growth. The company continues to invest in smaller, emerging concepts with the hope that one or two will become a vehicle for significant future growth. BWLD’s goal is to be a growth enterprise, with more than 3,000 total restaurants.

Thursday, April 3

- No material news

Friday, April 4

- SONC cut to neutral at Buckingham

- DIN rated new neutral at Longbow

- BBRG Barron’s came out with a positive note on Bravo Brio Restaurant Group, citing an attractive valuation and an anticipated increase in same-store sales driven by better weather and menu-enhancing initiatives.

- DNKN Barron’s came out with a cautious note on Dunkin’ Brands, citing a hefty valuation and decelerating same-store sales trends.

U.S. MACRO CONSUMPTION

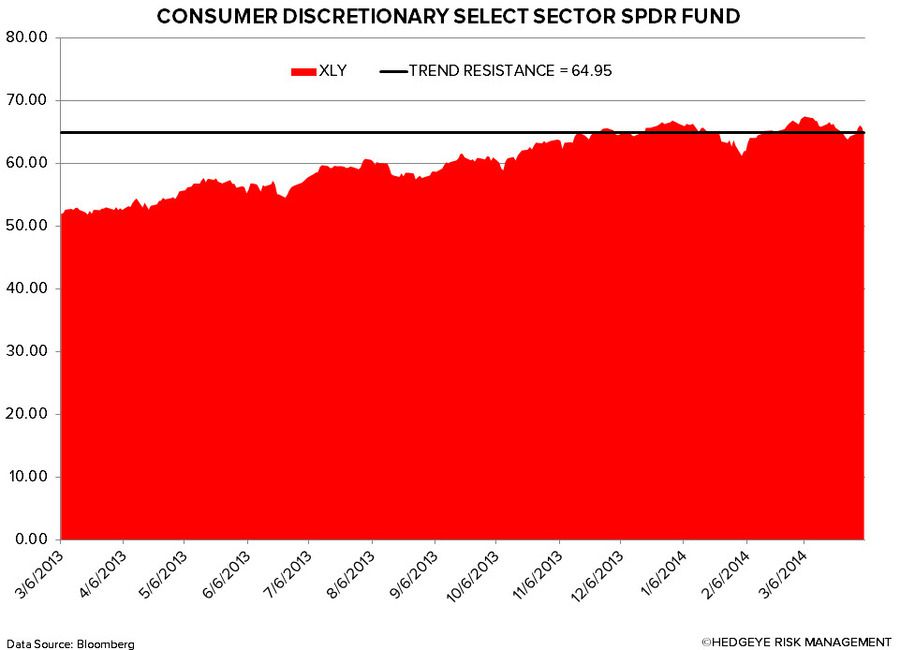

Last week was a bit of a bounce back one for consumer stocks, with the XLY +0.6% outpacing the SPX +0.4%. However, both casual dining and quick-service stocks, in aggregate, underperformed the broader XLY benchmark. The Hedgeye U.S. Consumption Model reverted back to bearish formation, from neutral, and is now flashing red on 7 out of 12 metrics. We continue to believe the current environment is more conducive to select fast casual and quick service restaurants than casual dining restaurants.

XLY QUANTITATIVE SETUP

From a quantitative setup, the sector remains bearish on an intermediate-term TREND duration.

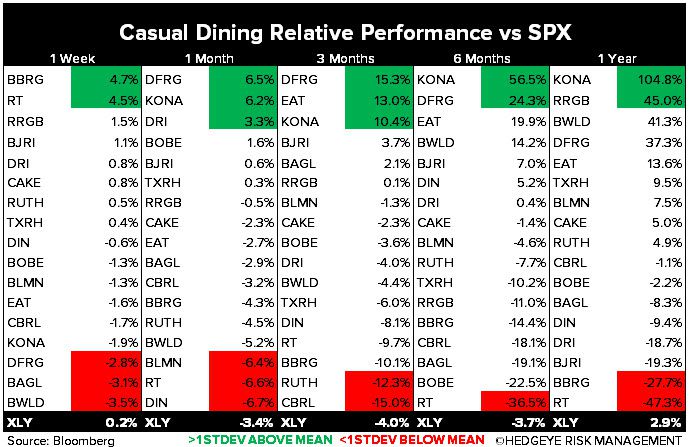

CASUAL DINING RESTAURANTS

Top 5 Week-Over-Week Divergent Performances

Positive Divergence: BBRG +4.7%, RT +4.5%, RRGB +1.5%, BJRI +1.1%, DRI +0.8%

Negative Divergence: BWLD -3.5%, BAGL -3.1%, DFRG -2.8%, KONA -1.9%, CBRL -1.7%

Positive Revision: RUTH +2.8%, DIN +0.2%

Negative Revision: DRI -1.3%, BLMN -0.9%, EAT -0.2%, CBRL -0.1%

QUICK SERVICE RESTAURANTS

Top 5 Week-Over-Week Divergent Performances

Positive Divergence: PLKI +4.9%, YUM +1.3%, THI +0.9%, MCD +0.2%

Negative Divergence: KKD -6.2%, GMCR -5.2%, PNRA -3.3%, SBUX -3.3%, PZZA -2.9%

Notable 1-Month Earnings Revisions

Positive Revision: SONC +0.9%, PZZA +0.8%, JACK +0.7%, GMCR +0.3%, CMG +0.1%

Negative Revision: KKD -3.3%, PNRA -0.4%, DPZ-0.2%, SBUX -0.2%, MCD -0.2%

Howard Penney

Managing Director

Fred Masotta

Analyst