We’re grinding on wrapping up our 2Q14 Macro themes presentation (call next Tuesday) so we’ll keep the March Employment review tight here. Some notable callouts along with a visual summary below:

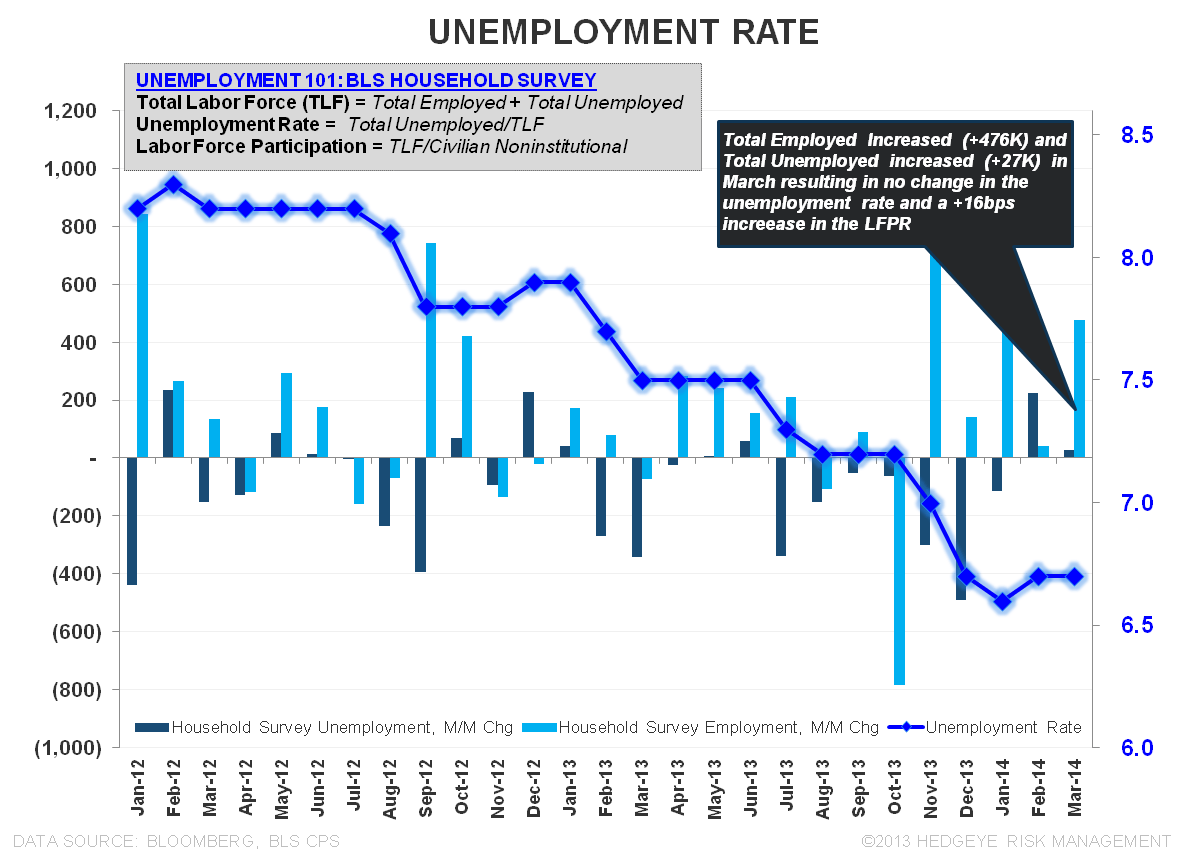

- Decent Absolute, Bad Growth: Both the NFP and Private payroll figures missed the round +200K estimate. While the absolute numbers (& the revisions) were decent, growth (2Y ave) in NFP and private payrolls posted their lowest rates since November 2012 and August 2011, respectively.

- No Policy Shift: Okay absolute + better sequentially = no change on the current policy path in the immediate term. Next FOMC meeting announcement is April 30th.

- Retracement: We have added exactly 8.9M private payrolls since the Feb 2010 trough in NFP employment. We officially eclipsed the prior Jan 2008 peak in total private employment for the first time this month

- Wage Growth Slowing: Ave hourly private sector earnings decelerated -10bps sequentially to +2.1% YoY. Similarly, hourly earnings growth for non-supervisory and production employees decelerated -20bps sequentially on both a 1Y and 2Y basis. A slowdown in wages does not augur strength for forward consumption growth (nominal PCE growth is running +3.0% as of Feb), particularly with savings rates near historic lows and wealth effect ebbing.

- Weather: BLS reported 148K out of work due to bad weather in March. This is up from the +117K reported in March of last year but exactly equal to the 10Y average of 148K. Weather distortion was real but its rearview.

- Seasonality: 1Q14 diverged negatively from the strong prior seasonal trends of the last 4 years. Seasonality will shift to a modest headwind from here.

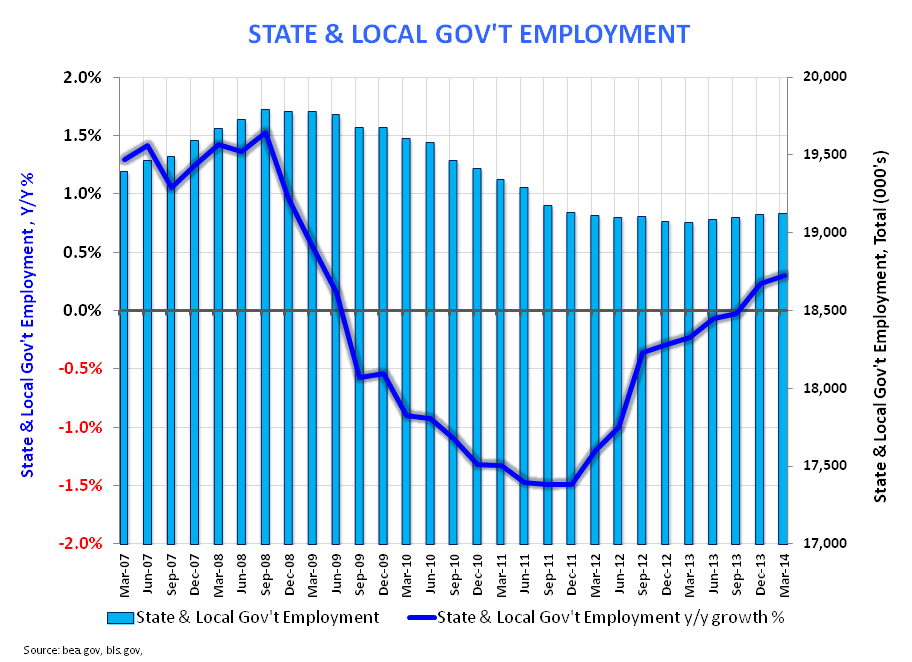

- State & Local Gov’t: A 7th consecutive month of positive growth for collective state/local government employment. Positive employment growth and higher spending at the federal level should continue to support aggregate gov’t sourced income growth in 2014 (~17% of total).

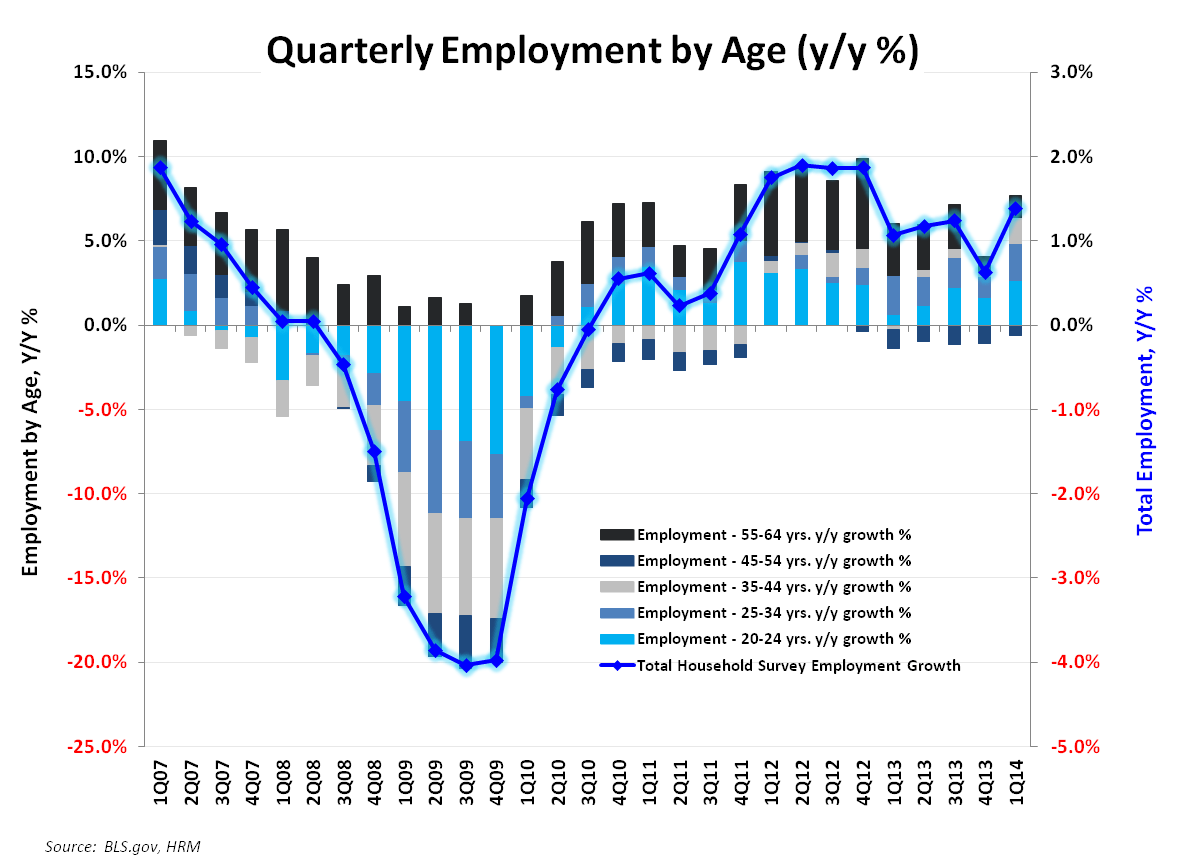

- Employment by Age: All age cohorts (20-64YOA) showed accelerating employment growth in March. For 1Q14, growth in total CPS employment is up 1.4% YoY – accelerating 80bps sequentially.

Christian B. Drake

@HedgeyeUSA