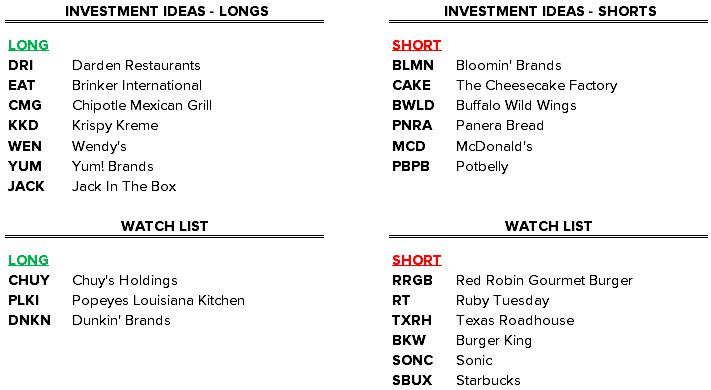

Recent Notes

03/24/14 Monday Mashup: DNKN, WEN and More

03/26/14 PNRA: Expect Some Near-Term Pain

Events This Week

Wednesday, April 2

- BWLD Analyst Day 10:30am EST

Chart Of The Day

The USDA reported last week the U.S. hog herd is at its lowest level in seven years, as cases of the fatal PEDv have tripled over the course of the last three months, killing nearly 8% of the herd. There is currently no cure for the virus, which has shown zero signs of slowing down. Prices of spare ribs and bacon are expected to continue surging in the coming months.

Recent News Flow

Monday, March 24

- SONC reported a strong 2QF14, delivering $0.07 adjusted EPS and beating bottom line estimates by approximately 18.5%. System-wide sales increased +1.4% as company drive-in margins improved 80 bps.

Tuesday, March 25

- RRGB acquired four Red Robin franchised restaurants from Swan Concepts Inc. The restaurants are primarily in the upstate New York area.

- WEN announced the completion of its system optimization initiative with the sale of 104 company owned restaurants in four primary markets. The initiative is expected to lead to higher operating margins, stronger free cash flow generation and higher quality of earnings.

- PNRA held its investor day and the results were generally disappointing. The company reiterated its 2014 guidance, but the initiatives in place (mainly the rollout of Panera 2.0) will take much longer to materialize than the street had anticipated. The company also declined to give 2015 guidance, due to a lack of visibility.

Wednesday, March 26

- DRI Activist Barington Capital officially called for a new CEO at Darden in a letter to the independent board of directors and urged the board to begin looking for Clarence Otis’ replacement.

- TXRH upgraded to buy at KeyBanc with a $30 PT.

Thursday, March 27

- YUM Taco Bell launched breakfast nationwide. The menu includes the Waffle Taco, A.M. Crunch Wrap, coffee and other products aimed at taking share from McDonald’s and other notable breakfast players.

- El Pollo Loco, a fast food chicken chain, is reportedly planning an IPO. The company operates 400 restaurants primarily in the West.

- IRG Chief Marketing Officer, Robin Ahearn, is stepping down to start her own marketing agency. Ignite will not replace the position and plans to work with Ahearn in her new role.

Friday, March 28

- MCD responded directly to Taco Bell’s breakfast rollout and controversial ad campaign by announcing a free two-week coffee promotion featuring its McCafe product line. The Breakfast War hath begun.

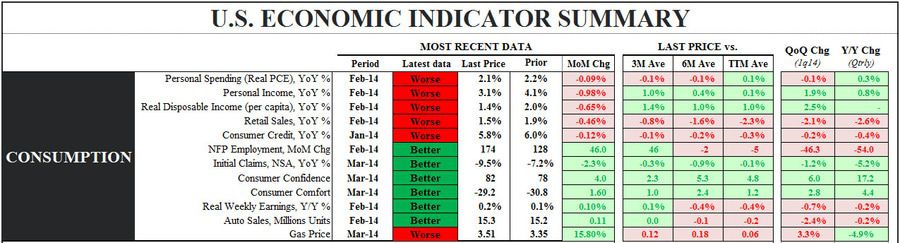

US Macro Consumption

Last week was a bloody one for consumer stocks, with the XLY -2.1% vs the SPX down -0.5%. Both casual dining and quick service stocks largely underperformed the XLY index for the second consecutive week. The Hedgeye U.S. consumption model reverted back to neutral, from bullish, and is now flashing green on 6 out of 12 metrics. We continue to believe the current environment is more conducive to select fast casual and quick service restaurants than casual dining restaurants.

XLY Quantitative Setup

From a quantitative setup, the sector turned bearish last week on an intermediate-term TREND duration.

Below we look at the performance of restaurant companies relative to the XLY and recent trends in earnings revisions estimates.

Casual Dining Restaurants

Top 5 Week-Over-Week Divergent Performances:

Positive Divergence: DRI +2.1%, EAT +1.9%, CBRL +1.3%, BAGL +1.3%, TXRH +0.6%

Negative Divergence: BBRG -5.1%, BWLD -3.5%, BJRI -3.4%, BLMN -3.4%, KONA -3.1%

Notable 1-Month Earnings Revisions

Positive Revision: RUTH +2.8%, BWLD +0.2%

Negative Revision: BOBE -25.4%, RT -1.1%, DRI -1.0%, BLMN -0.9%, BJRI -0.6%

Quick Service Restaurants

Top 5 Week-Over-Week Divergent Performances:

Positive Divergence: SONC +8.2%, MCD +4.0%, THI +2.1%, BKW +1.0%, YUM +0.7%

Negative Divergence: PNRA -5.8%, TAST -5.4%, CMG -5.1%, PLKI -3.7%, DNKN -3.3%

Notable 1-Month Earnings Revisions

Positive Revision: WEN +0.9%, PZZA +0.8%, GMCR +0.4%, SONC +0.4%, JACK +0.3%

Negative Revision: PNRA -0.4%, MCD -0.3%, SBUX -0.3%

Howard Penney

Managing Director

Fred Masotta

Analyst