The Big Picture

Food prices have surged in 2014, with the CRB Foodstuffs Index up +16.5% YTD and +4.8% YoY. While rapid advances in coffee, beef, cheese and milk have largely fueled the overall basket, all of the commodities we track are in the green YTD.

Commodity prices up YoY:

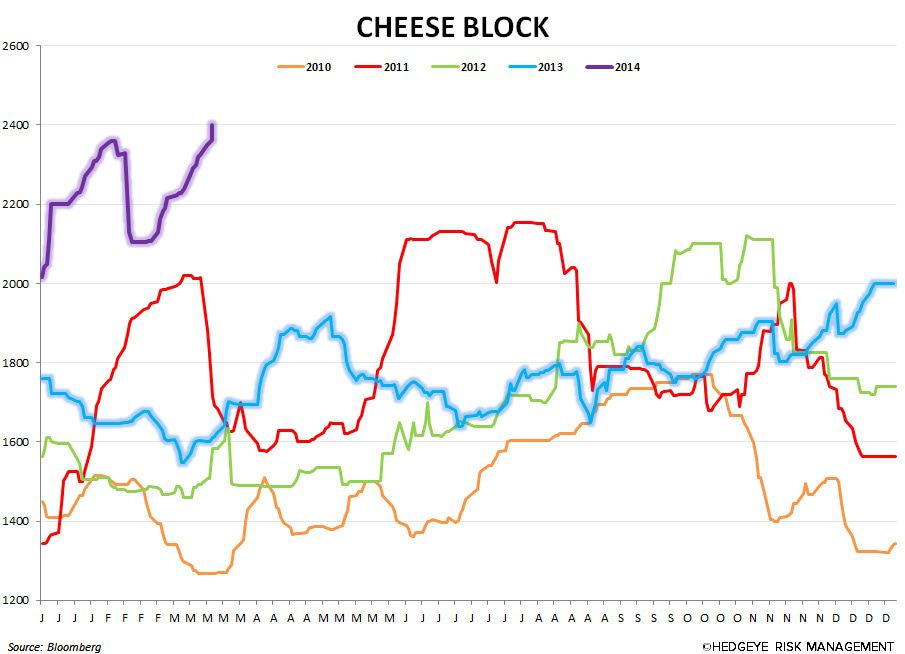

- Cheese Block

- Lean Hogs

- Rough Rice

- Soybean

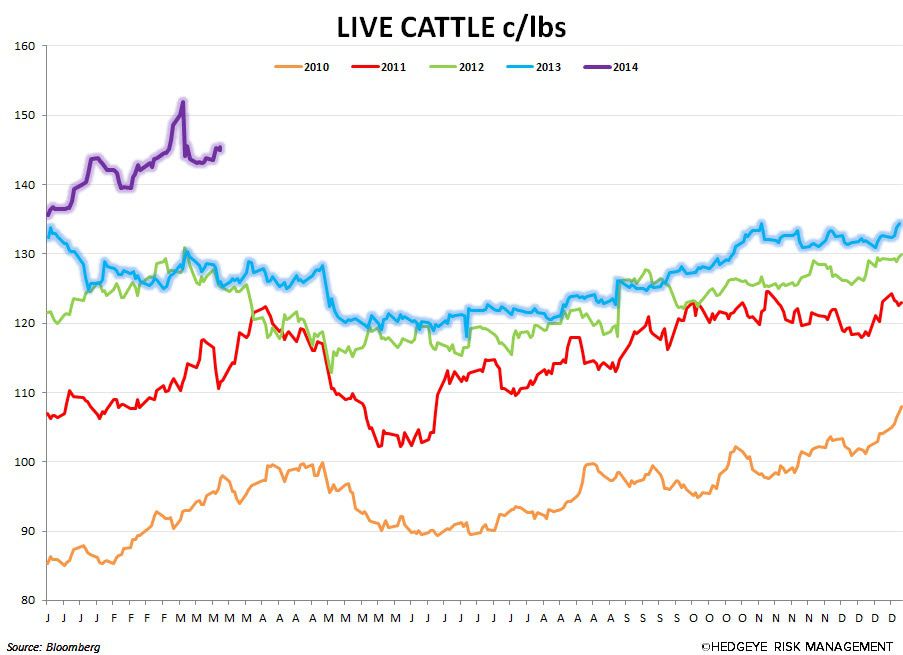

- Live Cattle

- Milk

- Natural Gas

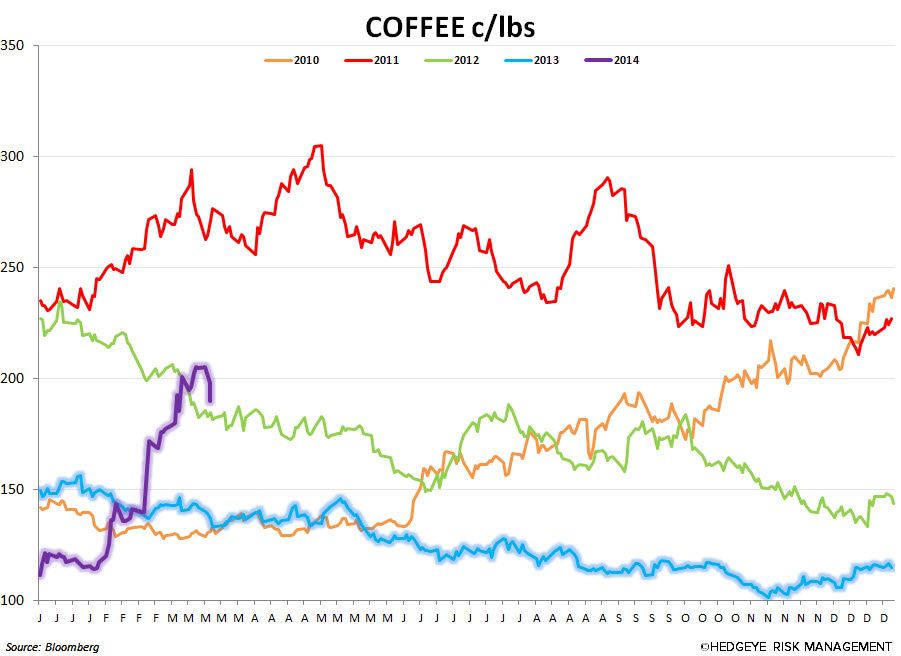

- Coffee

Commodity prices down YoY:

- Wheat

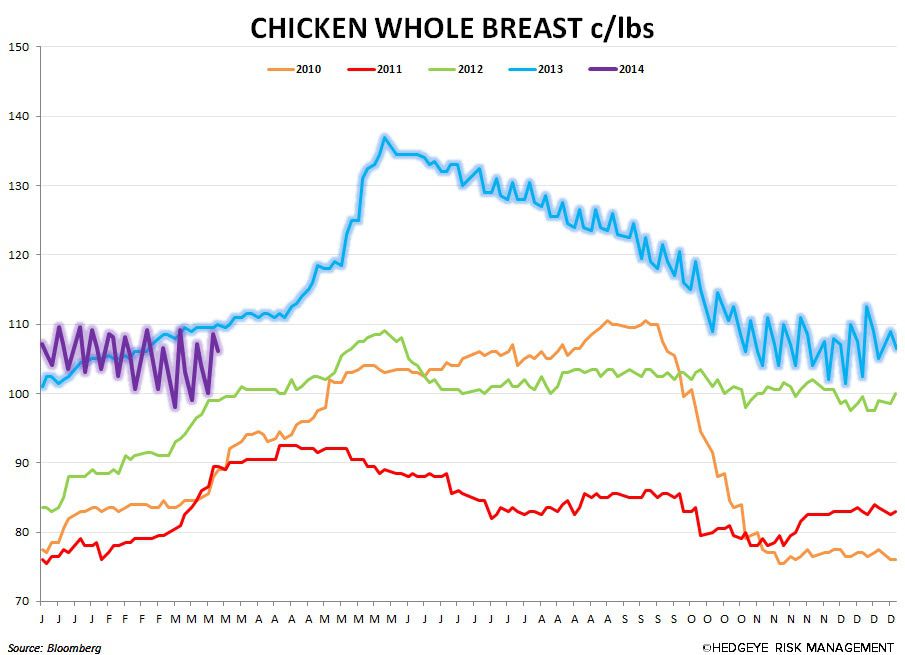

- Chicken Whole Breast

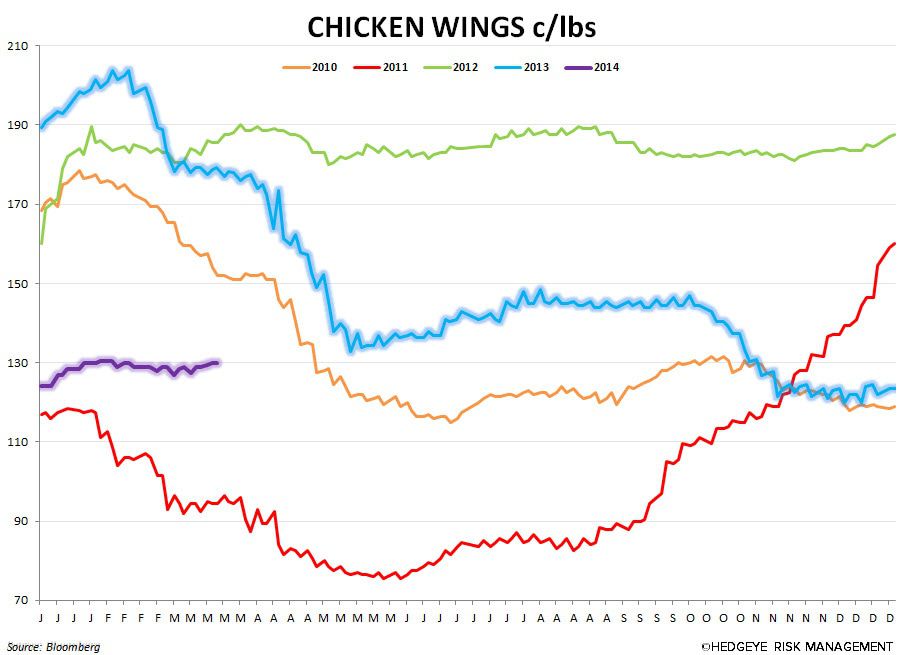

- Chicken Wings

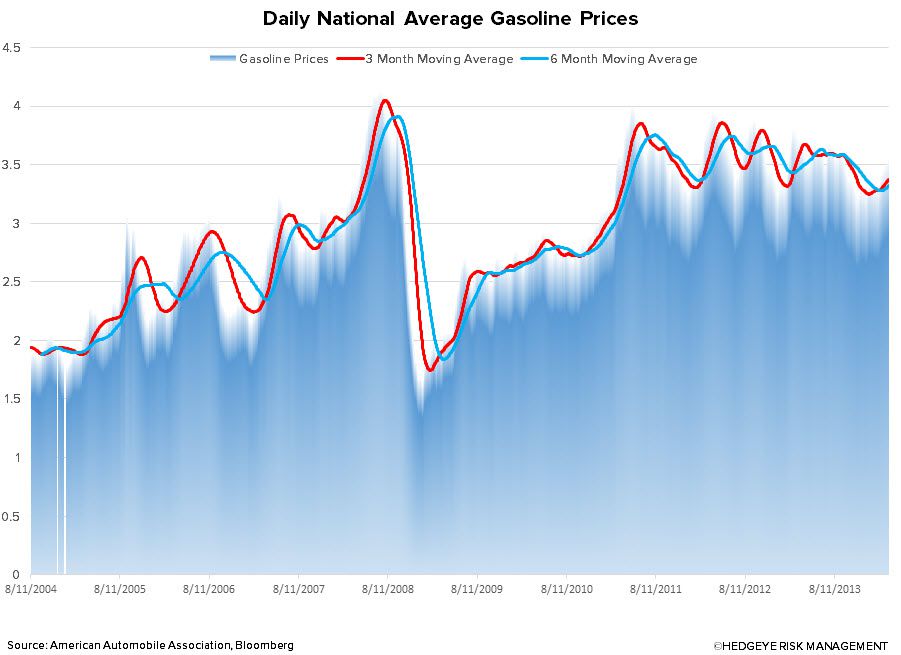

- Gasoline at the Pump

- Corn

- Sugar

Notable trends:

Coffee prices declined -12.1% over the past week. However, they have surged +60.2% YTD and remain up +21.5% YoY due to a prolonged drought in Brazil that has hampered national productivity levels. The two largest players in the coffee space, SBUX and DNKN, are essentially hedged for all of FY14, but we believe this increase has negatively affected sentiment within the space and could be a headwind in FY15. Takeaway – bearish for SBUX, DNKN, GMCR, KKD and THI.

Pork and Beef prices continue to tick higher, up +3.2% and +1.8%, respectively, over the past week. They are now up +50.1% and +16.0% YoY, respectively. Don’t expect much relief anytime soon – pork prices continue to be pressured by low slaughter rates and a tight supply, while the overall impact of PEDv remains unknown. Beef prices continue to rise amid a decline in cow herd sizes. Operators don’t expect much relief anytime soon as cattle herds take approximately two years to hit the market. Takeaway – bearish for TXRH, RRGB, BLMN, CMG, MCD, JACK, SONC, WEN and others with notable exposure.

Cheese Block and Milk prices are now up +49.4% and +37.6% YoY. Many operators expect, and have expected, these prices to moderate, but we have yet to see any signs of a slowdown. CME cheese block prices remain close to a decade high. We’ll continue to monitor these trends closely, as we have identified them as one of several critical factors in our short CAKE thesis. Takeaway – bearish for CAKE, DPZ, PZZA, TXRH, BLMN, SBUX, DNKN and others with notable exposure.

Wheat prices surged +5.6% over the past week, while Corn declined -0.1%. Both commodities are down -6.8% and -16.9% YoY and continue to provide some relief for operators. However, this benefit will continue to deteriorate if wheat stays on its current trajectory. Takeaway – has been bullish for everyone in Q1, but the trajectory has been decidedly bearish, on the margin, over the past month.

Chicken and Chicken Wing prices continue to provide relief to operators with notable exposure and menu flexibility. Both commodities are down -7.3% and -26.6% YoY, respectively. Takeaway – bullish for YUM, PLKI, BWLD and others with notable exposure.

Gasoline at the Pump is down -4.6% YoY, despite ticking up +0.3% over the past week. Takeaway – despite being down on a YoY basis, gasoline prices have been quietly ticking over the past month. Any sustained increase or decrease in gas prices could have a significant impact on the direction of discretionary spending and the consumer’s willingness to eat out. While current prices are a bullish data point for the industry, current trends suggest this may soon change.

Howard Penney

Managing Director

Fred Masotta

Analyst