Here's the second note in a series of five in advance of our LULU Consumer Survey results on Monday March 24th at 11am ET. When we polled consumers three months ago, we pulled away some clear insights. The concerns largely outweighed the strengths, which foreshadowed the company's results, and ultimately the stock price.

We're re-running our survey to gauge the incremental change over the past quarter, with the goal of seeing whether LULU is making progress (which could get us more constructive on the name) or not.

In preparation for 'Round 2' we want to offer up some of the notable takeaways from our last survey, as they'll be framing the discussion on Monday.

BUYING MORE/LESS

In this question, we asked consumers if they are buying more or less than a year ago. Now…we're the first to admit that we don't like this question very much. The reality is that the average consumer does not know how much she was buying a year ago. But, at least the question is consistent across brands, which is good enough for us. In our next survey, we'll see the rate of change by brand, which we think strengthens the question further.

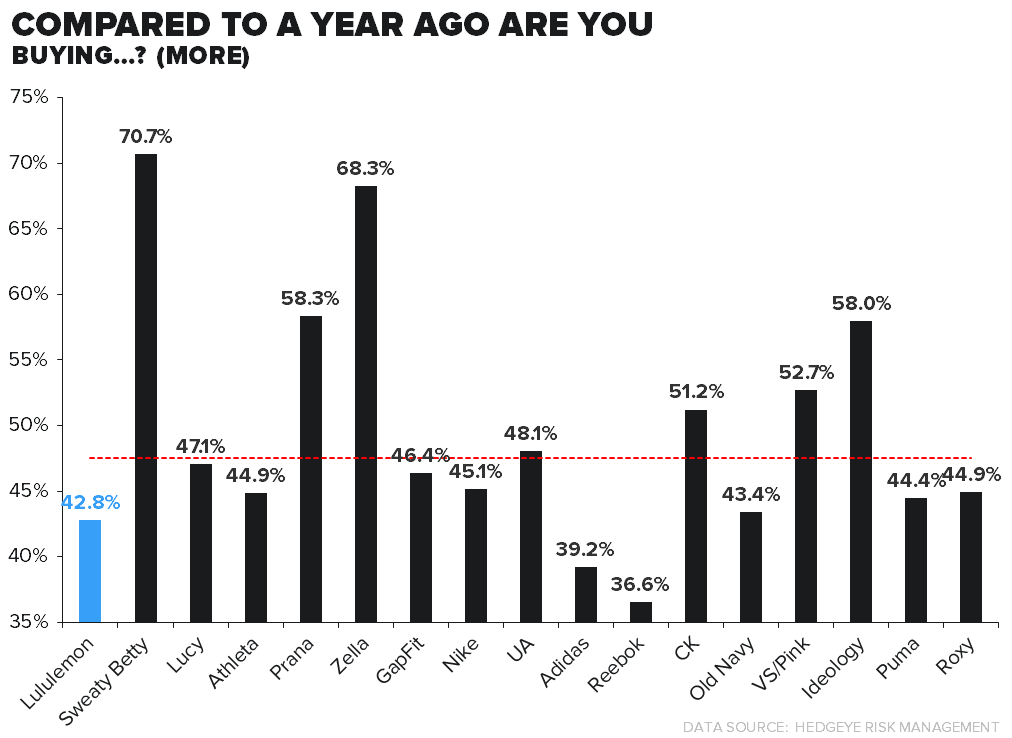

The first chart shows the percent of women who said that they are buying MORE product than they were a year ago. Winners are Sweaty Betty, Zella (Nordstrom), Ideology (Macy's) and Prana. Losers are Lululemon, Old Navy and AdiBok.

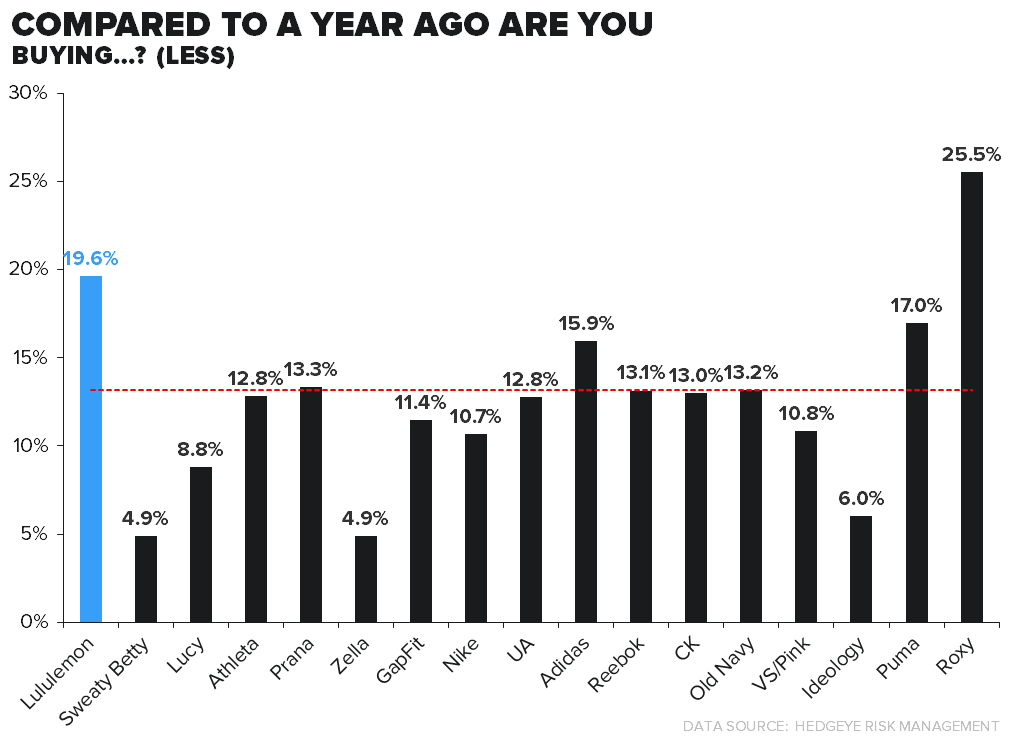

The second chart shows the percent of women who said that they are buying LESS of each brand versus a year ago. Roxy scored poorly, but the company is literally just starting its Yoga brand now (it is probably unfair to even have it on the list). Then comes LULU, Puma and Adidas. Most other brands scored respectably with 13% or less buying a smaller amount of the brand today versus a year ago. Check out Sweaty Betty and Zella (JWN) -- truly solid brand momentum.

Continuing with the 'buying more or less' theme, we thought it would be interesting to stack up our Yoga results vs what we learned when we did this for prior surveys in different categories. We're talking different consumer groups and different income levels in each survey. But the trends are noteworthy nonetheless. Department stores naturally trailed the pack with far more people 'buying less' than 'buying more'. Then comes Action Sports with a positive trend, followed by Yoga which puts the rest of the categories to shame. The results of this question won't make or break our thesis -- or decision to potentially change it. But it will give us an indication as to whether the category is getting even stronger or is easing on the margin.