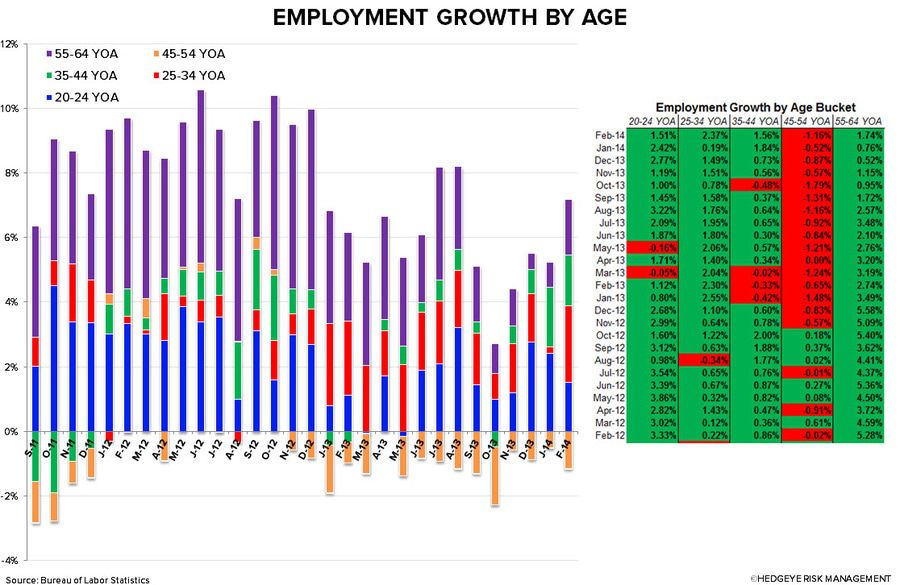

Employment growth by age trends have been fairly consistent over the past year. but we do have a couple of notable call-outs. The 25-34 YOA cohort had its best month of employment growth since January 2013, which should bode well for many quick-service and fast casual operators. On the other hand, the 45-54 YOA cohort continues to struggle, as February marked the 16th consecutive month of employment deterioration. This continues to be one of many headwinds facing the casual dining industry. February employment growth data below:

- 20-24 YOA: +1.51% YoY; -90.8 bps sequentially

- 25-34 YOA: +2.37% YoY; +217.7 bps sequentially

- 35-44 YOA: +1.56% YoY; -28 bps sequentially

- 45-54 YOA: -1.16% YoY; -64.2 bps sequentially

- 55-64 YOA: +1.74% YoY; +97.8 bps sequentially

Employment in the industry continues to grow at a healthy clip, but this growth has been decelerating across all three categories since mid-2013 which is, on the margin, negative for restaurants.

TTM Leisure & Hospitality growth has held up strong on a YoY basis, while TTM Knapp comps have declined steadily since the beginning of 2012. If anything, this supports our case that casual dining is currently facing a secular decline. In this type of environment, only the most nimble, innovative players will thrive.

Howard Penney

Managing Director

Fred Masotta

Analyst