TODAY’S S&P 500 SET-UP – March 11, 2014

As we look at today's setup for the S&P 500, the range is 27 points or 0.70% downside to 1864 and 0.74% upside to 1891.

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.41 from 2.41

- VIX closed at 14.2 1 day percent change of 0.64%

MACRO DATA POINTS (Bloomberg Estimates):

- 5:30am: Bank of England’s Carney, others speak in London

- 7:30am: NFIB Small Business Optim, Feb., est. 94 (pr 94.1)

- 7:45am: ICSC retail sales

- 8:55am: Redbook weekly sales

- 10am: JOLTs Job Openings, Jan. (prior 3.99m)

- 10am: Wholesale Inventories, Jan., est. 0.4% (prior 0.3%)

- 4:30pm: API weekly oil inventories

GOVERNMENT:

- President Obama to attend Democratic National Cmte, Democratic Senatorial Campaign Cmte events in New York

- Vice President Biden meets with Colombian President Juan Manuel Santos before attending inauguration of Chilean President Michelle Bachelet in Santiago

- 12:25pm: OMB Director Burwell speaks at Economic Club of Washington on Obama’s proposed FY15 budget

- 11am: John Brennan delivers remarks on 1st yr as CIA director

- 4pm: Sec. Jeh Johnson before House Homeland Security panel on agency’s 2015 budget proposal

- U.S. election wrap: Florida primary tomorrow

WHAT TO WATCH:

- Blackstone said to plan $5.5b Gates Global bid with TPG

- Lloyds trader said to tip off BP on $500m currency deal

- Ackman to show internal documents in Herbalife China webcast

- SoftBank’s Son vows "price war" if T-Mobile deal approved

- Russia holds firm on Crimea as Ukraine bolsters its defenses

- Malaysia widens search for missing jet to Malacca Strait

- Microsoft’s Titanfall game is being released

- Bank of Japan sticks to easing plan as sales-tax bump looms

- Sean Combs is said to bid $200m for MSG’s Fuse TV network

- Jimmy Iovine’s Beats Music is said to raise up to $100m

- House panel to probe GM recall of vehicles on ignition switches

- Repo fire-sale proposal said within reach

- Insurance cos. attempt to escape U.S. bank capital requirements

- Honda makes Acura stand-alone division to boost luxury lineup

- Energy Future said to hold last-minute talks to ease bankruptcy

- Blackstone buys majority stake in Accuvant for $150m: WSJ

- Wells Fargo reverses ban on staff making P2P loans, FT reports

- Apple said to seek exclusive iTunes releases: L.A. Times

AM EARNS:

- American Eagle Outfitters (AEO) 8am, $0.26 - Preview

- Arcos Dorados Holdings (ARCO) 8am, $0.16

- Dick’s Sporting Goods (DKS) 7:30am, $1.11 - Preview

- John Wiley & Sons (JW/A) 8am, $0.85

- Springleaf Holdings (LEAF) 7:30am, $0.45

- Synta Pharmaceuticals (SNTA) 6:45am, ($0.30)

- Transcontinental (TCL/A CN) 10:30am, $0.34

PM EARNS:

- Caesars Entertainment (CZR) 4pm, ($1.52)

- Diamond Foods (DMND) 4:01pm, $0.08

- Furiex Pharmaceuticals (FURX) 4:05pm, ($1.06)

- Inter Parfums (IPAR) 4:05pm, ($0.17)

- NCI Building Systems (NCS) 4:01pm, ($0.01)

- VeriFone Systems (PAY) 4:01pm, $0.27

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Iron Ore Bear Market Deepens Amid China Credit, Surplus Concerns

- WTI Trades Near 3-Week Low as Supplies Seen Rising; Brent Stable

- Nickel Pioneer Shut Out as China Cuts Smokestacks: Commodities

- Copper Rebounds as Barclays Says Worst Selling May Have Passed

- Corn Extends Slump to One-Week Low as USDA Signals Ample Supply

- Gold Climbs Toward Four-Month High as Ukraine Spurs Haven Demand

- Indonesian Exchange Sets Daily Suggested Opening Bid for Tin

- Corn Extending Rally With Wheat for CBH on Ukraine Supply Risk

- Rebar Rises After Biggest Three-Day Decline Since October 2011

- Japan’s Giant Tsunami Wall Fails to Stop Atomic Power Fears

- Palm Oil Drops as Prices at 18-Month High Seen Cutting Demand

- Ukraine Crisis Endangers Exxon’s Black Sea Gas Drilling: Energy

- Record Bullish Oil Bets May Deepen Any Slump: Chart of the Day

- Tin Shipment Seized by Indonesian Navy En Route to Singapore

CURRENCIES

GLOBAL PERFORMANCE

EUROPEAN MARKETS

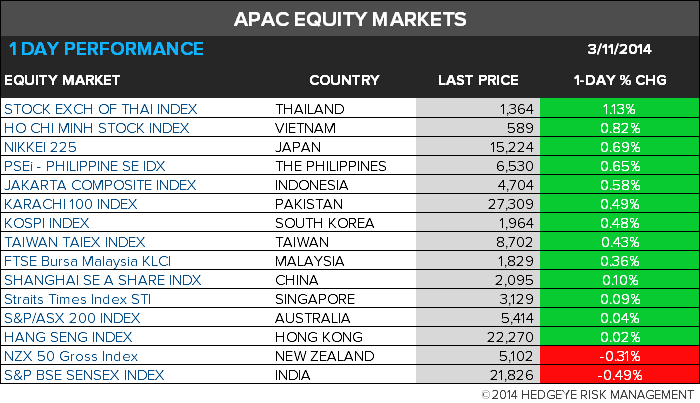

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team