“The punishment process is as important as the reward system.”

-John Allison

As I quote one of my favorite post-2008-crash books, The Financial Crisis and The Free Market Cure (pg 177), I’m thinking more about the full body ache I have from our old-man hockey semi-final yesterday than what’s going on in the market. That’s not good.

Neither was the US stock market’s reaction to Friday’s US jobs report that “beat” expectations (must have been the weather). Stocks raged to all-time highs on the open, then got pancaked by midday. Newsflash: the monthly jobs report is a lagging indicator.

I didn’t have a good week, but it could have been worse. With the CRB Commodities Index +9.6% YTD (vs. the Dow -0.7%), this year’s Burning Buck rally in some asset prices has a lot more to do with #InflationAccelerating than anything else.

Back to the Global Macro Grind…

While I am certain that if they had @CNBC Kiev, Ukraine would look just fine (Ukrainian currency crash has its stock market +29.8% YTD in Burning Currency terms); it’s not. Especially when a country’s currency is in free fall, her stock market is not the economy.

In Russian terms, Putin’s Ruble is crashing (-10% YTD) and so is his stock market (-24% since OCT and -19.7% YTD). Meanwhile the Chinese just printed a -18.1% year-over-year export disaster for FEB. The Shanghai Composite dropped -2.9% on that to -5.5% YTD.

Argentina’s Burning Currency is -17.1% YTD, but there’s probably nothing to worry about there either. Unless you are an Argentine, that is… Oh, and after trying the whole debt-levered-currency-devaluation thing, Venezuela is about to default on its debt.

In other news last week…

- US Dollar Index remained on its YTD lows (below @Hedgeye TAIL risk line of $81.14)

- US 10yr Yield popped +14bps to 2.80%, but failed to overcome @Hedgeye TREND resistance of 2.81%

- Coffee Prices ripped another +9.2% on the week to +74.3% YTD

No that’s not a typo – up +74.3% is the number, so whatever you do – don’t call that #InflationAccelerating.

With the CRB Foodstuffs Index +14.9% YTD, it’s not just coffee prices that are inflating:

- Corn was up another +5.5% last week to +13.7% YTD

- Soy was up another +3.1% last week to +14.2% YTD

- Lean Hogs were up another +5.8% last week to +24.6% YTD

Yes, basically you’re going to have to back everything out of your breakfast and call eating anything with pig in it “non-core” as the Fed tells you to consume a gluten-free Whatsapp for a buck a day instead.

Have you ever asked yourself why neither the Fed nor Bush/Obama ever talk about America’s currency?

As John Allison points out plainly on page 187 of the aforementioned book, “The fundamental issue underlying the boom-and-bust cycle in the financial industry is the lack of sound money. Unfortunately, the Fed is constantly manipulating the value of the dollar.”

And our profession gets that – or at least the machines do. It’s called Correlation Risk – and this is how it works:

- Down Dollar starts to trend as the Fed abandons anything that remotely resembles a two-way policy

- “Bad” economic news becomes good for asset price inflation, as the market front-runs the Fed easing

- Correlation Risk (asset price inflation trading inversely with US Dollars) starts to dominate

On that last point, here are the 30-day inverse correlations between US Dollar and the big stuff:

- Gold -0.88

- SPX -0.87

- CRB Index -0.75

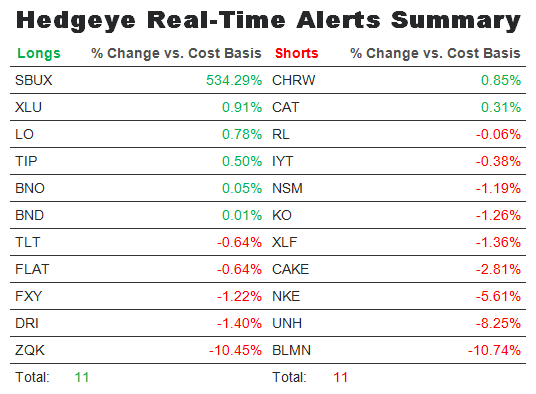

In other words, the market calls what the Fed is signaling a Policy To Inflate (humans call it a tax). And yes, #InflationAccelerating will slow growth. That’s why you saw me buy bonds on Friday (and anything that looked like a bond, including Utilities, XLU).

Punishing The People with food, energy, rent, etc. inflation can only last for so long. Unless you think America has it in her to become Argentina, she has a tendency to rise up against these types of un-constitutional taxes. So stay tuned on that. History repeats.

“The Unites States has already had two failed central banks. Between 1870 and 1913, the US experienced the greatest economic boom in history without a central bank.” –John Allison, pg 187

UST 10yr Yield 2.59-2.81%

SPX 1

Shanghai Comp 1

VIX 12.95-15.64

USD 79.46-80.16

Gold 1

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer