ISM Services printed its worst headline number since February of 2010 as the Employment series went sub-50, posting its largest MoM decline since November of 2008 and its first contractionary print in 25 months.

The dead cat bounce for New Orders off its worst print in more than 4 years in December continued as the series gained just +0.4 MoM in February - with a cumulative 2-month gain of just 1pt.

Indeed, the rolling averages (3M/6M/TTM) in New Orders across both the Manufacturing and Non-Manufacturing survey’s continue to slow.

On the positive side, Prices Paid slowed sequentially and the Backlogs index ticked above 50 for the first time in 4 –months. Unsurprisingly, weather remained the ubiquitous caveat for both pundits and ISM survey respondents

In the end, the takeaway is really just this:

We’ve seen multi-decade/record MoM declines across a number if the sub-indices in the two ISM survey’s in recent months. Yes, perhaps the weather is providing a modest-to-moderate negative distortion but, even if you discount that, the current Trend is one of deceleration.

Overall, the ISM data remains in agreement with the preponderance of fundamental, domestic macro data which continue to reflect a slowdown from a second derivative perspective.

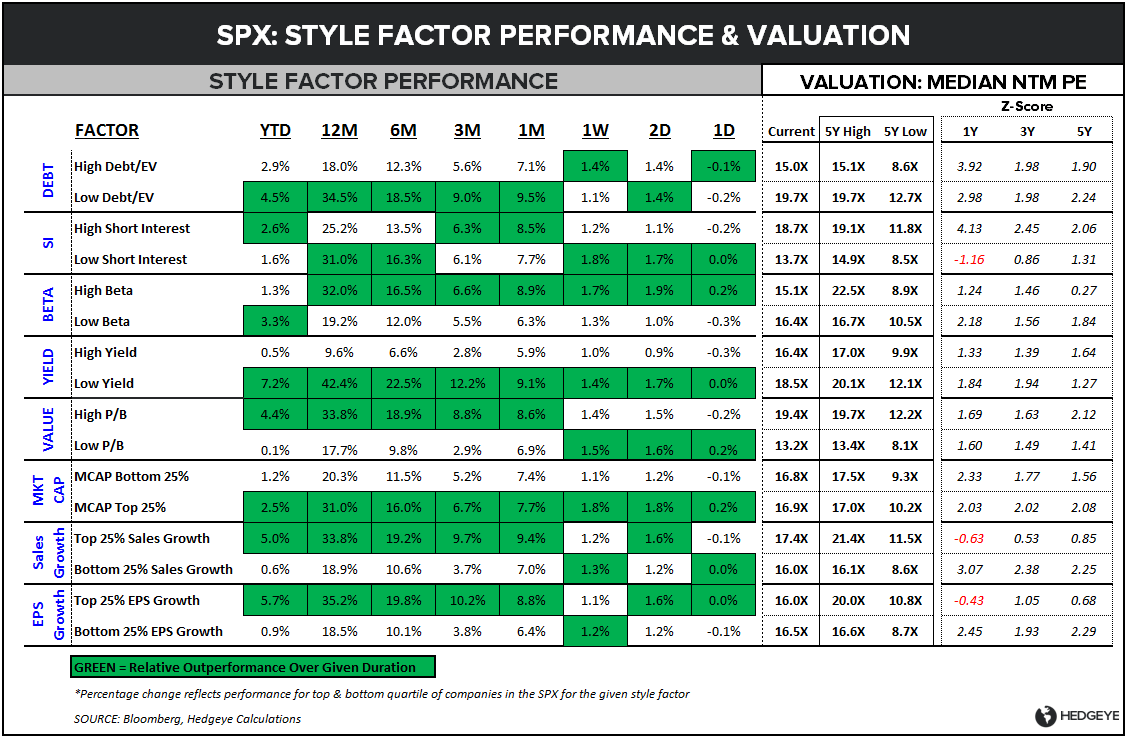

HOW IS THE MARKET SCORING 1Q14: Equity Indices are up but the market continues to provide a relative bid to slower-growth sector/assets (Bonds/Utilities/Gold).

Low Beta/Large Cap/Low Leverage Style factors continue to outperform and, with commodities and inflation hedge assets outperforming as well, investors (seemingly) continue to expect a rhetorical shift in policy out of the Fed in response to the fundamental deterioration.

More broadly, if the high-end is reigning in consumption (see Monday’s note: Consumer Spending: High End in Retreat) alongside a slowdown in housing and portfolio appreciation and energy and commodity inflation continues to drive the deflator higher while taking a larger share of wallet for the bottom 80%, the upside for consumption growth in the immediate/intermediate term remains limited.

TAKING HIGH PROBABILITY SWINGS: Will warmer weather bring a bounce in the reported data and, in reflexive fashion, drive confidence/hiring/etc higher, and a resurgence in pro-growth equity flows?

Perhaps, but neither the fundamental data nor the price signals are supportive of that probability currently.

We’ll change alongside the data, but until then we’ll continue to keep our gross and net domestic equity exposure tighter than we did over the Nov 2012 – Dec 2013 period, tilting that exposure towards slower growth sectors or those with positive leverage to inflation (vs. our focus on high beta, pro-growth, consumer leverage in 2013) while holding higher allocations to bonds and select commodities.

Looking forward to more manic weather and labor force participation rate related commentary come Friday…..

Christian B. Drake

c

@HedgeyeUSA