TODAY’S S&P 500 SET-UP – February 28, 2014

As we look at today's setup for the S&P 500, the range is 30 points or 1.47% downside to 1827 and 0.15% upside to 1857.

SECTOR PERFORMANCE

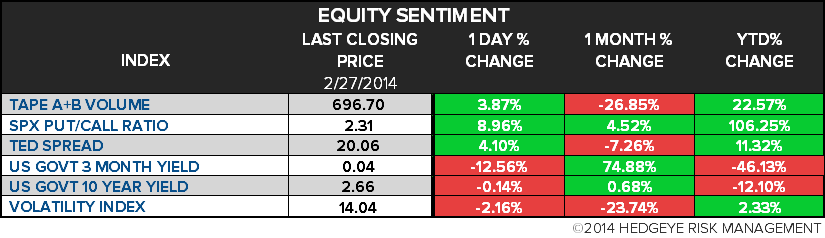

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.33 from 2.32

- VIX closed at 14.04 1 day percent change of -2.16%

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: Revised GDP q/q, 4Q, est. 2.5% (prior 3.2%)

- 9:45am: Chicago Purchasing Mgrs, Feb., est. 56.4 (pr 59.6)

- 9:55am: UofMich. Conf, Feb. final, est. 81.2 (prior 81.2)

- 10am: Pending Home Sales m/m, Jan., est. 1.8% (prior -8.7%)

- 10:15am: Fed’s Stein, Kocherlakota, Evans, Plosser speak

- 1pm: Baker Hughes rig count

GOVERNMENT:

- 4:45pm Obama DNC speech topics may incl mid-term elections, Affordable Care Act, immigration laws

WHAT TO WATCH:

- Mt. Gox files for bankruptcy in Tokyo with 6.5b yen debt

- Euro-area February inflation exceeds economists’ forecasts

- Yuan drops most on record amid band widening speculation

- Apple wins dismissal of $2.2b patent suit in Germany

- AT&T said to build Europe case amid silence on Vodafone

- Jos. A. Bank seeks talks with Men’s Wearhouse on deal

- Berkshire Hathaway annual report to be posted Saturday

- United sees rev. cut after 22,500 flights erased by storms

- IBM begins cutting U.S. jobs in $1b restructuring plan

- Salesforce projects 1Q rev. that may top ests.

- Gap profit exceeds estimates as deep discounts draw shoppers

- Gunmen occupy Crimea airports, Ukraine seeks IMF financial aid

- U.S. Jobs, Obama’s Budget, Buffett, ECB: Week Ahead March 1-8

AM EARNS:

- 3D Systems (DDD) 8am, $0.19

- Auxilium Pharmaceuticals (AUXL) 7am, $0.21

- BroadSoft (BSFT) 7am, $0.41

- Endo Health Solutions (ENDP) 6:32am, $0.93

- Exelis (XLS) 6:15am, $0.45

- Golar LNG (GLNG) premkt, ($0.07)

- Iron Mountain (IRM) 6am, $0.22

- Isis Pharmaceuticals (ISIS) 8:30am, ($0.16)

- Lexicon Pharmaceuticals (LXRX) 6am, ($0.05)

- Liberty Interactive (LINTA) 7:30am, $0.46

- Liberty Media (LMCA) 7:30am, $0.60

- Northwest Natural Gas Co (NWN) 6am, $1.03

- NRG Energy (NRG) 6:49am, $0.23

- Pepco Holdings (POM) 6:03am, $0.21

- Vantage Drilling Co (VTG) 7am, $0.08

PM EARNS:

- Dyax (DYAX) 4:01pm, ($0.04)

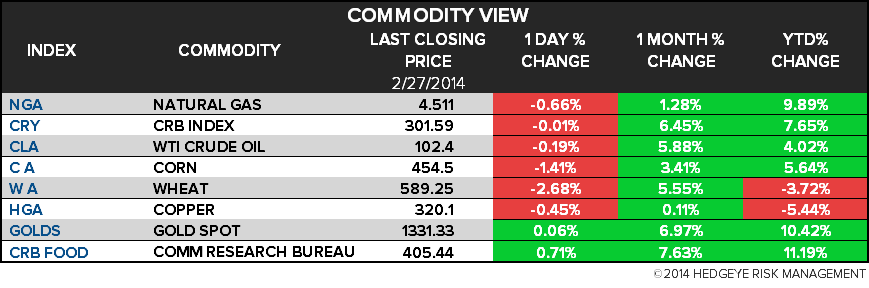

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- WTI Trims Monthly Gain on U.S. Demand, Discount to Brent Narrows

- Drought Threatens Southeast Asia Food Prices as Haze Worsens

- Nickel Reaches One-Week High on Speculation Supply to Tighten

- Gold Declines in London as Traders Book Profits Following Climb

- Natural Gas Heads for Biggest Weekly Drop in New York Since 1996

- Wheat Heads for Biggest Monthly Gain Since 2012 on U.S. Concern

- Coffee Declines as Rally Prompts Brazilian Sales; Cocoa Advances

- EU Sugar Plans Pit Growers Against Food Makers After Prices Fall

- Freeport May Declare Force Majeure at Grasberg Mine on New Rules

- London Gold Fix Study Indicates Decade of Bank Manipulation

- Afghanistan $3 Trillion Minerals Won’t Go Anywhere Without Rails

- Frozen East Coast Pays as Law Blocks Cheaper Fuel Flows: Energy

- Cosan Seeks $4.7 Billion Deal to Streamline Sugar Transportation

- Rebar in Shanghai Falls a Third Month as China Demand Weakens

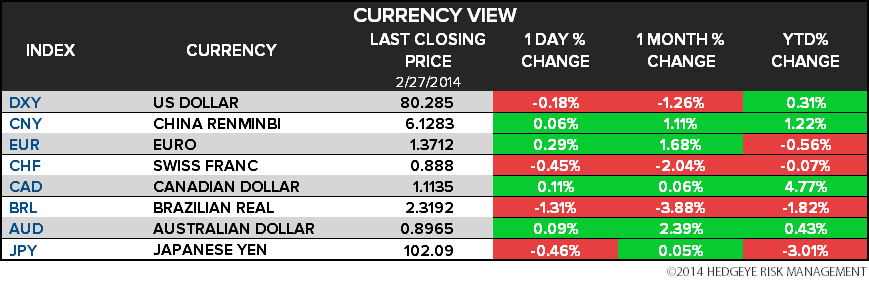

CURRENCIES

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

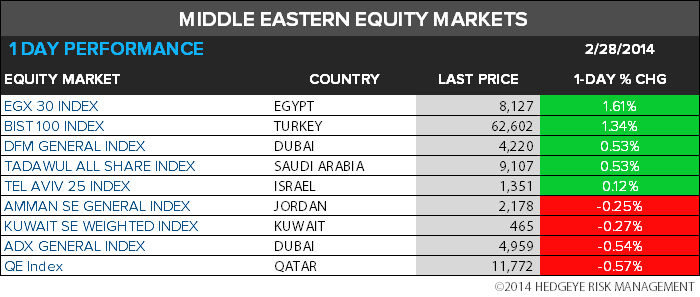

MIDDLE EAST

The Hedgeye Macro Team