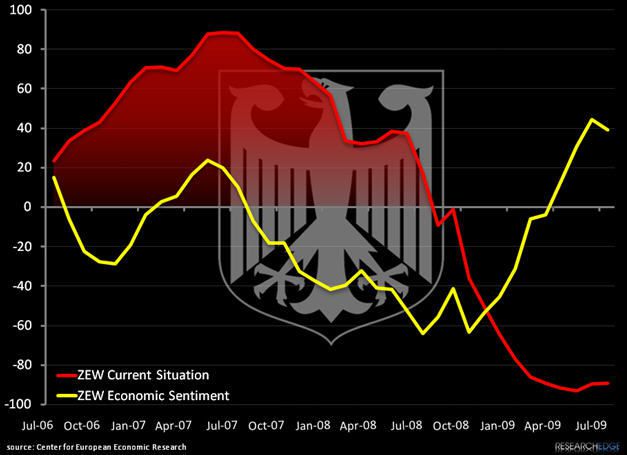

The ZEW Center for European Economic Research reported today that its July index of investor and analyst expectations slipped to 39.5 from 44.8 in June. The index aims to predict economic health six months ahead, and came in considerably lower than surveyed economists' forecast of 47.8. Conversely ZEW's gauge of the current economic situation rose to minus 89.3 from minus 89.7 in June, underperforming a consensus forecast of -87.8.

July's drop comes after months of sequential improvement in economic expectations (see chart) and recent improvements in underlying fundamentals. May German Industrial Production improved on a monthly and annual basis, helping to confirm a bottoming in production; and Factory Orders improved 4.4% on a monthly basis. (For more, see our post on 7/8 "Sequential Improvement for Europe's Workhorse"). Exports picked up 0.3% on a month-over-month basis in May while imports declined 2.1%, contributing to an increase in the unadjusted trade surplus to $9.6 Billion from $9.4 Billion in April, according to the Federal Statistics Office.

Inflation is currently running at a healthy annual 0.0-0.1% (at the Eurozone average) and we don't expect that number to veer greatly when July's report comes out tomorrow. As we move into 2H '09 we expect to see a slight increase in unemployment, offset with increased exports that should turn consumer and investor confidence higher. Look for Factory Orders to be an important indicator of the health of the German economy.

In light of this data, moderating expectations for future growth indicated by the ZEW survey suggest a realistic appraisal of sluggish global demand, rather than a negative sentiment shift.

While we've yet to see positive performance out of the DAX in 2009 (currently at -1.1% YTD) our bullish bias on Germany remains. We believe that Germany's significant industrial capacity provides a structural advantage, especially as global economies melt up. Further, the country's economic rather than financial leverage, a function of the government's aversion to overextending its balance sheet and Chancellor Merkel's balanced pledge of 85 Billion Euros to promote growth through tax cuts and programs like its "cash-for-trash" auto rebate will benefit steady but slow economic improvement in 2009 and positive growth in 2010, especially when compared to some its financial levered Western European peers, including: Italy, Spain, UK, and Ireland.

Matthew Hedrick

Analyst