Editor's note: This unlocked research note was originally published February 06, 2014 at 14:53 by Retail Sector Head Brian McGough. For more information on how you can subscribe to Hedgeye click here. Institutions please ping sales@hedgeye.com.

Note: Our goal today is not to present a complete bullet-proof bull case on ZQK, but rather to share some of the building blocks of our call, and set the stage for a more comprehensive research product that we expect to present in the coming weeks.

ZQK is one of our top long-term ideas. We think that the consensus view has it all wrong.

Those who are bullish are focused around the new management team, cost cutting, and optimization of a broken organization. While we agree with those points, the reality is that those initiatives will only get the stock into the high single digits. Which doesn't get us too excited given that the stock is already pretty much there. In order for us to build confidence in ZQK as a BIG call from here, we need revenue growth. We were skeptical at first – probably because the company hasn’t grown its top line in about 5 years. Yeah, we really like new management – and quite frankly are surprised that the Board attracted such high quality – but if you hand a bunch of broken and saturated brands to even the best management team, we’re pretty sure it will be a colossal failure. Fortunately, our research suggests that's not the case here.

We conducted an extensive analysis based on insight from a diverse group of Action Sports consumers, and walked away with confidence that the ZQK brands are far more relevant and authentic than we suspected. There’s very little that needs to be done to get these brands to a point where the new ZQK management team can kick-start growth.

While we’re only slightly ahead in 2014, our revenue estimate in the out years is 23% ahead of consensus. We also think that ZQK has well over $1.00 in earnings power, which is more than 50% ahead of consensus. A buck in earnings on top of a $7 stock certainly grabs our attention.

Accordingly, this is the first of a series of notes that outlines some key factors behind our thesis, with this report focusing specifically on brand desirability and authenticity. The data referenced is based on a statistically valid survey of 1,000 Action Sports consumers.

Later in this series, we’ll ultimately build up, in specific detail, how and why we are different than the Street as it relates to categories, brands, consumers, and geographies. If you’d like to listen to our original presentation on ZQK, click the following link (http://app.hedgeye.com/m/n_T/a'R(u6/zqk-survey-conference-call).

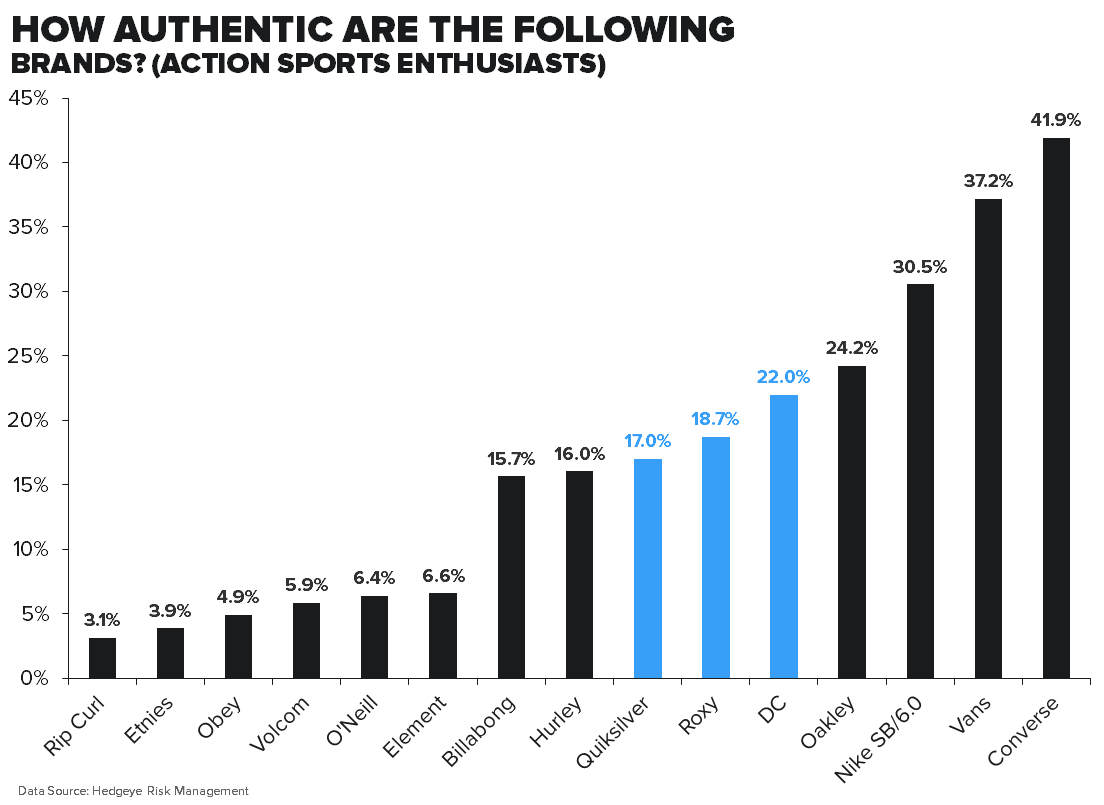

Question #1: Brand desirability remains high

It goes without saying that underinvestment in ZQK's core brands has hurt top line growth trajectory, but brands have bent - not broken. We asked consumers to rank the following brands in the order that they would purchase if price was taken out of the equation – which we translate as ‘desirability’. In charting out the results (see chart below), ZQK brands scored towards the higher end of the peer group. Vans, Nike S.B., etc. have stolen share over the past few years, but not to the extent that we had anticipated. Quite frankly, we expected ZQK’s brands to score near the bottom. This was clearly not the case.

Question #2: Core consumers still like the brand

One of our greatest concerns headed in to our study is that we’d find out that Action Sports Enthusiasts would consider Quik, Roxy and DC as being too mainstream. Unfortunately, once a brand becomes mainstream, there’s really no coming back. Again, we thought we’d learn that ZQK scored near the low end of its’ peer group. In reality that simply was not the case. Did it do as well as Nike, Vans and Converse? No. But it outscored well over a dozen other brands (some are not pictured here), and proved to be well above average. In a perfect world we’d like higher scores, but the bottom line here is that the survey tells us that ZQK's core consumers have not given up on the brand. Not by a long shot.

Question #3: Repurchase Intent

The worst thing a brand can do is fire its consumer. It’s abundantly clear to us that ZQK did not go there. A company can fix distribution, product, and brand messaging, but it’s nearly impossible to get consumers back when they've said they are gone for good (i.e. LULU).

So we asked questions to gauge people’s intent and willingness to purchase product in the future. The groupings to the right side of the chart show the percent of people that indicated they would ‘likely’ or ‘definitely’ shop these brands in the future. Any way we slice it, we think that the numbers are impressive. But the key area to look at is the cluster of three columns to the far left. This is where we ask people if they will ‘never shop this brand again’. We ask this in all the surveys we conduct, and by far and away ZQK’s reading ranked among the most favorable. Only 2.0%-2.5% of consumers say that they’ll never return – and we’d argue that Roxy’s high reading is a function of older teens having outgrown the core product.

Question 4: Power Rankings

One of the ways we rank brands is in what we call a ‘Power Ranking’. In effect, it takes into account two factors. 1) Where the brand ranks in consumers’ desirability and awareness, and then 2) the revenue base of the brands. Why does that matter? Everybody is aware of Converse and Vans. But not necessarily the case with much smaller brands like DC, Volcom, and Etnies. So we take the brand factors, and we adjust for the size of the revenue base it generates. It’s one of the best ways we can normalize stats across companies.

Surprisingly, in our Power Rankings, ZQK is beat by only one brand – Hurley (owned by Nike), which has a surprisingly strong awareness relative to its size. But DC and Roxy registered particularly strong results. Quiksilver came in at 0.9x, which is in-line with Converse, Vans and Volcom. Overall, a good showing.

The Bottom Line

Our goal here today is not to outline a complete bullet-proof bull case, but rather to share some of the building blocks that will lead to a research product that we expect to present in the coming weeks. This is only 4 of 52 slides we have in our deck, and our data files include much more information.

Please contact us if you want more info.