WTW 2014 GUIDANCE

Guidance was a considerable disappointment, missing consensus EPS estimates by over 45% at the midpoint. Below are the main guidance takeaways from its earnings call.

- Revenue: ~$1.4 billion vs. consensus of $1.5 billion

- EPS: $1.30-$1.60 vs, consensus of $2.72

- North America: Revenue & Attendance down low 20% (vs. -11% & -15% in 2013)

- Online: Revenue to decline high-teens (vs. 4% growth in 2013)

- United Kingdom: Revenue to decline 20% range (vs. 20% in 2013)

- Europe: Revenue to decline mid-single digits (vs. flat in 2013)

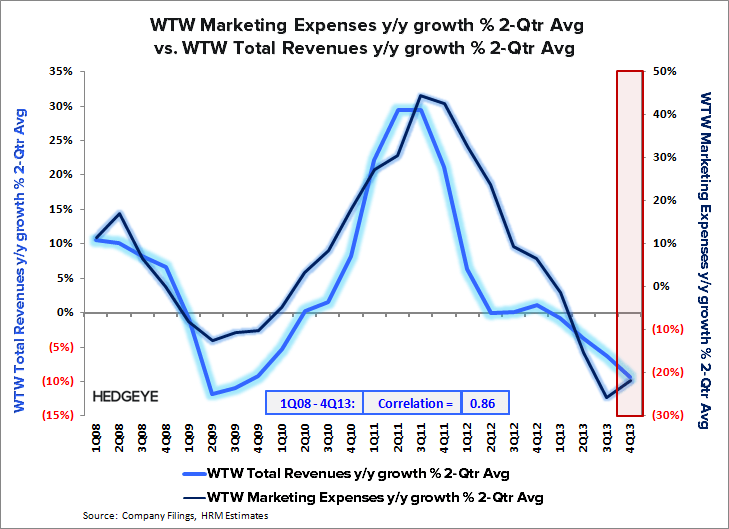

- Marketing: to decline $20mm y/y (-7% y/y)

SHORT THESIS UPDATE

WTW didn't offer anything concrete as to how it plans to reignite growth, or address the growing competitive threat from free apps and activity monitors.

Management chose to focus on Weight Watchers being the market leader while implying it has the best product in the industry. While that could be true, it's not a question of the value of the Weight Watchers product, but whether the end-user values its product as much as the company is looking to charge for it.

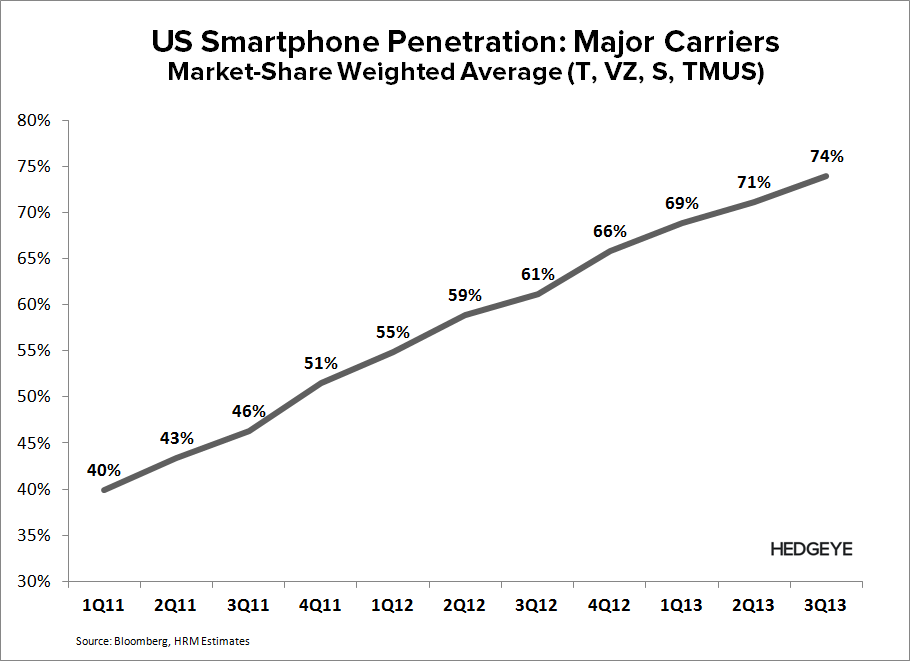

Free apps have been out there for a while. That's not the main issue. The main issue facing WTW is that access to these apps continues to climb; with smartphone penetration nearly doubling over the last 3 years to 74% in 3Q13 from 40% in 1Q11.

We don't believe WTW can right the ship without taking a more aggressive approach to membership growth and retention. It's plans to cut marketing in 2014 suggests it's going the opposite way, which we believe will only exacerbate it's member retention issues.

More importantly, WTW has a decision to make. It can maintain its current pricing ($43 for a monthly pass, $19/month for its online product) and continue to cede share, or it can reduce pricing to become more competitive. In either event, revenues will take a hit, whether it's membership or ARPU.

Consensus is assuming that revenues stabilize in 2015, which suggests the street is discounting the secular threat facing WTW. So we'll remain short from here, until the street finally gets it.

Hesham Shaaban, CFA

@HedgeyeInternet

Thomas W. Tobin

@HedgeyeHC