Research Edge Portfolio Positions: CAF, EWZ

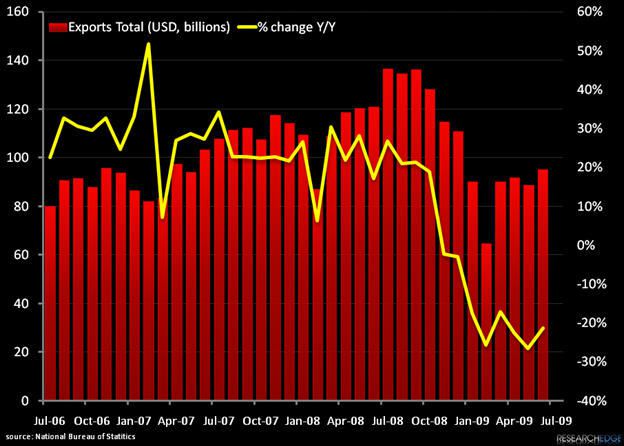

June trade data released by the National Bureau of Statistics today showed a modest sequential improvement in exports with the total registering at a decline 0f 21.3% on a year-over-year basis (see chart below). This represents the eight consecutive declining months on a year-over-year basis, and despite the earnest efforts of Beijing to pull all levers to soften the landing for export dependant industries, there is still no indication that there is any light at the end of the external demand tunnel. Remember, the US and the UK are a mess.

(continued text post chart)

Imports on the other hand, showed a marked improvement with a significant sequential uptick to -13.2% year-over-year as stimulus driven demand continues to chug along (see chart below).

Imports of key industrial commodities continued to expand. NBS estimates for iron ore inputs, an input measure we follow closely, registered at the second highest monthly level ever at 55.3 million metric tons, a year-over-year increase of 46.3% (see chart below). Although on the margin we continue to collect anecdotal reports that could support buying driven in part by speculative bubble formation and transport bottlenecks we continue to regard the commodity signals as overwhelmingly positive for continued production levels driven by infrastructure development and consumer demand for durable goods.

The clear winners in the race to provide The Client with what he needs are Brazil and Australia, who by NBS estimates have seen shipments rise to levels near 2008 highs after a tremendous rebound from January's lows (in the case of Brazil, June's total exports to china represented a 277% increase over January's shipments on a USD basis). We remain long Brazil via the EWZ ETF and continue to be positioned to trade Australian equities opportunistically on the long side based on price action.

We have been hammering home our message about the tactical situation for Chinese equities in recent days, and this bullish data does nothing to change that: We continue to be cautious in the face of such an extended rally. Strategically this data continues to confirm our thesis -but also intensifies our desire to search for any marginal data that could indicate asset specific bubble's forming.

In short, the data is decidedly positive and we remain decidedly confident.

Andrew Barber

Director