TODAY’S S&P 500 SET-UP – February 13, 2014

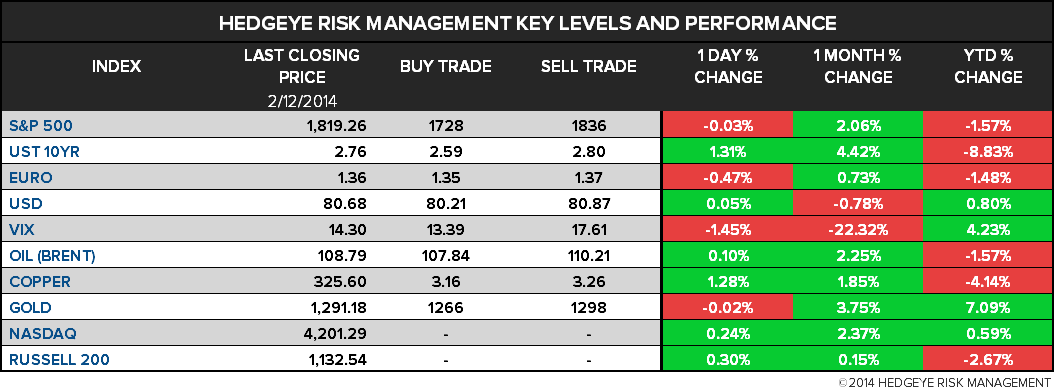

As we look at today's setup for the S&P 500, the range is 108 points or 5.02% downside to 1728 and 0.92% upside to 1836.

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.43 from 2.39

- VIX closed at 14.3 1 day percent change of -1.45%

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: Retail Sales Advance m/m, Jan., est. 0.0% (pr 0.2%)

- 8:30am: Initial Jobless Claims, Feb. 8, est. 330k (pr 331k)

- 8:45am: Bloomberg Feb. U.S. Economic Survey

- 9:45am: Bloomberg Consumer Comfort, Feb. 9 (prior -33.1)

- 10am: Business Inventories, Dec., est, 0.4% (prior 0.4%)

- 10am: Freddie Mac mortgage rates

- 10:30am: EIA natural-gas storage change

GOVERNMENT:

- POSTPONED:Fed Chairman Janet Yellen’s testimony before the Senate Banking Cmte

- POSTPONED: Senate Health, Education and Labor Cmte hearing on proposals to raise minimum wage

WHAT TO WATCH:

- Comcast said to agree to buy Time Warner Cable for about $44b

- Charter said unlikely to match Comcast’s Time Warner Cable bid

- U.S. to shut Washington offices as snowstorm hits Northeast

- POSTPONED: Fed Chair Yellen’s testimony to Senate Banking Cmte

- Royal Mail, Asos, Inter Pipeline, Seiko Epson join MSCI World

- China said to target export growth at slower pace than 2013

- Volcker Rule bankers’ lawsuit dropped as regulations revised

- Merck & Co.’s sale of consumer unit may top $10b, WSJ reports

- Buffett in talks to exit stake in former Washington Post owner

- Apple adds Macs assembled in Texas by Flextronics in U.S. push

- Lenovo projects end to Motorola losses With China phone plan

- ITC to review Avago decision in Mellanox patent case

- BNP Paribas profit drops on $1.1b U.S. legal provision

- Lloyds posts fourth consecutive loss on costs of redress

- Nestle forecasts sales growth in 2014 near low end of target

- Rolls-Royce falls after forecasting unchanged profit growth

- Oil inventories fell most since 1999 on demand in IEA estimate

- China January auto sales miss estimates as economy slows

- China Trust assets surge to $1.8 trillion amid default risks

- Storm causes havoc on U.K. rail as flooding forecast to worsen

AM EARNS:

- Amtrust Financial Services (AFSI) 7am, $0.78

- Apache (APA) 8am, $1.80 - Preview

- Avon Products (AVP) 7:01am, $0.30

- Barrick Gold (ABX CN) 6:30am, $0.41 - Preview

- Bombardier (BBD/B CN) 6am, $0.11 - Preview

- BorgWarner (BWA) 8am, $0.71

- Bunge (BG) 6:30am, $2.12

- Burger King Worldwide (BKW) 7am, $0.23

- Calpine (CPN) 6am, ($0.09)

- Canadian Tire (CTC/A CN) 7:46am, $2.26

- Cenovus Energy (CVE CN) 6am, $0.33

- Diebold (DBD) 8am, $0.58

- Discovery Communications (DISCA) 7am, $0.90

- Encana (ECA CN) 6am, $0.18 - Preview

- EQT (EQT) 7am, $0.68

- Generac Holdings (GNRC) 5:59am, $0.90

- GNC Holdings (GNC) 8am, $0.64

- Goldcorp (G CN) 8am, $0.23 - Preview

- Goodyear Tire & Rubber (GT) 7:30am, $0.63

- Great-West Lifeco (GWO CN) 12:44pm, $0.61 - Preview

- International Flavors & Fragrances (IFF) 7am, $0.91

- Jarden (JAH) 6:50am, $1.30

- Louisiana-Pacific (LPX) 8am, $0.05

- Manulife Financial (MFC CN) 6am, $0.43 - Preview

- Molson Coors Brewing Co (TAP) 7:30am, $0.72

- Nielsen Holdings NV (NLSN) 7am, $0.71

- PBF Energy (PBF) 7am, $0.56 - Preview

- PepsiCo (PEP) 7am, $1.00 - Preview

- Precision Drilling (PD CN) 6am, $0.17

- Realty Income (O) 9:15am, $0.21

- RioCan Real Estate Investment (REI-U CN) 7am,

- Sonoco Products Co (SON) 7:30am, $0.58

- Starwood Hotels & Resorts (HOT) 6am, $0.70

- Teck Resources (TCK/B CN) 5am, $0.43 - Preview

- TELUS (T CN) 8:30am, $0.48 - Preview

- Vantiv (VNTV) 7am, $0.44

- WhiteWave Foods (WWAV) 6am, $0.20 - Preview

PM EARNS:

- Agilent Technologies (A) 4:05pm, $0.66

- Allison Transmission Holdings (ALSN) 4:01pm, $0.37

- American International Group (AIG) 4pm, $0.97

- Brocade Communications Systems (BRCD) 4pm, $0.20

- Cliffs Natural Resources (CLF) 4:22pm, $0.79

- Cloud Peak Energy (CLD) 4:10pm, $0.23

- Ingram Micro (IM) 4:05pm, $0.79

- Key Energy Services (KEG) 6:18pm, ($0.06)

- Kraft Foods Group (KRFT) 4pm, $0.61 - Preview

- Liberty Global PLC (LBTYA) 5:40pm, $0.25

- Regal Entertainment Group (RGC) 4pm, $0.25

- Trulia (TRLA) 4:05pm, $0.07 - Preview

- Weight Watchers International (WTW) 4:05pm, $0.61

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Oil Inventories Fell Most Since 1999 on Demand in IEA Estimate

- Rice Exports From India Rising to Record as Iran Boosts Reserves

- WTI Crude Declines From Four-Month High as Gains Seen Excessive

- Gold Falls in New York After Gains Seen Encouraging Metal Sales

- Copper Drops as China Said to Target Slower Growth in Exports

- Rubber Falls a 2nd Day as Stronger Yen, Falling Oil Cut Appeal

- Soybeans Rise as Supply May Tighten Before South America Harvest

- Shree Renuka to Buy More Indian Raw Sugar as Exports Subsidized

- New Smelter Pipeline Threatens Any End to Aluminum Overcapacity

- Washington Offices to Close as Winter Storm Approaches Northeast

- Barrick Gold Earnings Trail Estimates as Production Declines

- U.K. Farmers Contend With Floods as Wheat to Pasture Submerged

- Coal Burns Bright as Utilities Switch From Gas: Carbon & Climate

- Palm Rises to Highest This Year on Exports Amid Brazil Dryness

CURRENCIES

GLOBAL PERFORMANCE

EUROPEAN MARKETS

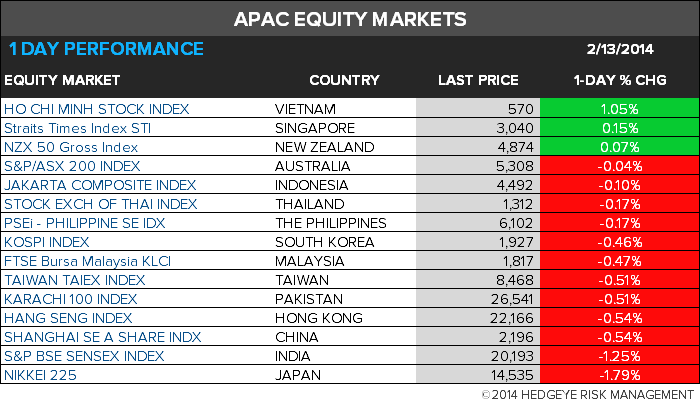

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team